Downloaded 1,166 times

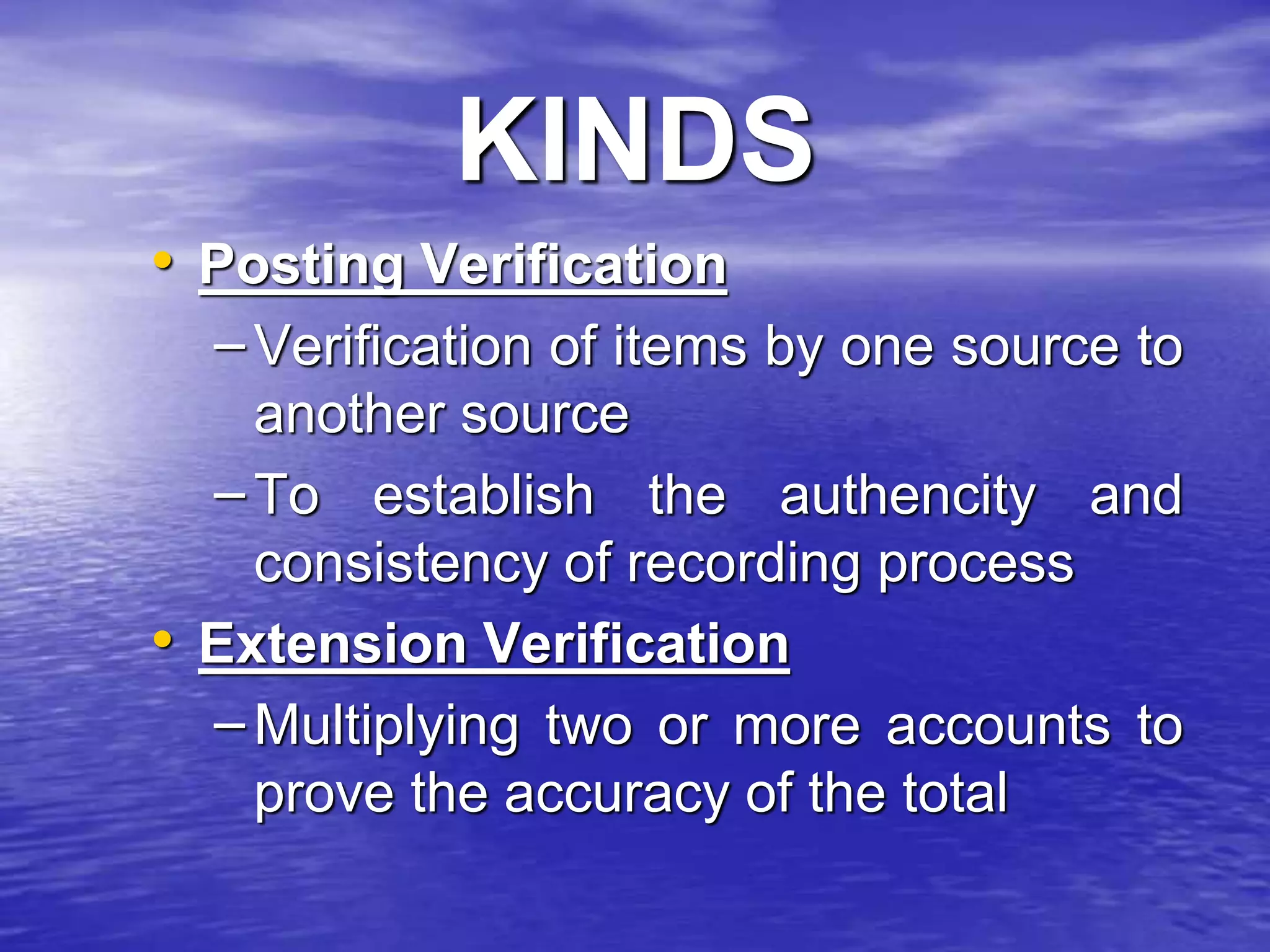

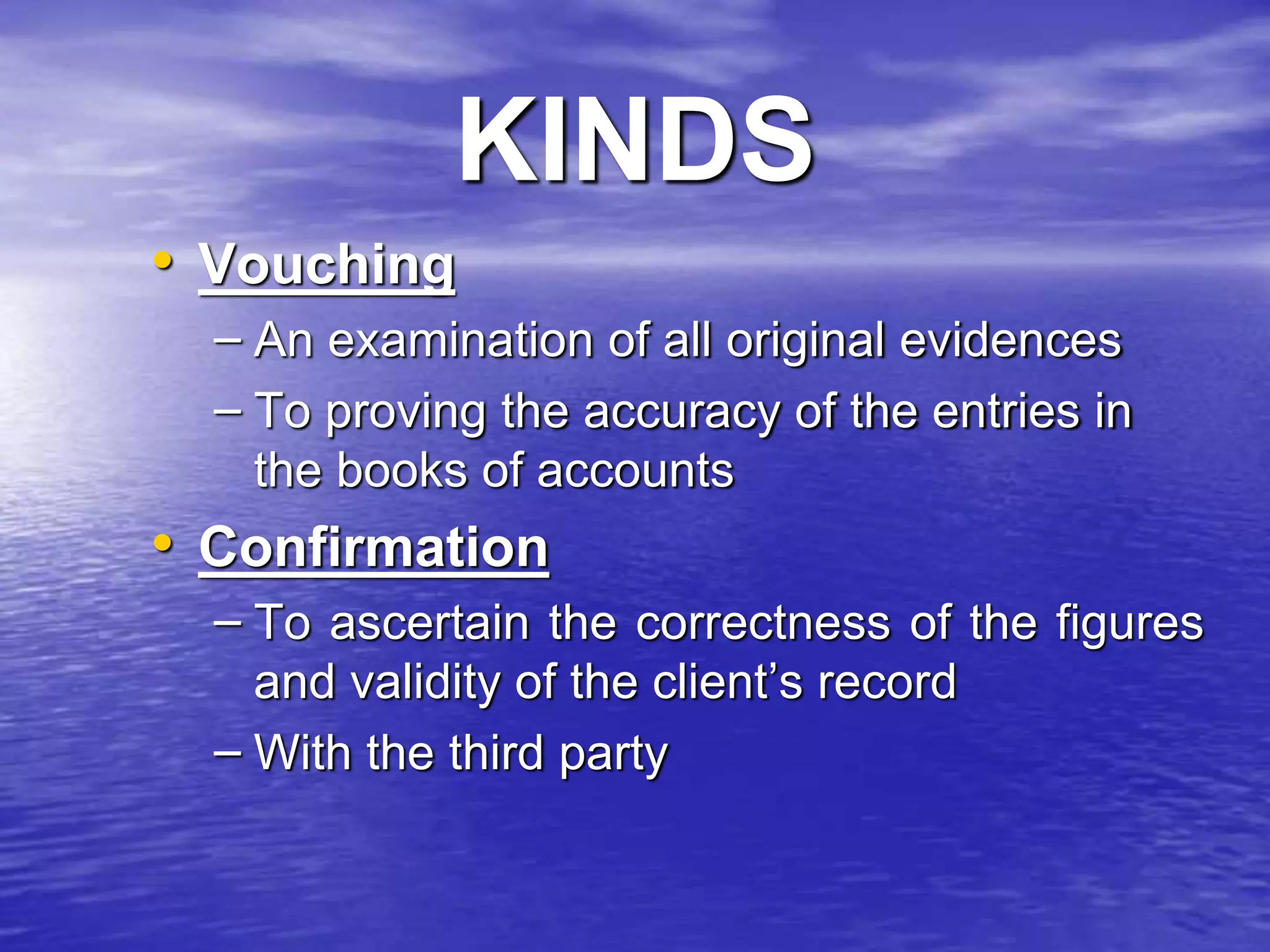

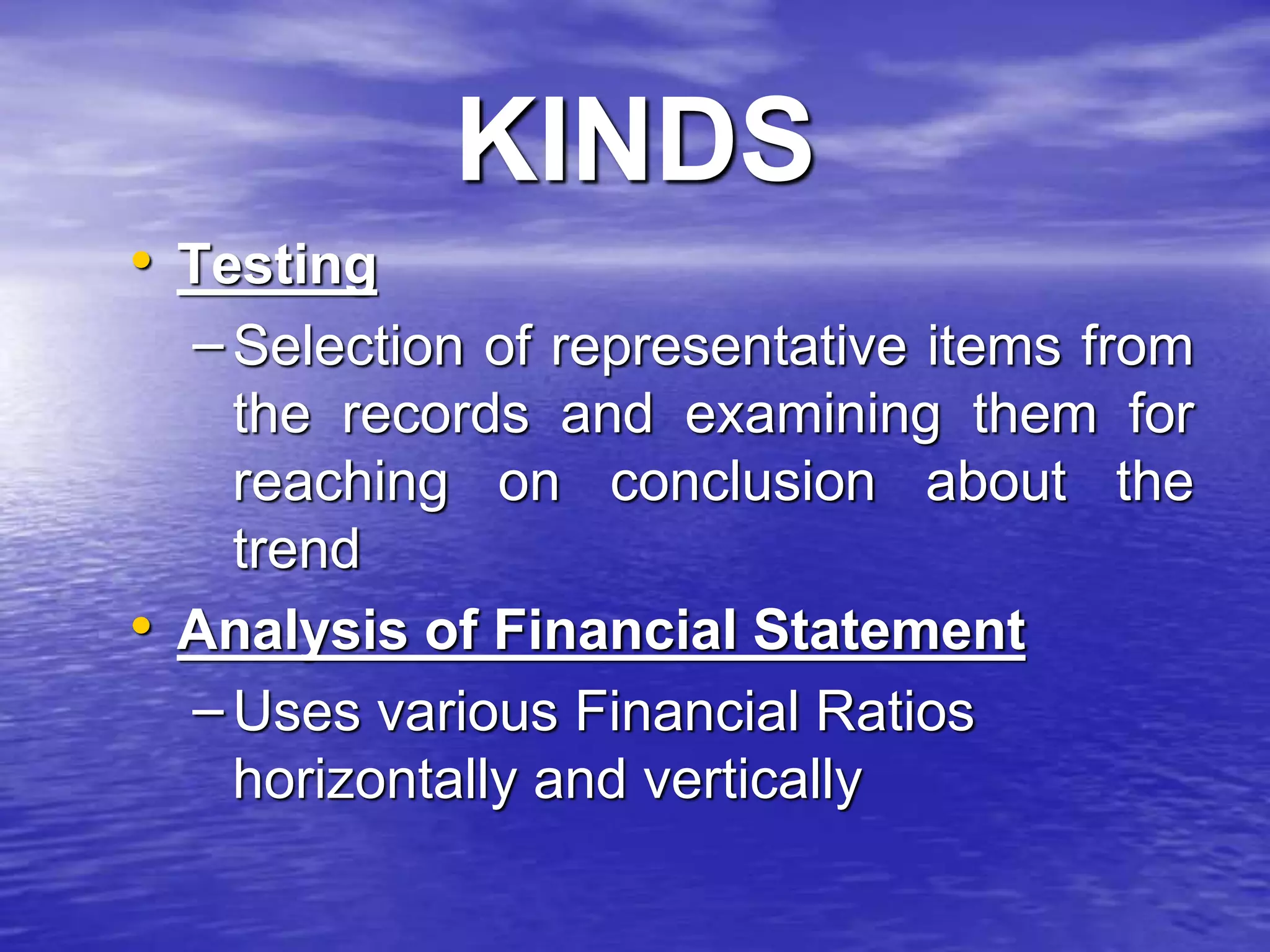

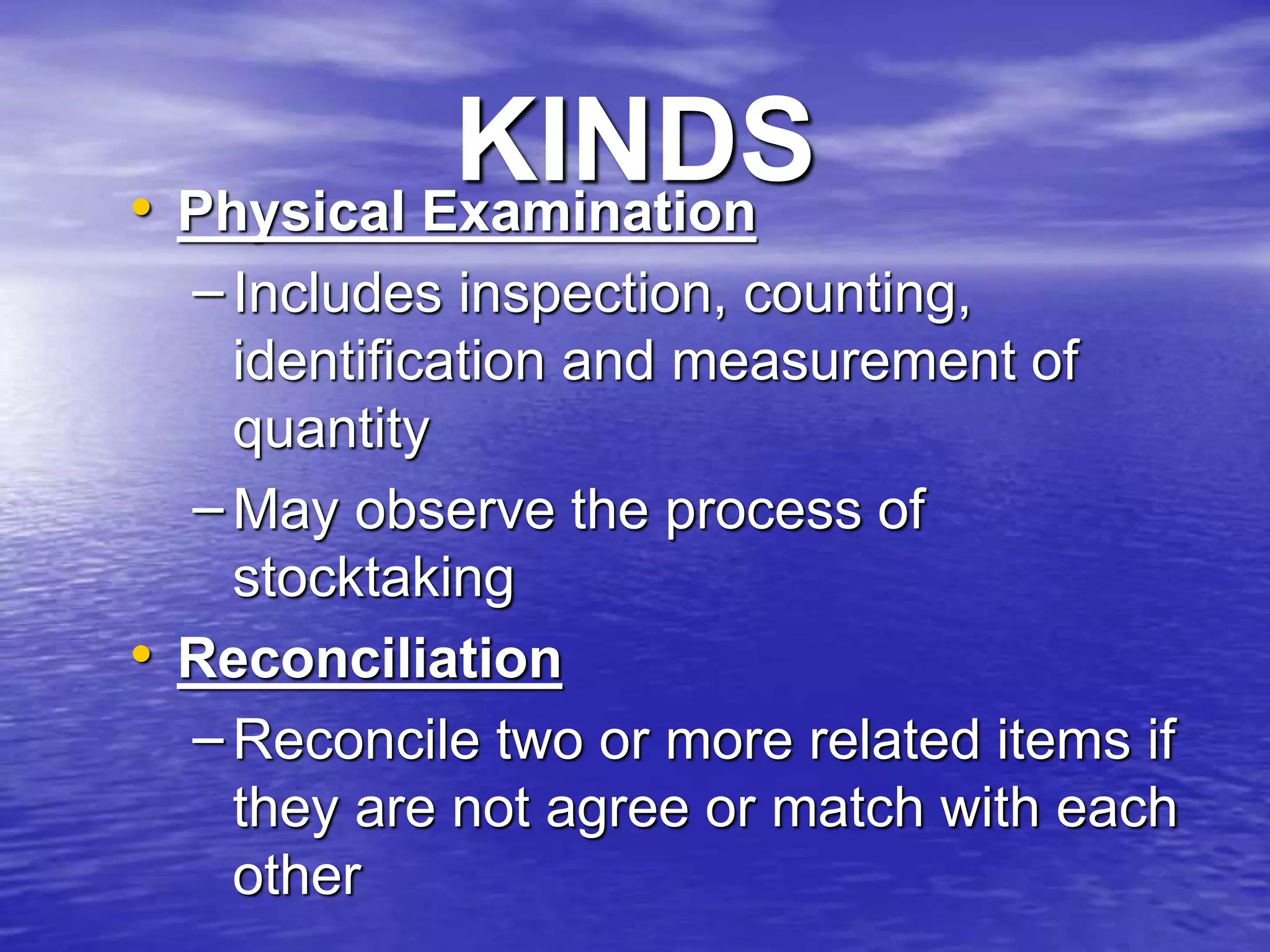

Audit techniques are tools and methods used by auditors to collect evidence to support their opinions on a client's financial assertions. The document outlines various audit techniques including posting and extension verification, vouching, confirmations, physical examination, reconciliation, testing, analysis of financial statements, sampling techniques, compliance testing, and substantive testing. Specific techniques are described like vouching of transactions, confirmation with third parties, testing of representative samples, and analytical review of financial statements. Obtaining management representations and using audit sampling are also discussed.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)

![Audit evidence a framework (ppt ch7[1].pdf)](https://cdn.slidesharecdn.com/ss_thumbnails/auditevidence-aframeworkpptch71-pdf-121211154609-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)