Downloaded 221 times

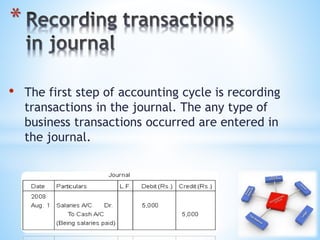

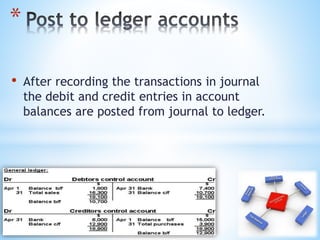

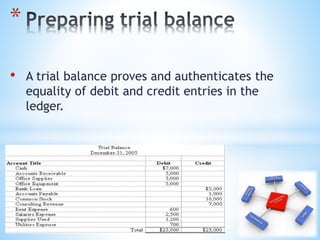

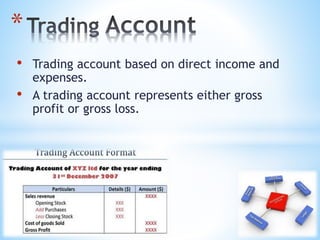

The accounting cycle describes the process of recording, classifying, and summarizing business transactions. It involves sourcing documents, recording transactions in a journal, posting entries to ledgers, preparing a trial balance, and ultimately generating financial statements including a trading and profit/loss account and balance sheet. These steps ensure accuracy and equality between debits and credits.