Downloaded 72 times

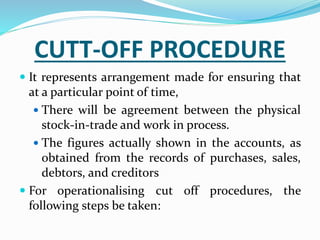

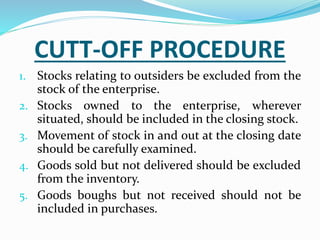

Vouchers provide documentary evidence of transactions recorded in accounting books. Auditors examine vouchers to verify transactions are valid, authorized, and correctly recorded. The extent of vouching depends on the strength of the company's internal controls - stronger controls allow auditors to check a sample rather than all transactions. Vouching typically involves two people comparing details in books to supporting documents. Cut-off procedures ensure physical inventory and account balances agree by properly accounting for stock movements and sales/purchases around the reporting date.