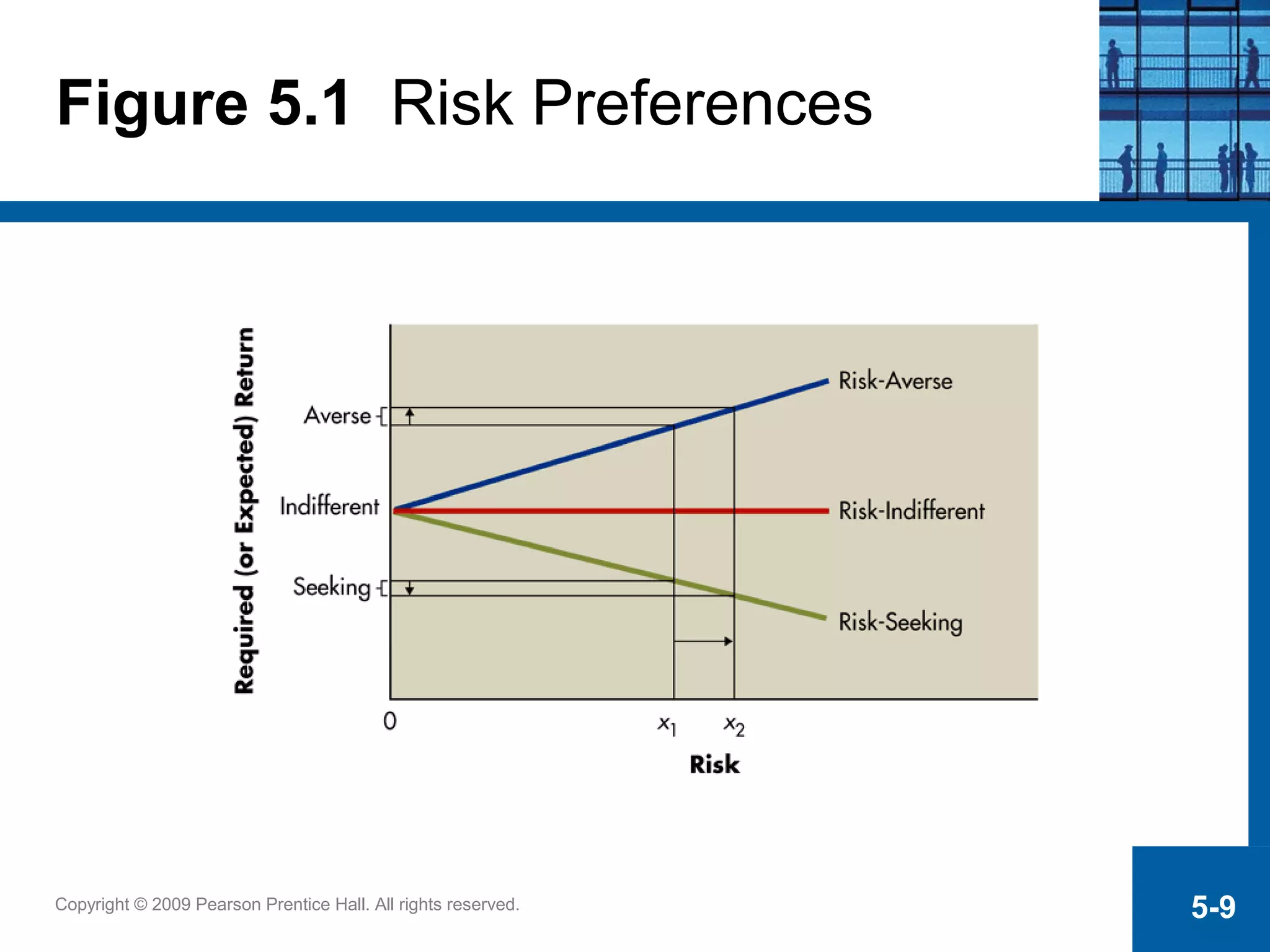

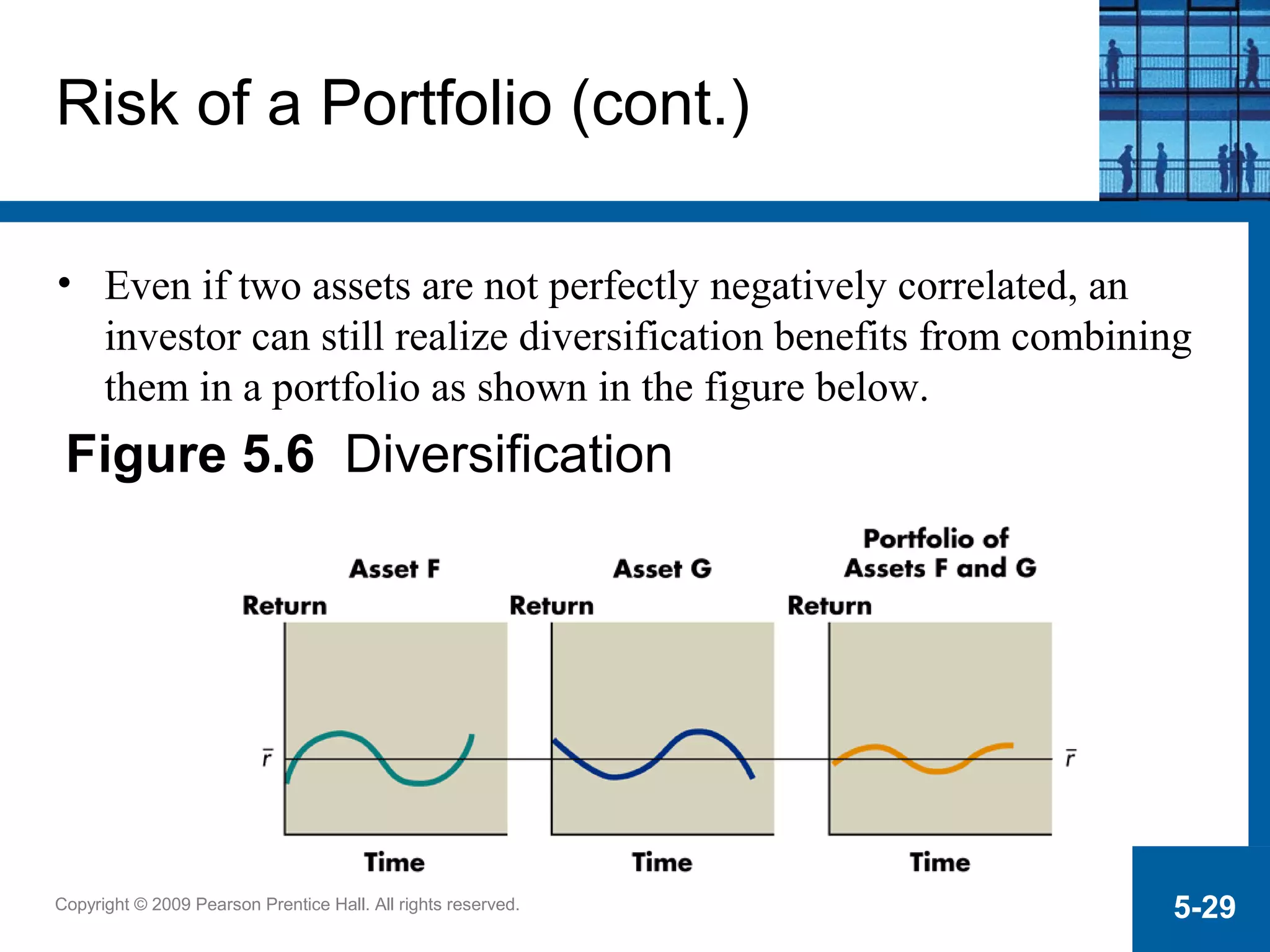

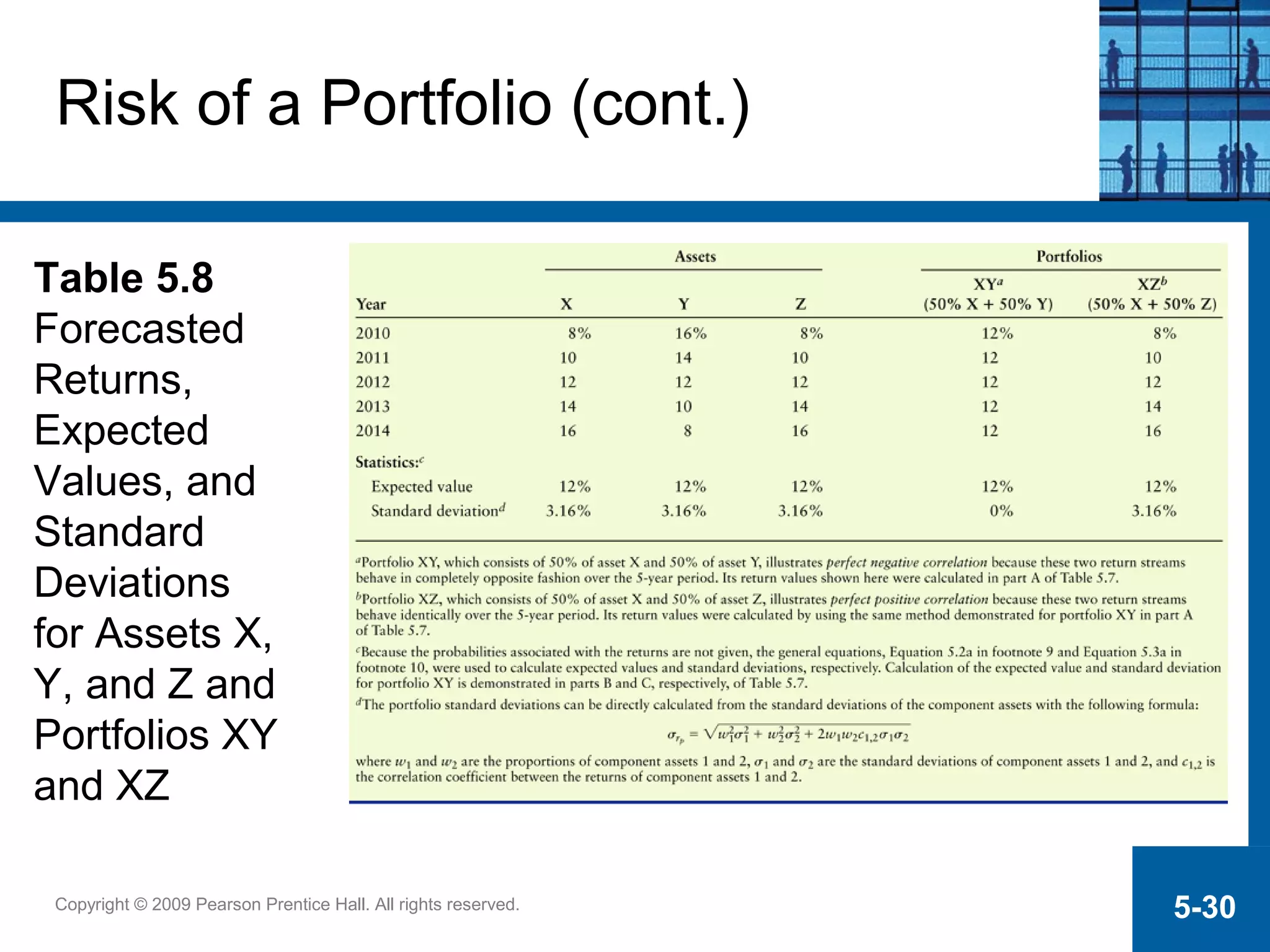

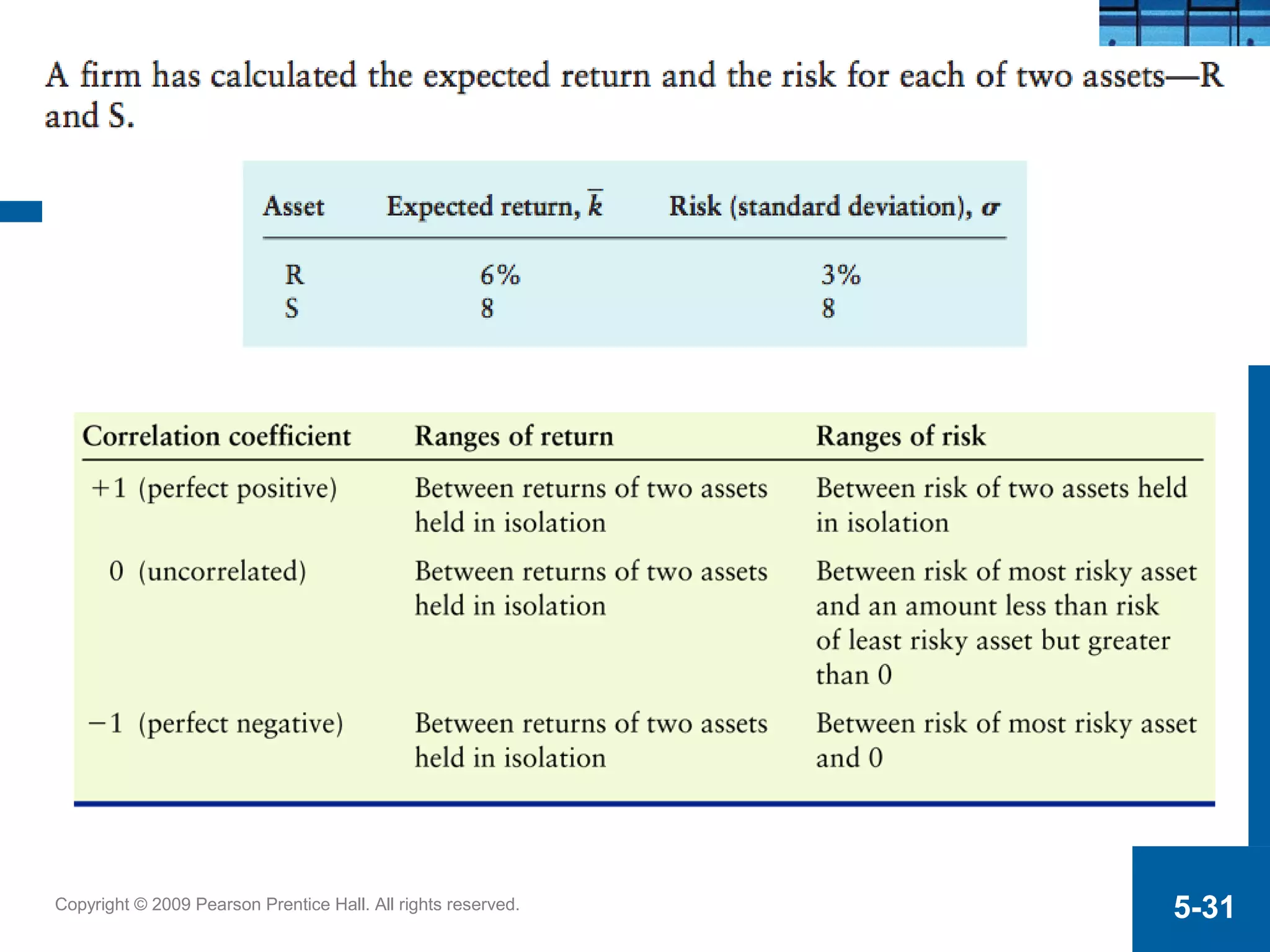

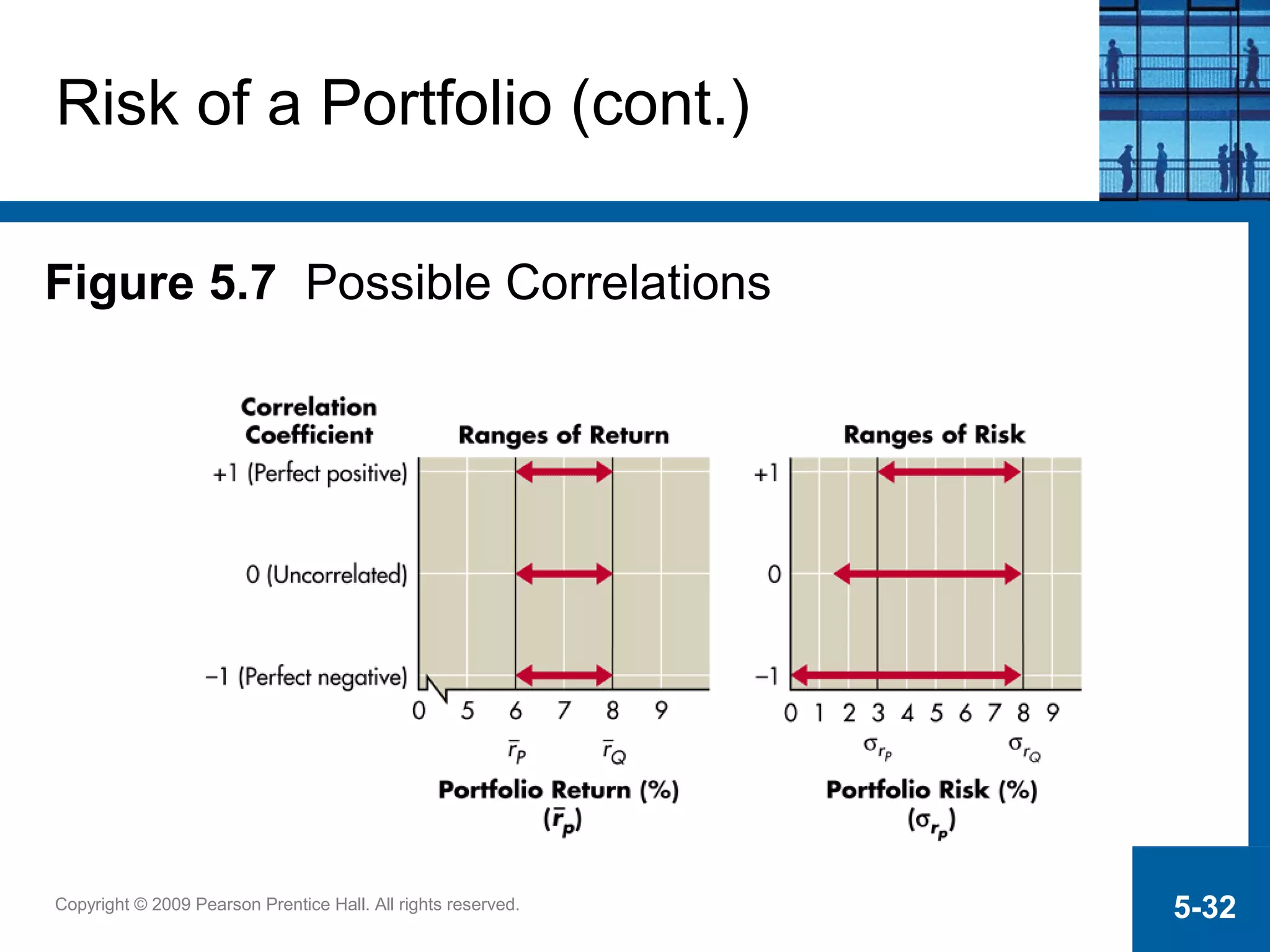

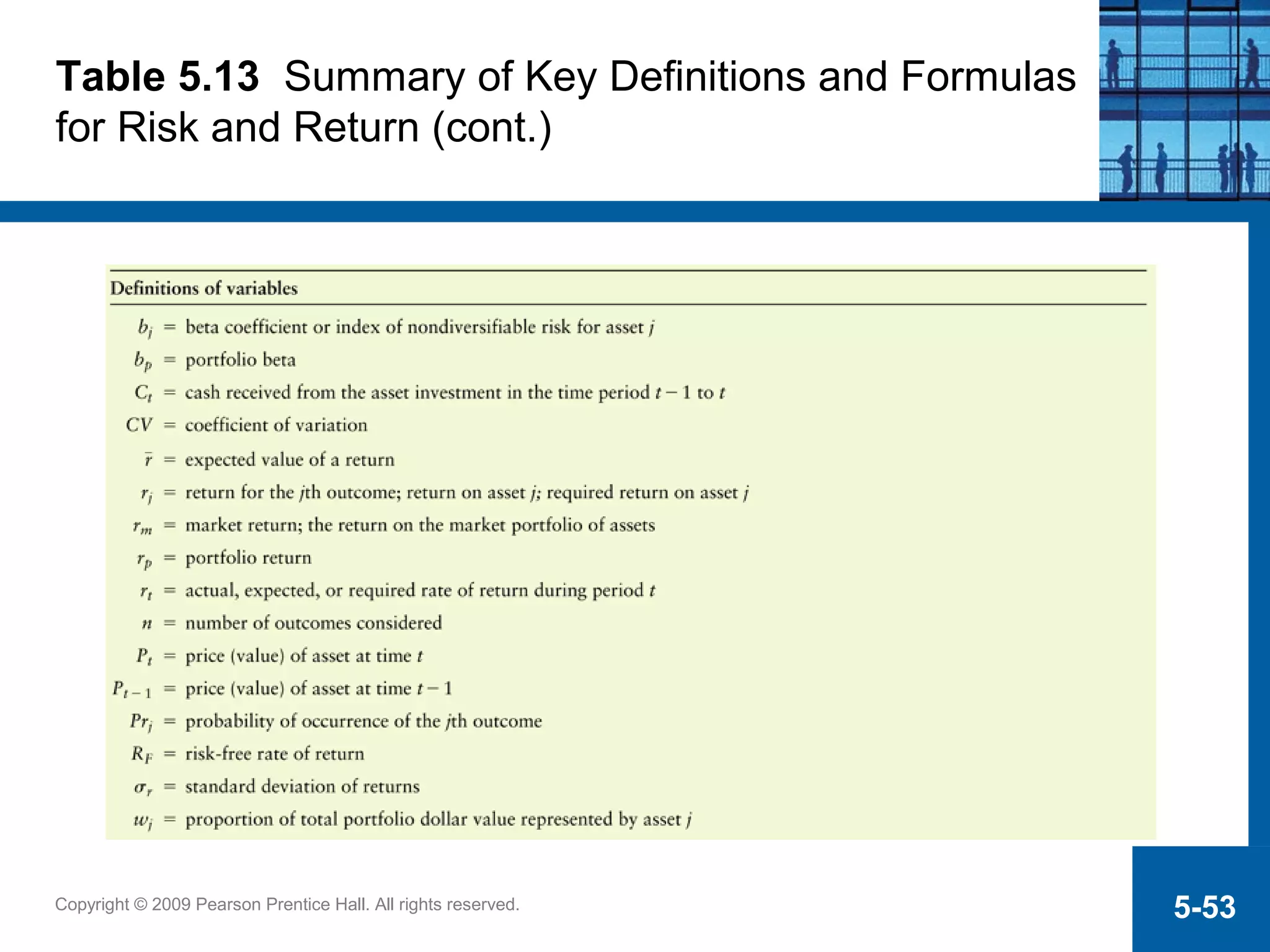

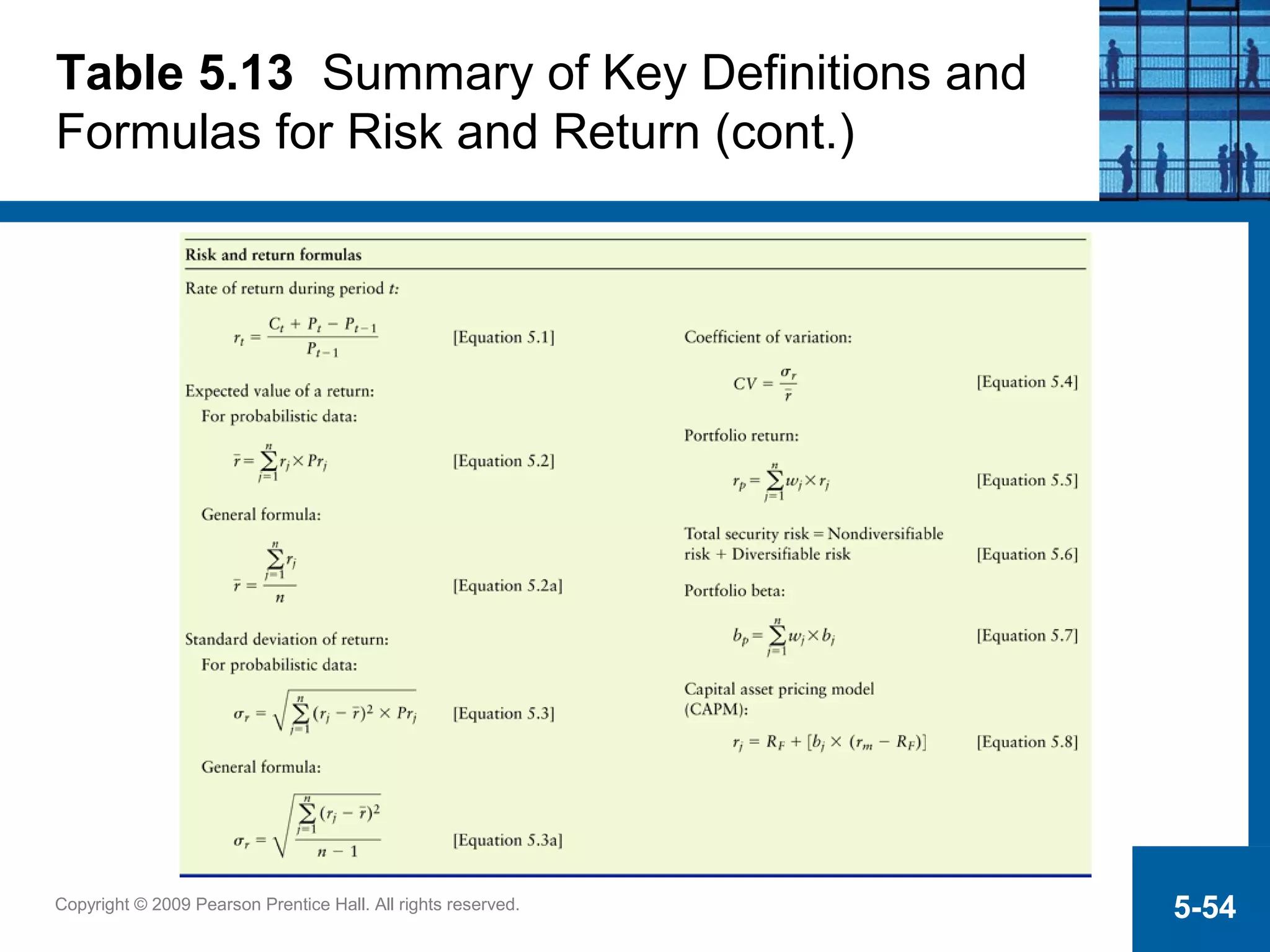

This chapter discusses the relationship between risk and return for both individual assets and portfolios of assets. It defines risk as the chance of financial loss and explains that higher risk assets generally provide higher expected returns. The chapter covers measuring the expected return, standard deviation, and coefficient of variation of individual assets. It then explains how forming a portfolio of assets can reduce overall risk through diversification. The chapter discusses how the correlation between asset returns impacts the risk reduction from diversification. It also addresses how adding more assets to a portfolio continues to reduce non-market or unique risk.

![Copyright © 2009 Pearson Prentice Hall. All rights reserved. 5-48

kZ = 7% + 1. 5 [11% - 7%]

kZ = 13%

Benjamin Corporation, a growing computer software

developer, wishes to determine the required return on asset

Z, which has a beta of 1.5. The risk-free rate of return is

7%; the return on the market portfolio of assets is 11%.

Substituting bZ = 1.5, RF = 7%, and km = 11% into the CAPM

yields a return of:

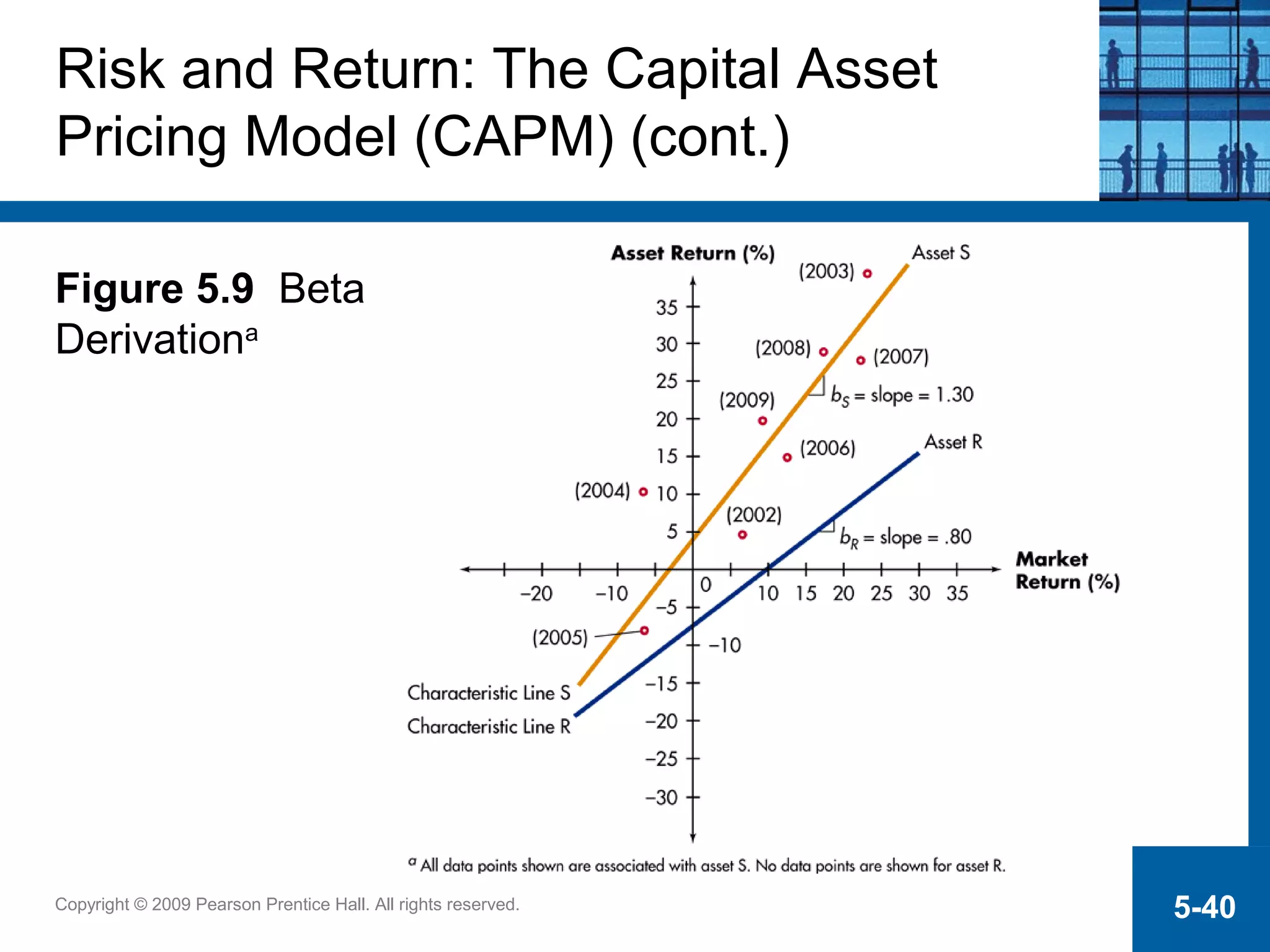

Risk and Return: The Capital Asset

Pricing Model (CAPM) (cont.)](https://image.slidesharecdn.com/riskandreturn-160928091902/75/Risk-and-Returns-48-2048.jpg)

![Topic 4[1] finance](https://cdn.slidesharecdn.com/ss_thumbnails/topic41-131107182635-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)