Cost curves show the relationship between a firm's costs of production and output levels. There are several types of costs:

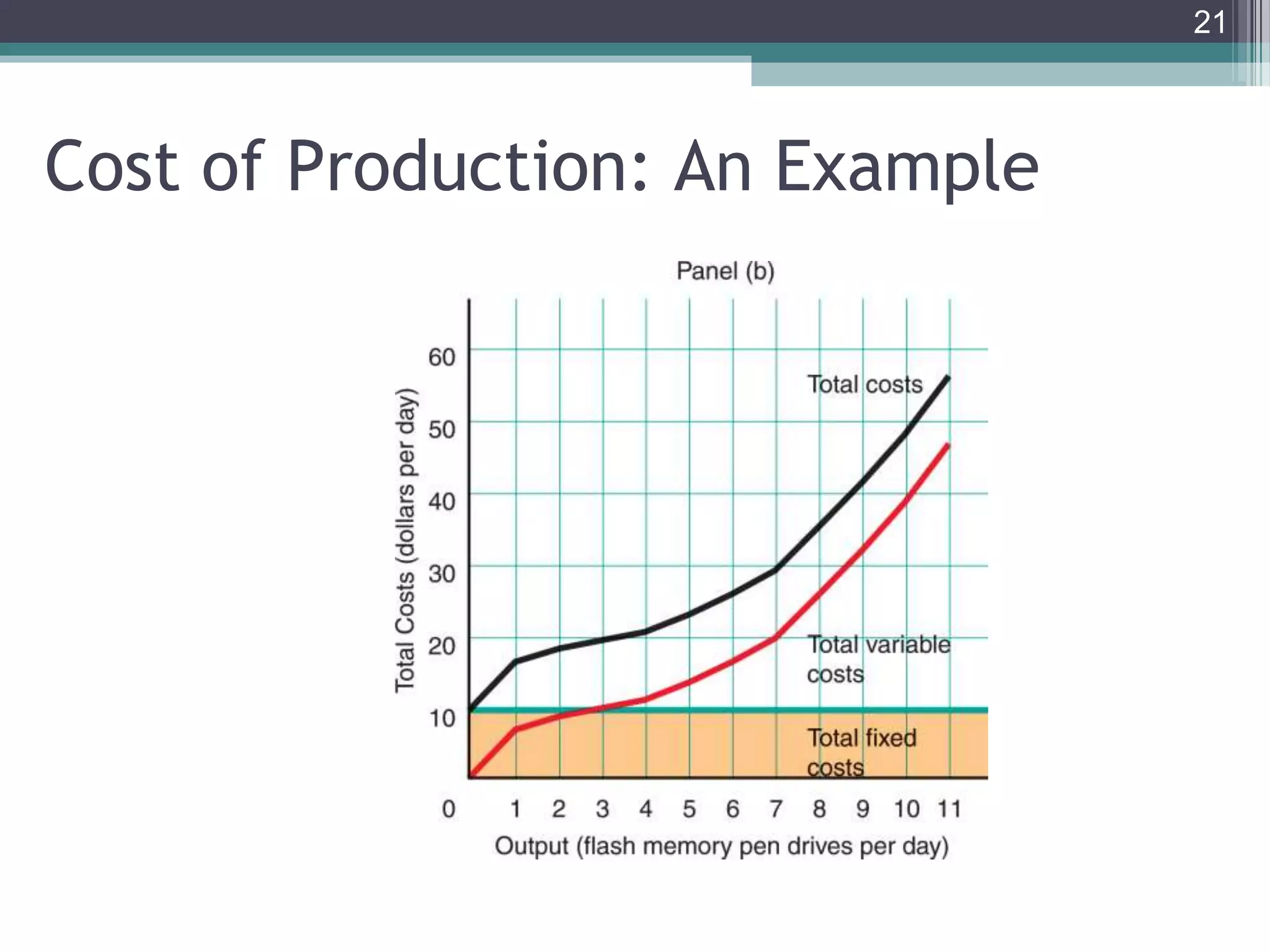

1. Total costs include fixed costs like rent and variable costs like wages that change with output. Average and marginal costs are derived from total costs.

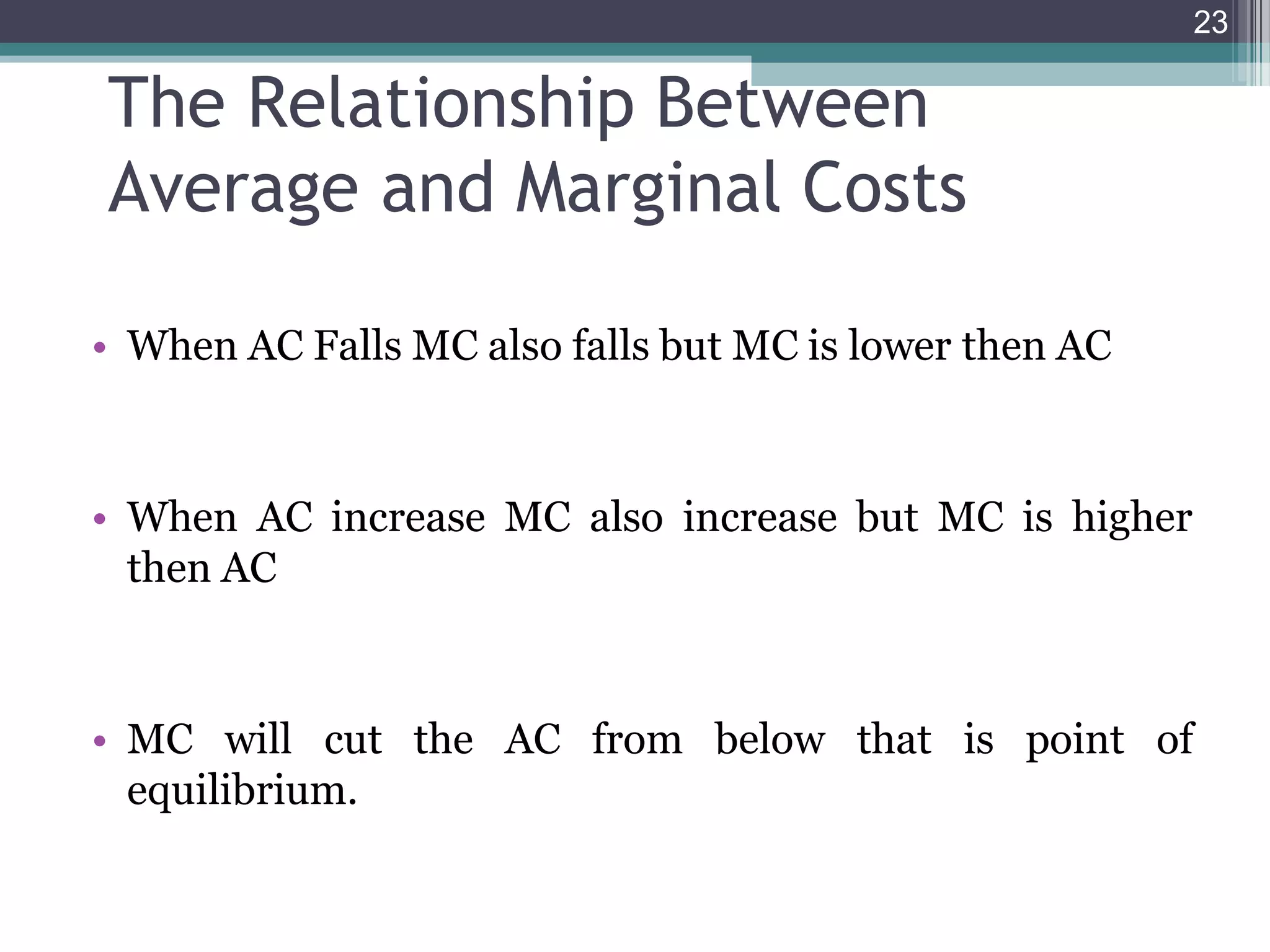

2. In the short run, firms have fixed costs so average costs fall then rise as output increases. Marginal cost cuts through average cost from below.

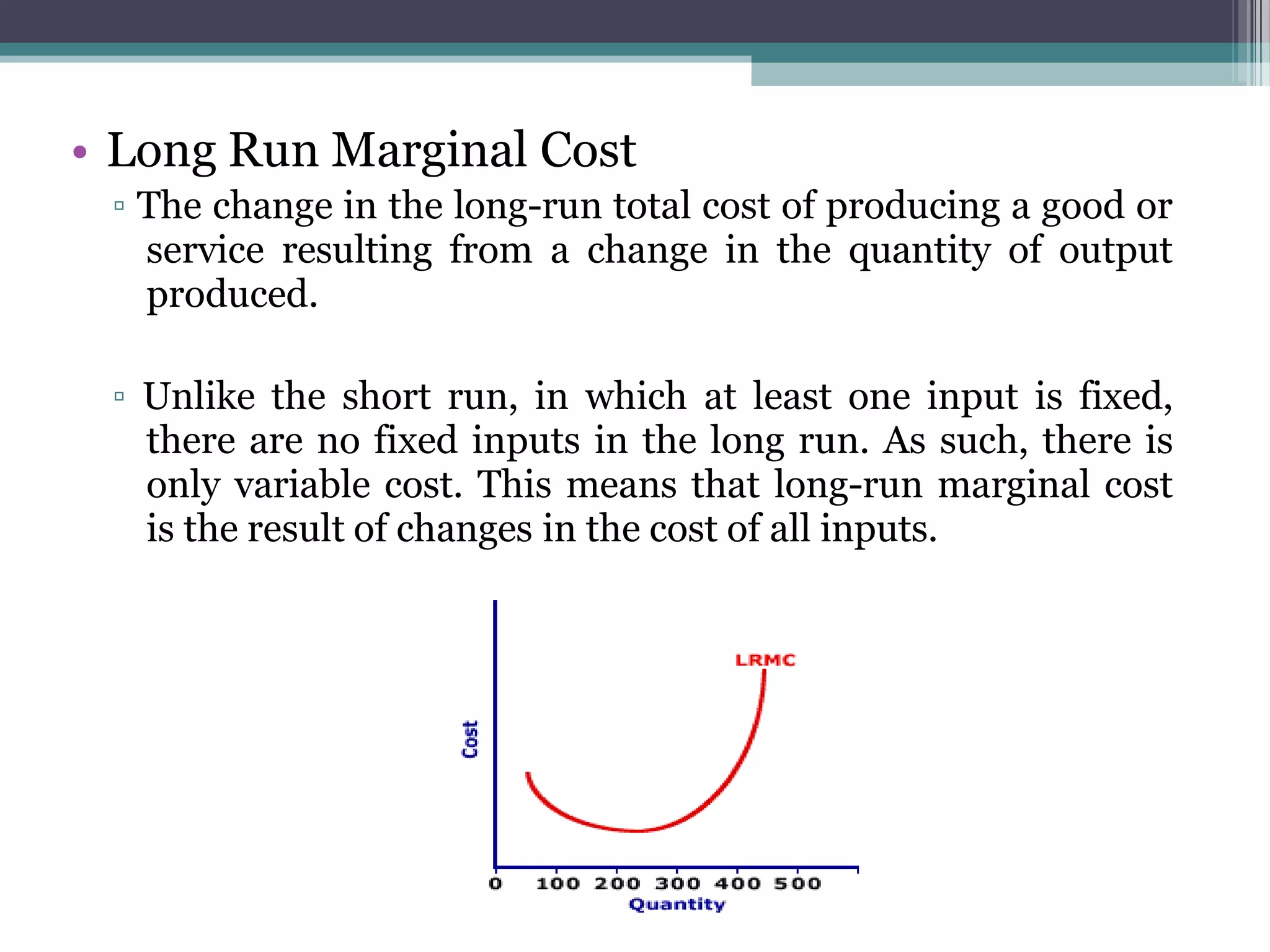

3. In the long run, all costs are variable so there is a U-shaped long run average cost curve from economies and diseconomies of scale. Marginal cost is the change in total costs from a unit change in output.