Downloaded 337 times

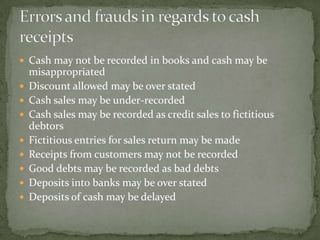

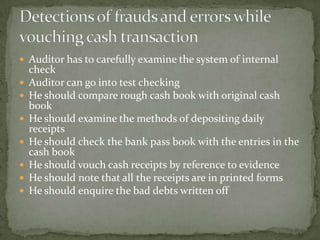

Vouching involves testing the accuracy of transactions recorded in accounting books by examining supporting documentation. It helps auditors ensure transactions are valid, all entries are supported, and nothing has been omitted or misrecorded. Key aspects auditors examine when vouching cash receipts include cash sales records, bank deposit slips, and reconciling receipts to entries in cash books and bank statements. This helps auditors verify revenues have been completely and properly recorded.