Downloaded 21 times

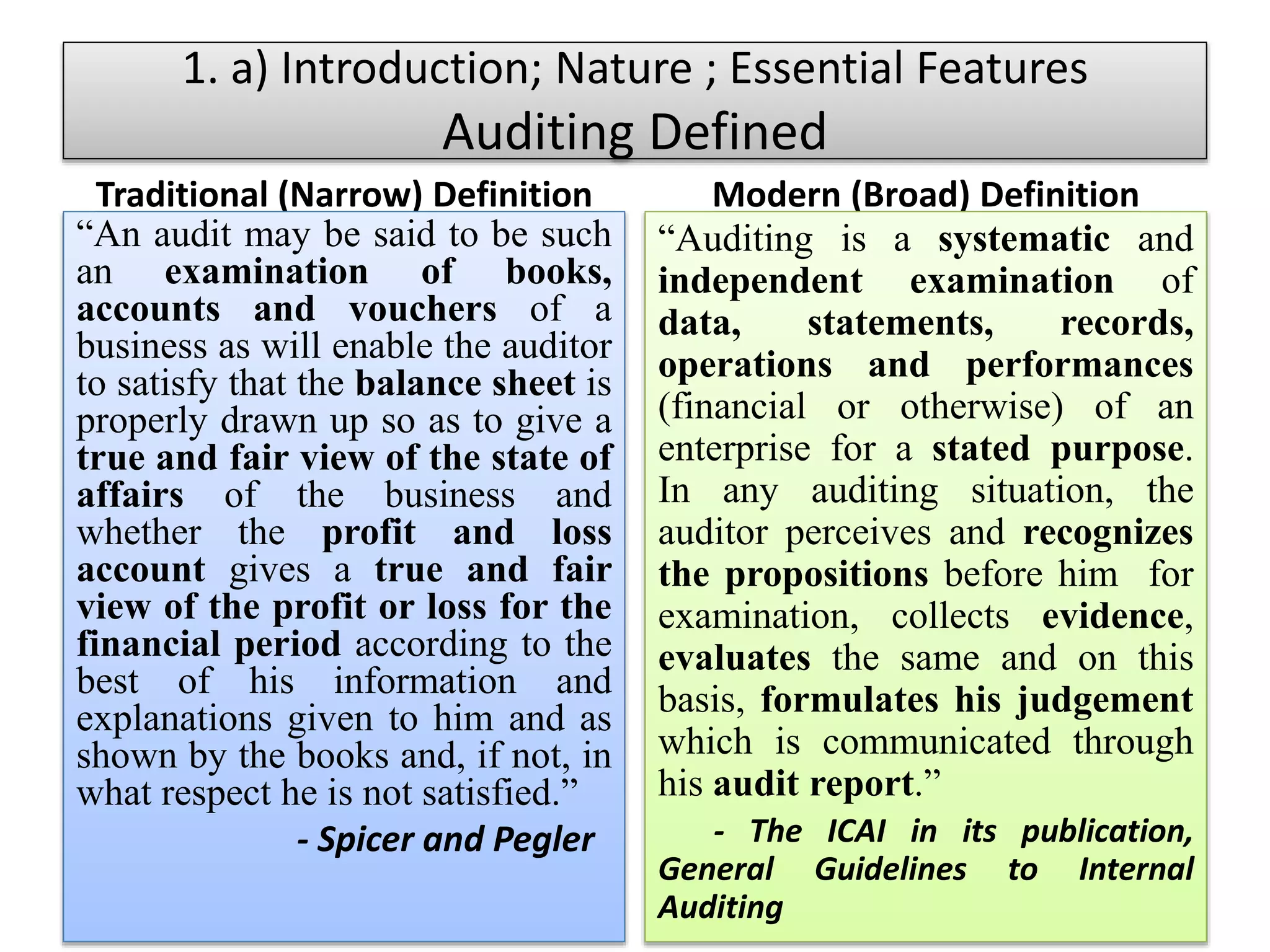

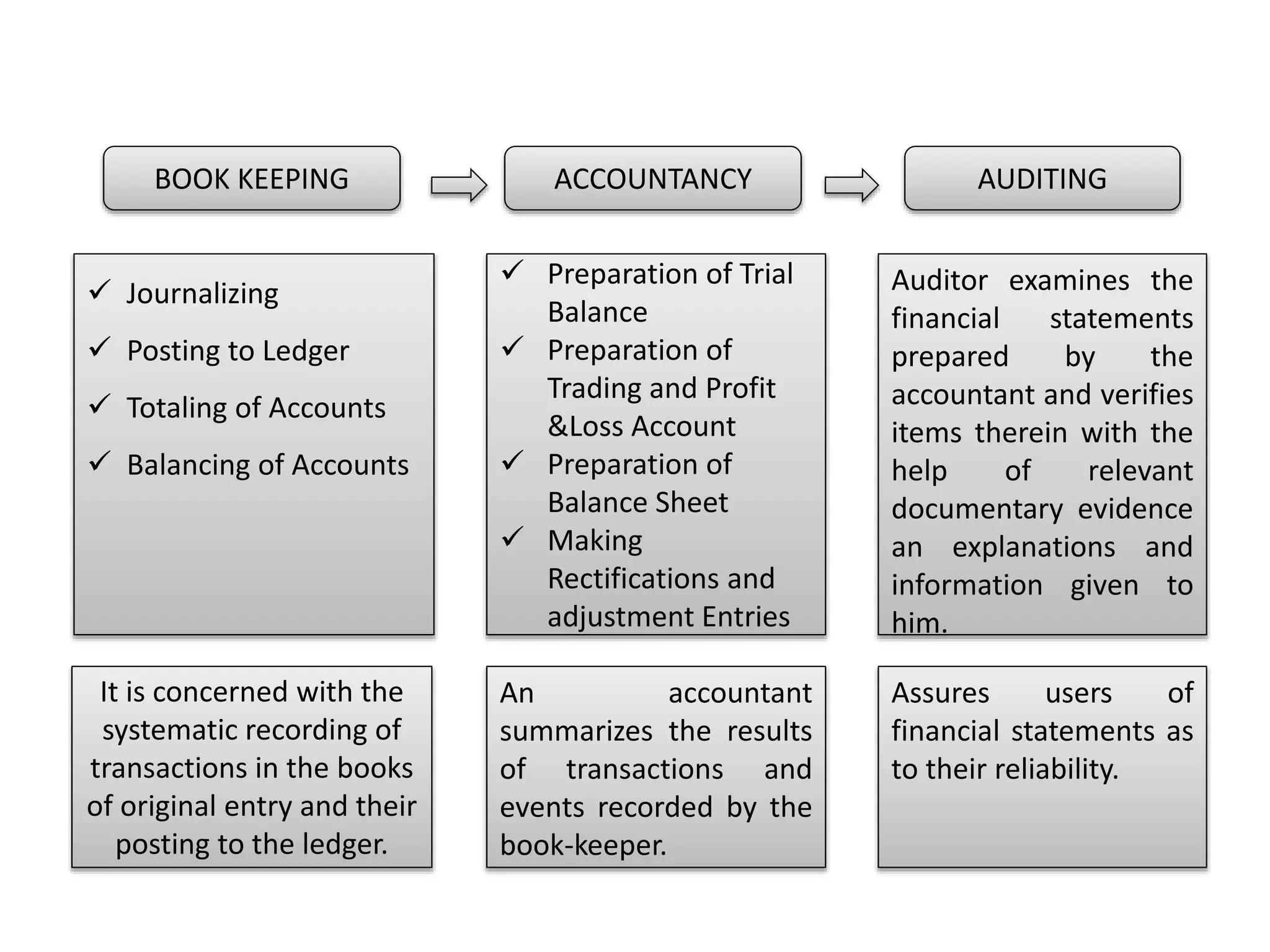

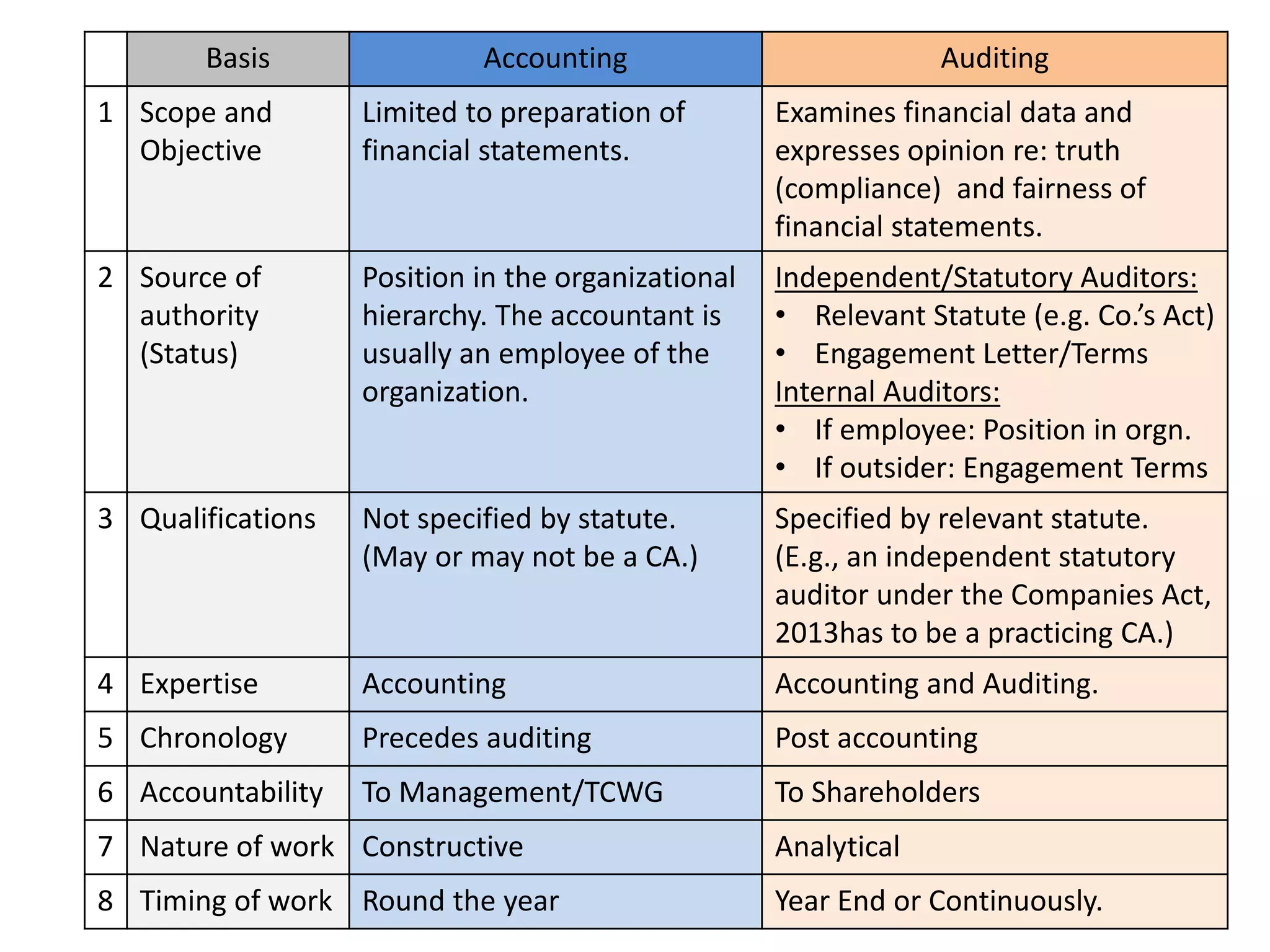

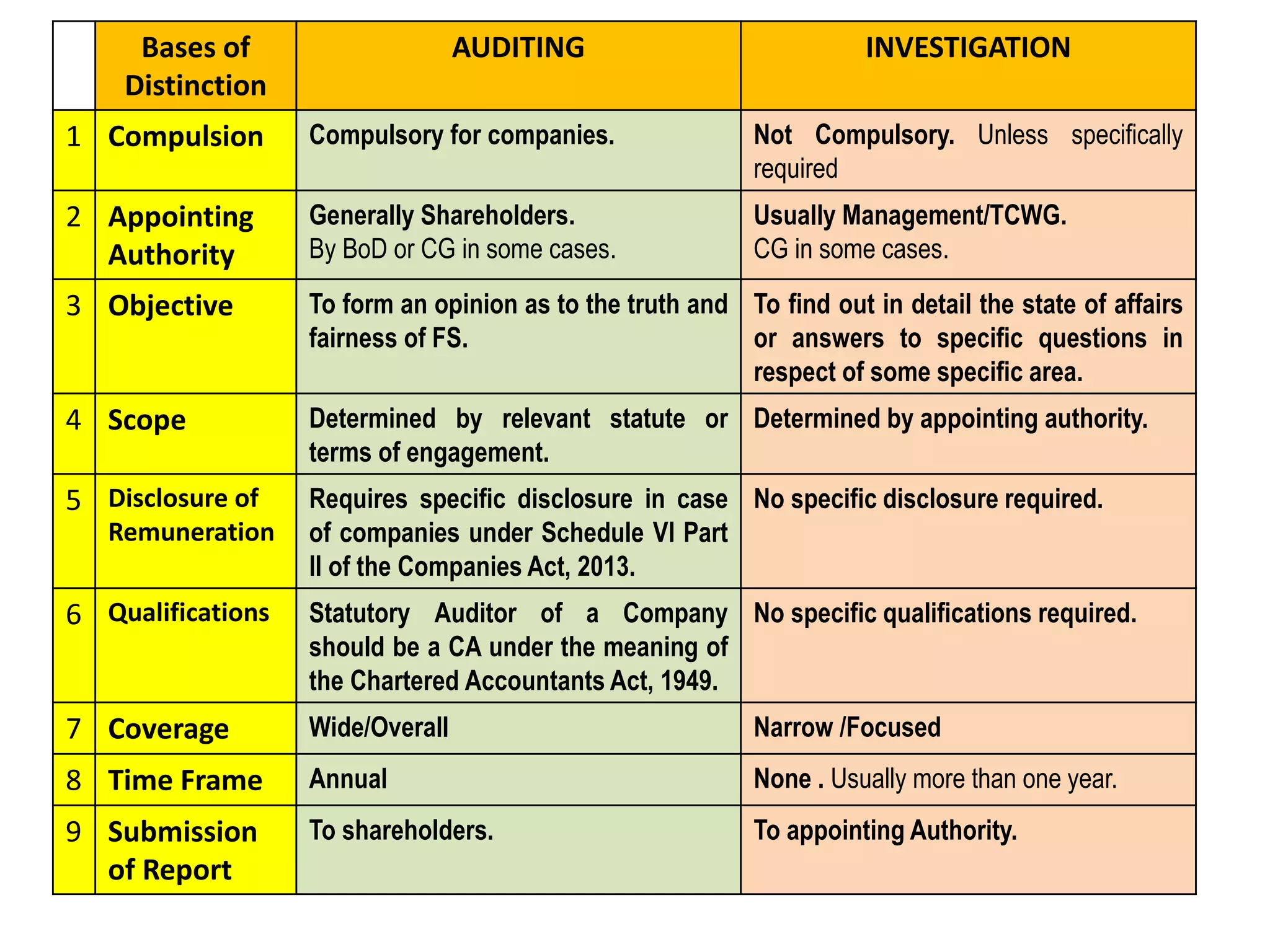

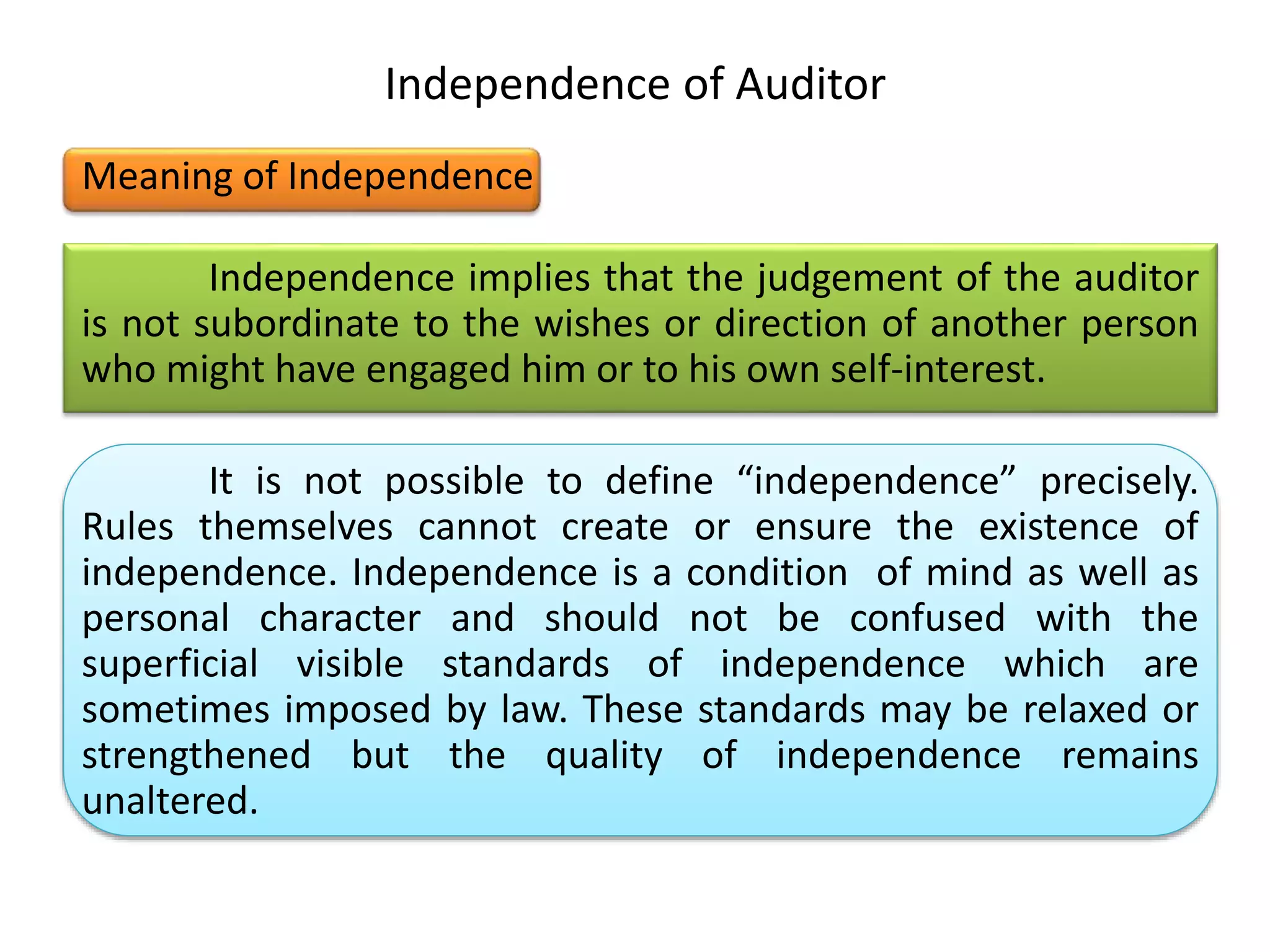

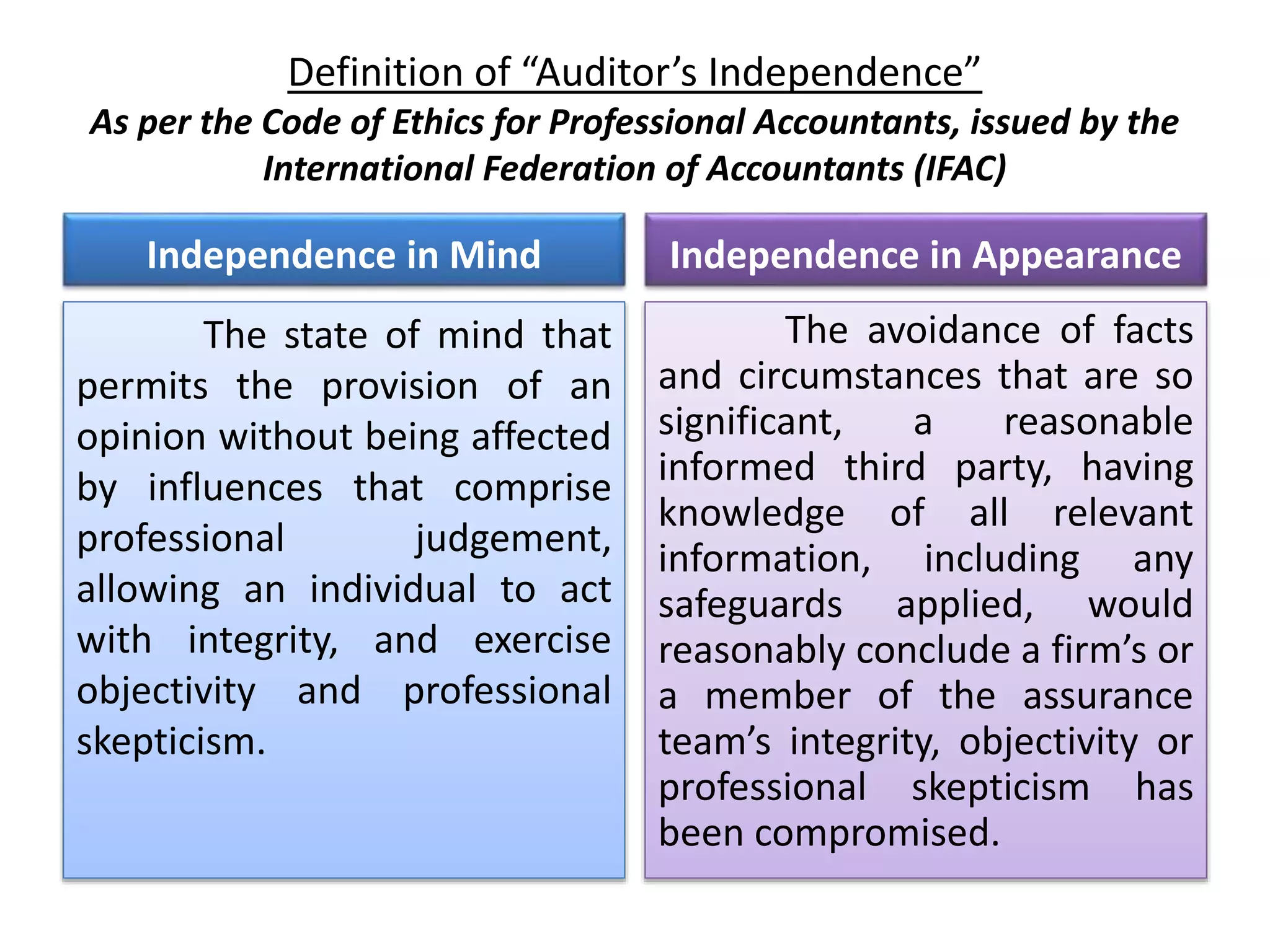

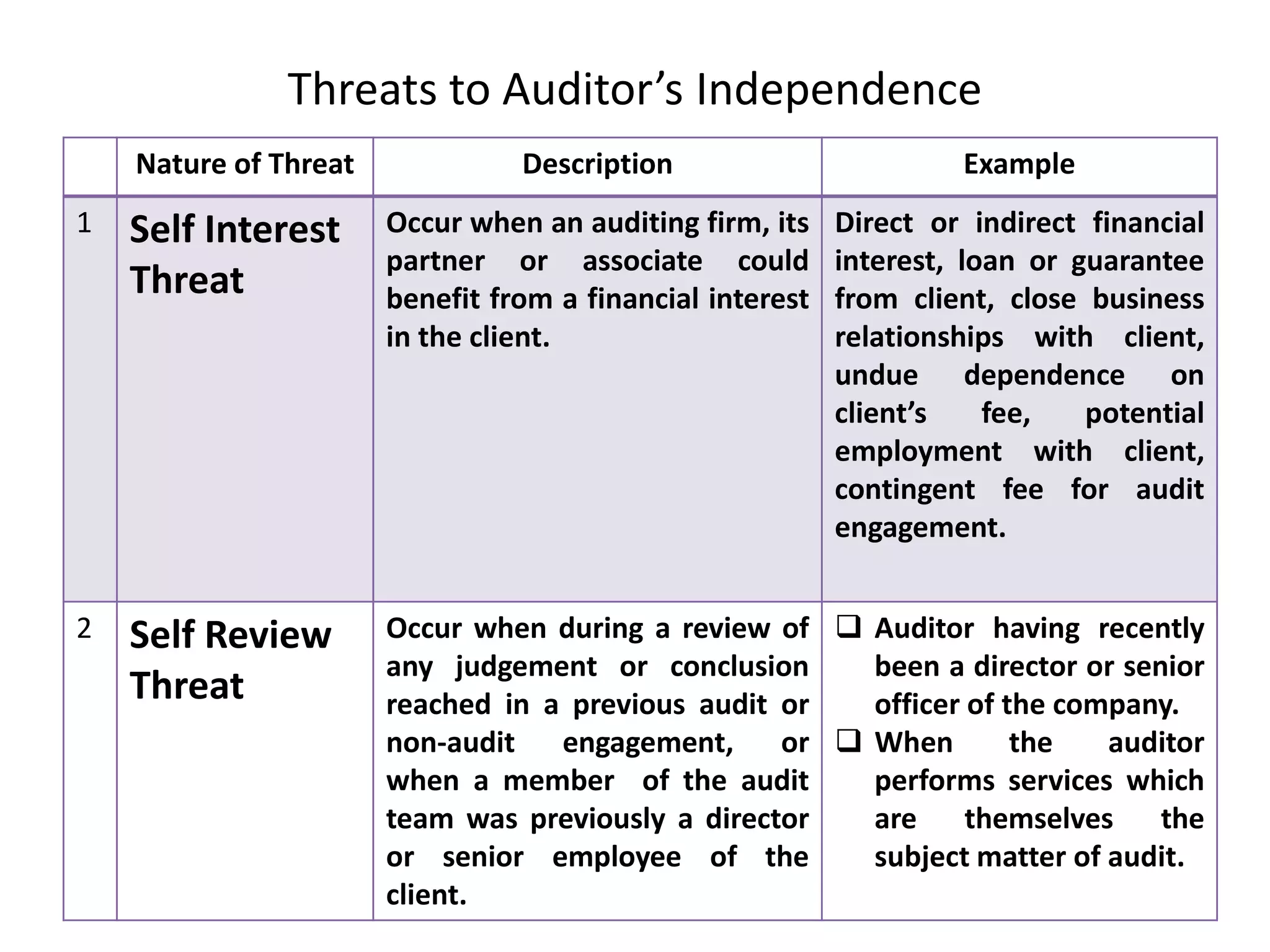

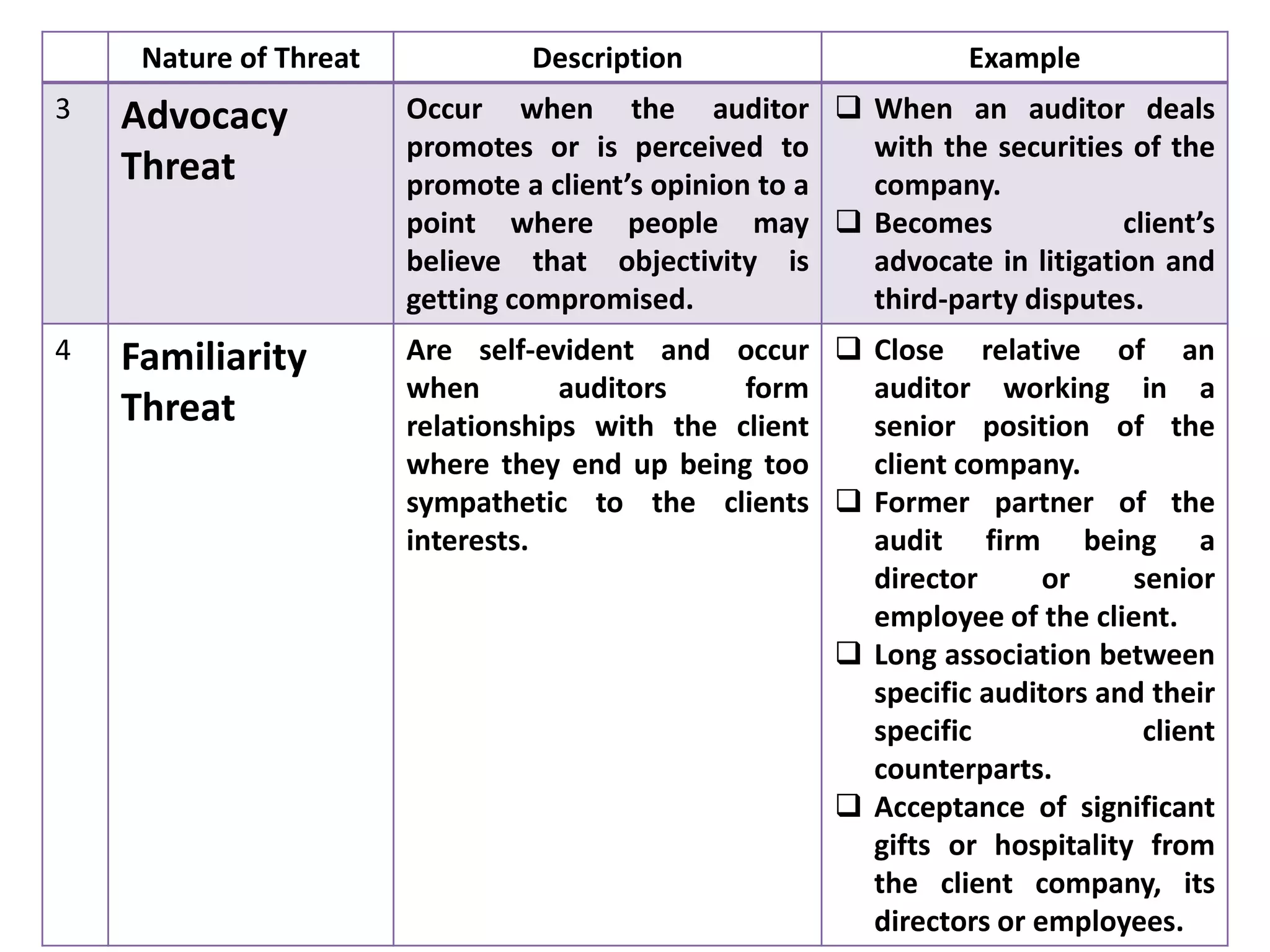

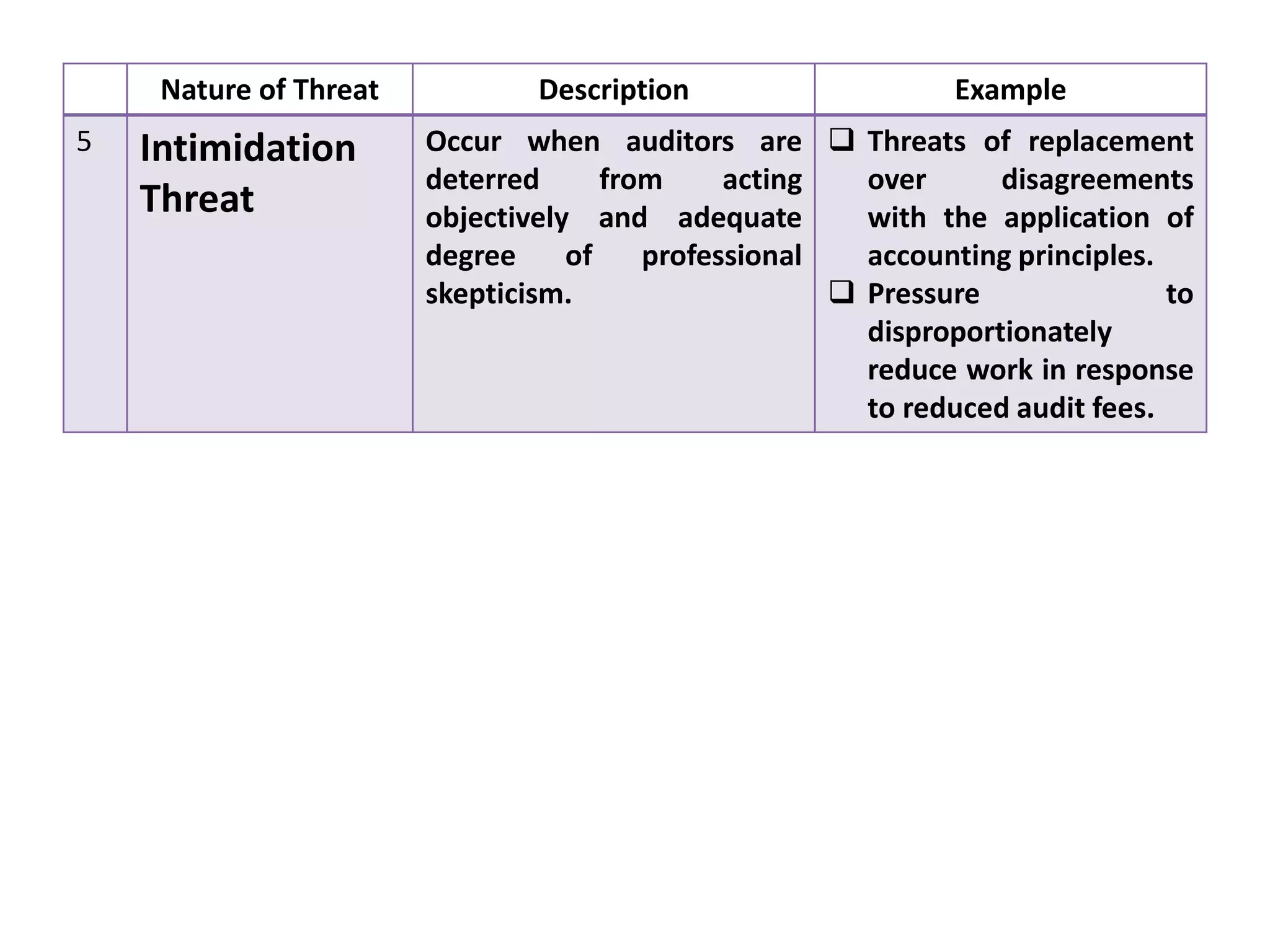

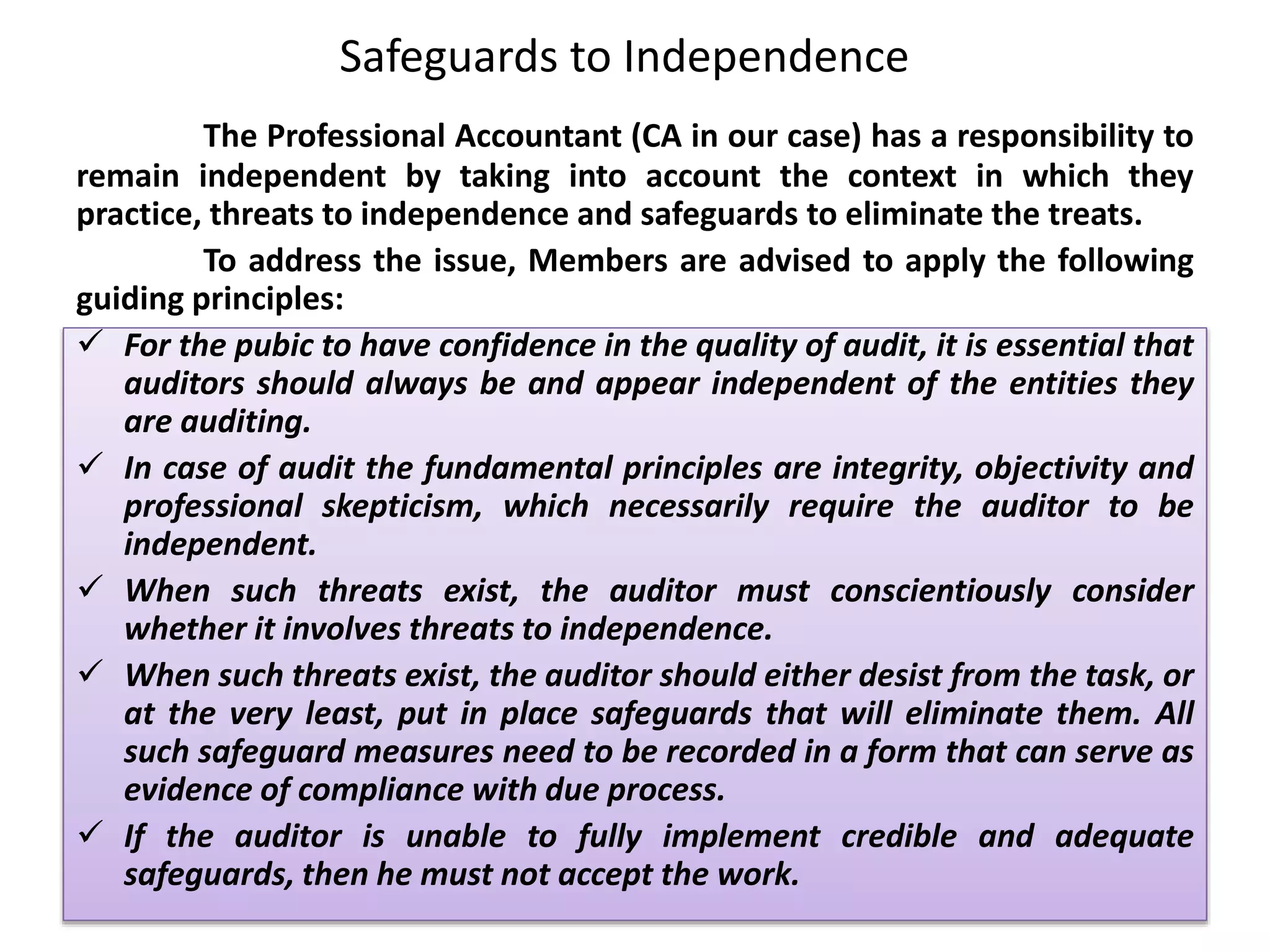

The document discusses the nature of auditing, including its objectives, principles, concepts, scope, and limitations. It defines auditing and distinguishes it from accounting and bookkeeping. Key topics covered include the independence and ethics of auditors, threats to their independence, and safeguards to address such threats.