Downloaded 1,128 times

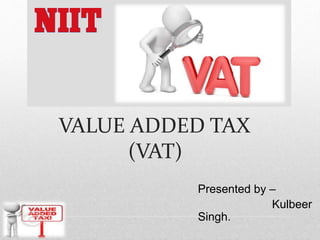

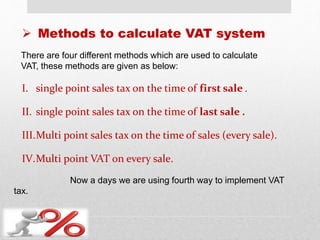

![Retailer (z) Cons (p)

(PUR) 110 (10) 220[10+10] 20 330(10+20) 30

Raw mat+exp 80

+profit 20 90 80

Sales price = 100 200 300

+sales

tax(10%)

10 20 30

Invoice price 110 220 330

reasons

• Double tax (Multi taxation) charged.

• Tax on Tax (cascading effect)

As discussed as earlier, vat comes into existence because

the sales tax was causing couple of problems, these are:](https://image.slidesharecdn.com/valueaddedtax-140608134945-phpapp01/85/Value-added-tax-4-320.jpg)

Value Added Tax (VAT) is an indirect tax on goods imposed by state governments in India, introduced in 1986 to address issues related to sales tax. VAT is a multi-point tax, where it is charged on the value addition at each stage of sale, and includes specific tax rates for different goods. Dealers are categorized as registered, unregistered, or composite based on their annual turnover, with registered dealers eligible for input tax credit and required to remit VAT returns.