Downloaded 94 times

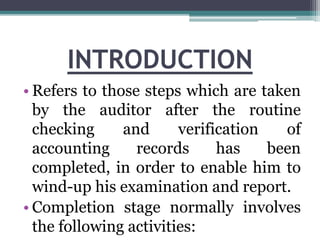

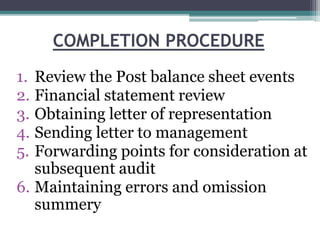

The completion stage of an audit involves final steps before issuing an audit report. It includes reviewing post-balance sheet events and the financial statements, obtaining a management representation letter, sending a letter to management, noting items to follow up on in the next audit, and preparing a summary of any unadjusted errors. The auditor seeks to identify any necessary adjustments to the financial statements, ensure compliance with standards and regulations, and communicate areas for improvement to management.

![Audit evidence a framework (ppt ch7[1].pdf)](https://cdn.slidesharecdn.com/ss_thumbnails/auditevidence-aframeworkpptch71-pdf-121211154609-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)