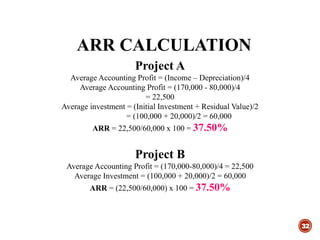

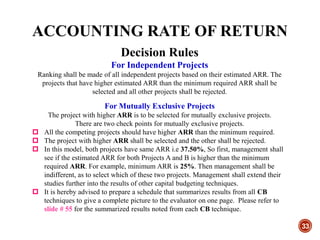

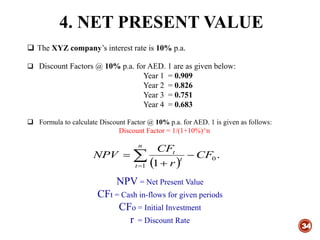

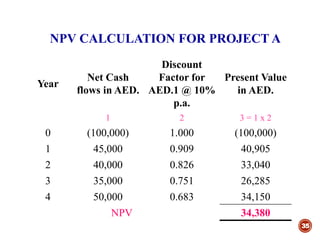

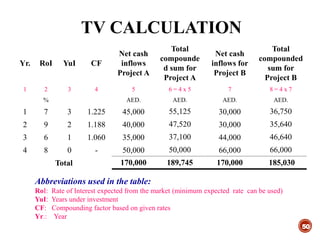

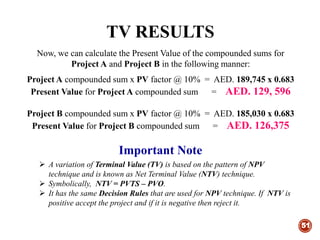

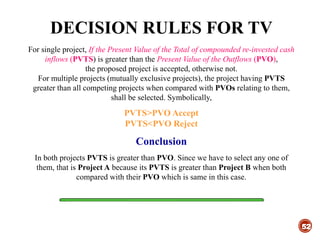

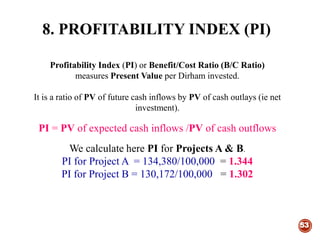

Downloaded 1,314 times

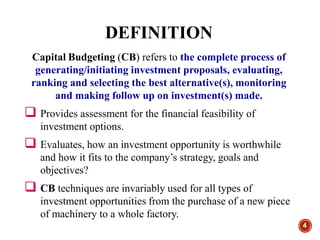

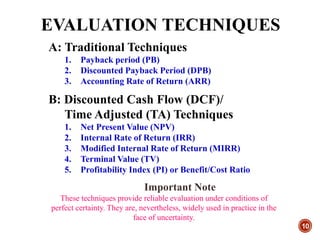

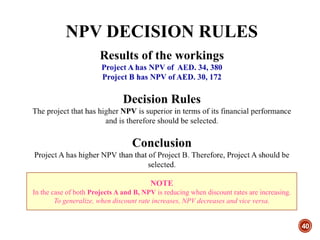

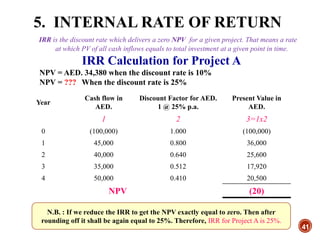

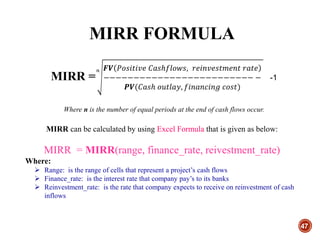

![CALCULATING IRR WITH EXCEL

FOR PROJECT A

43

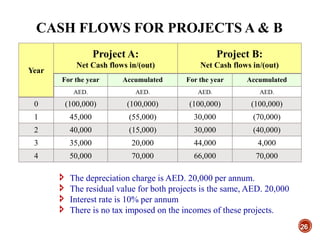

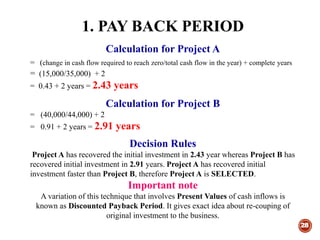

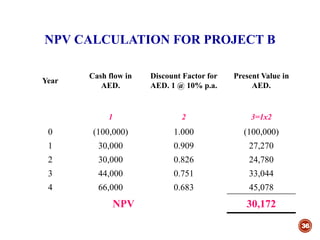

Year Cash flow in AED.

0 (100,000)

1 45,000

2 40,000

3 35,000

4 50,000

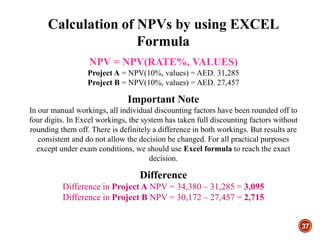

IRR for Project A = IRR(values, [guess])

This formula produces an IRR for Project A of 25%.

Tip

Select any cell where you want to see the result. Write =IRR(values, [guess]).

In the place of values give range of cells as given in the above table including

investment at Y0.](https://image.slidesharecdn.com/capitalbudgeting-150523153723-lva1-app6892/85/Capital-Budgeting-43-320.jpg)

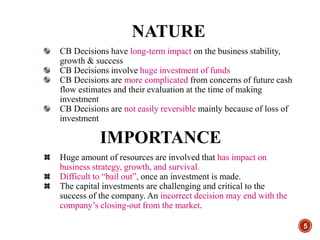

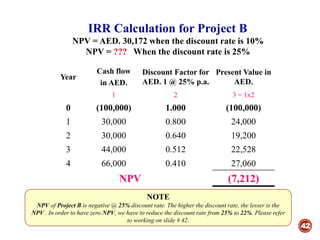

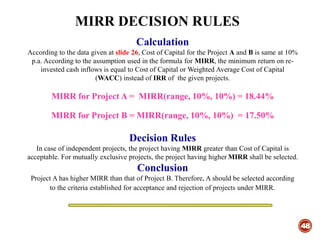

![44

CALCULATING IRR WITH EXCEL

FOR PROJECT B

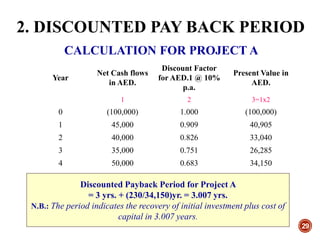

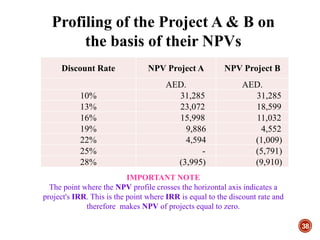

Year Cash flow AED.

0 (100,000)

1 30,000

2 30,000

3 44,000

4 66,000

IRR for Project A =IRR(values, [guess])

This formula produces an IRR for Project A of 21.42%.

TIP

Calculating IRR with EXCEL is easier than from the interpolation formula,

as given here-in-above. So it is advised to calculate IRR with EXCEL.](https://image.slidesharecdn.com/capitalbudgeting-150523153723-lva1-app6892/85/Capital-Budgeting-44-320.jpg)

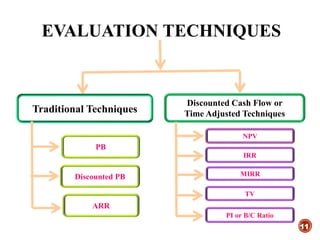

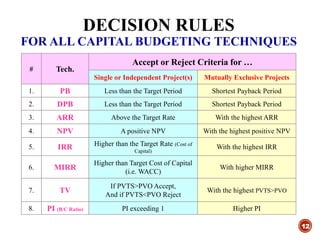

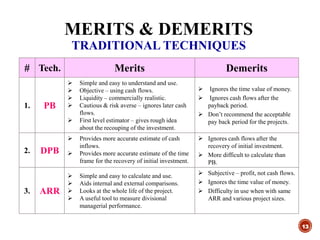

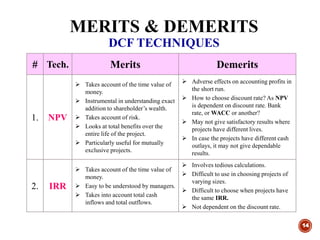

The document discusses capital budgeting, detailing its objectives, processes, and techniques for evaluating investment proposals. It emphasizes the significance of cash flow analysis over accounting profit and presents various decision-making techniques such as NPV, IRR, and payback period, while also addressing issues around capital rationing and the impact of non-financial factors. The document outlines a structured approach to selecting investment opportunities that align with a company's strategic goals and financial performance.

![5) capital_budgeting_(1)_-(2)[1].ppt.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5capitalbudgeting121-250323135834-146732f6-thumbnail.jpg?width=640&height=640&fit=bounds)