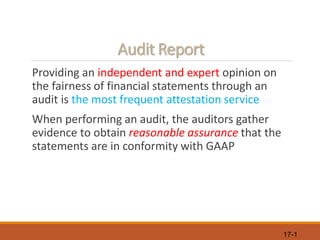

This document discusses key aspects of audit reports, including:

- The auditor's standard report provides an opinion on whether the financial statements are presented fairly and in accordance with GAAP.

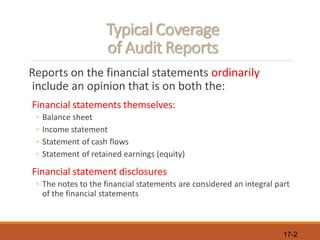

- Audit reports typically include opinions on the financial statements themselves (balance sheet, income statement, etc.) and the related disclosures.

- Modifications to the standard report may be needed if certain conditions are present, such as material departures from GAAP or scope limitations.

- The auditor's report for public clients follows specific requirements regarding titles, addresses, references to auditing standards, and inclusion of opinions on internal control over financial reporting.

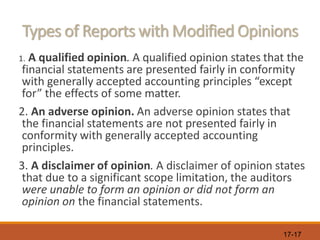

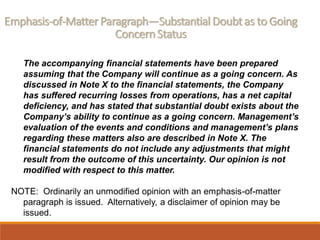

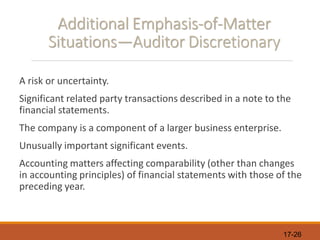

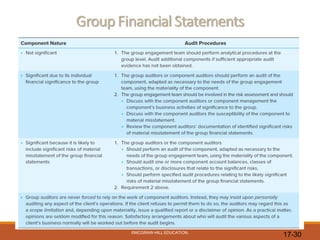

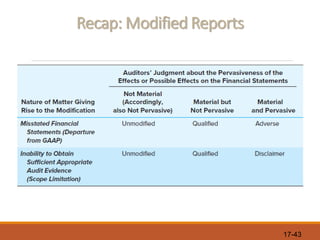

- The opinion paragraph states the auditor's opinion on whether the financial statements

![17-6

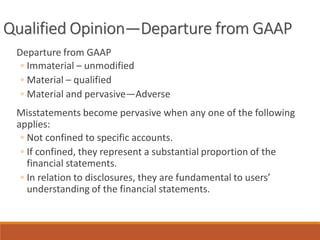

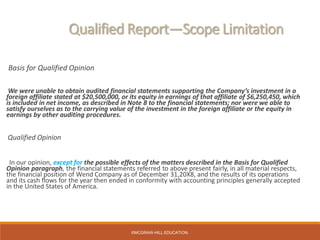

Opinion Paragraph

Opinion on the Financial Statements

We have audited the accompanying balance sheets of X Company (the

“Company”) as of December 31, 20X7 and 20X6, the related statements of

income, comprehensive income, stockholders’ equity, and cash flows, for

each of the three years in the period ended December 31, 20X7, and the

related notes [and schedules] (collectively referred to as the “financial

statements”). In our opinion, the financial statements present fairly, in all

material respects, the financial position of the Company as of December 31,

20X7 and 20X6, and the results of its operations and its cash flows for each

of the three years in the period ended December 31, 20X7, in conformity

with accounting principles generally accepted in the United States of

America.

We also have audited, in accordance with standards of the Public Company

Accounting Oversight Board (United States) (“PCAOB”) the Company’s

internal control over financial reporting as of December 31, 20X7, based on

Internal Control-Integrated Framework issued by the Committee of

Sponsoring Organizations of the Treadway Commission (COSO) and our

report dated February 9, 20X8 expressed an unqualified opinion.](https://image.slidesharecdn.com/chapterauditreport-191012071953/85/Chapter-audit-report-6-320.jpg)

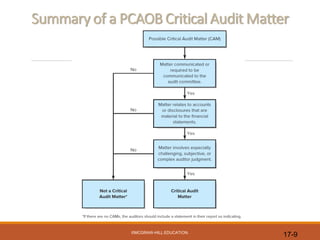

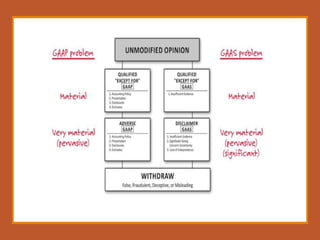

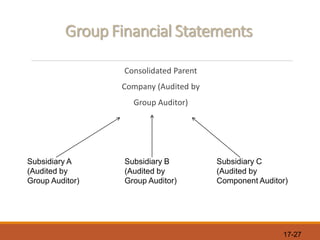

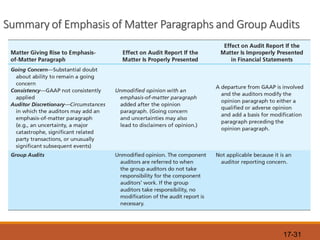

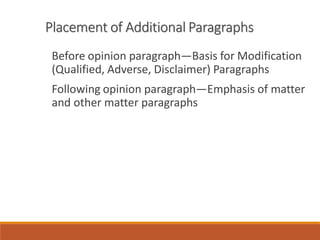

![17-8

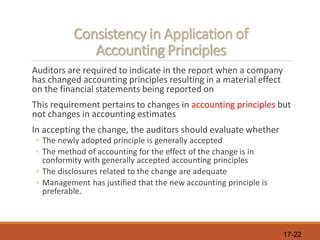

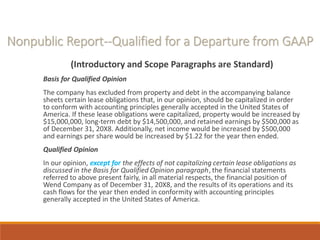

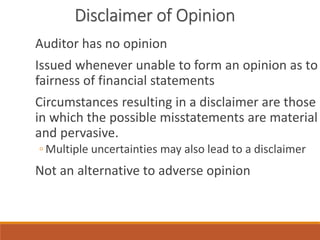

Critical Audit Matters

Critical Audit Matters

The critical audit matters communicated below are matters arising from the current period

audit of the financial statements that were communicated or required to be communicated

to the audit committee and that (1) relate to accounts or disclosures that are material to

the financial statements and (2) involved our especially challenging, subjective, or complex

judgments. The communication of critical audit matters does not alter in any way our

opinion on the financial statements, taken as a whole, and we are not, by communicating

the critical audit matters below, providing separate opinions on the critical audit matters or

on the accounts or disclosures to which they relate.

[Include critical audit matters]

Blue, Gray & Company

Certified Public Accountants

We have served as the Company’s auditor since 20X0.

Los Angeles, California

February 9, 20X8](https://image.slidesharecdn.com/chapterauditreport-191012071953/85/Chapter-audit-report-8-320.jpg)

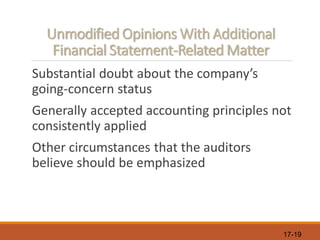

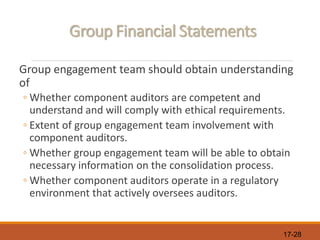

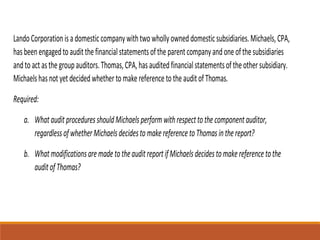

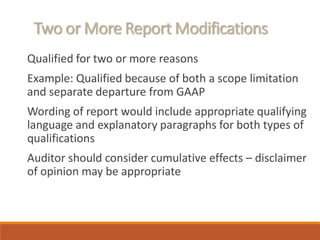

![17-32

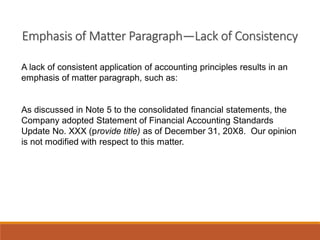

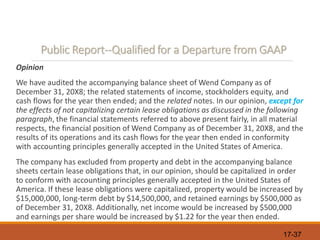

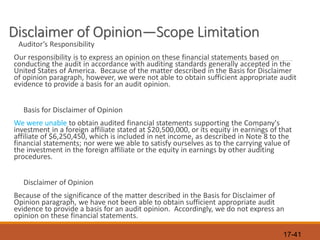

Group Financial Statements

Report:

[Standard introductory paragraph language] We did not audit the financial

statements as and for the year ended December 31, 20x1 of Glendo, Inc.,

which statements reflect total sales constituting 27 percent of total

consolidated sales for 20x1. Those statements were audited by other

auditors whose reports have been furnished to us, and our opinion, insofar as

it relates to data included for Glendo, Inc. for 20x1, is based solely on the

report of the other auditors.

[Standard scope paragraph language] We believe that our audits and the

reports of other auditors provide a reasonable basis for our opinion.

In our opinion, based on our audits and the reports of other auditors, …](https://image.slidesharecdn.com/chapterauditreport-191012071953/85/Chapter-audit-report-32-320.jpg)

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)