Downloaded 150 times

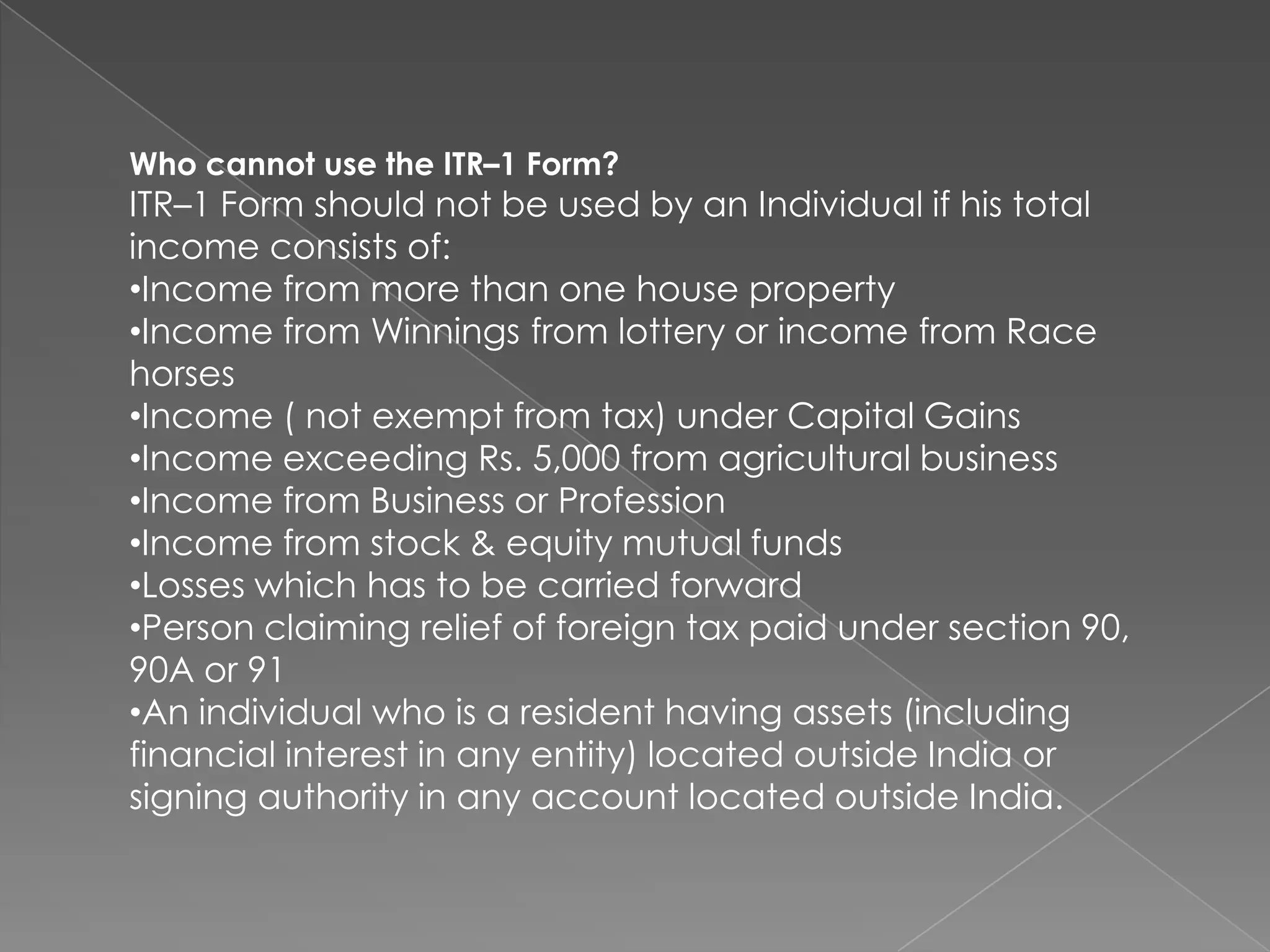

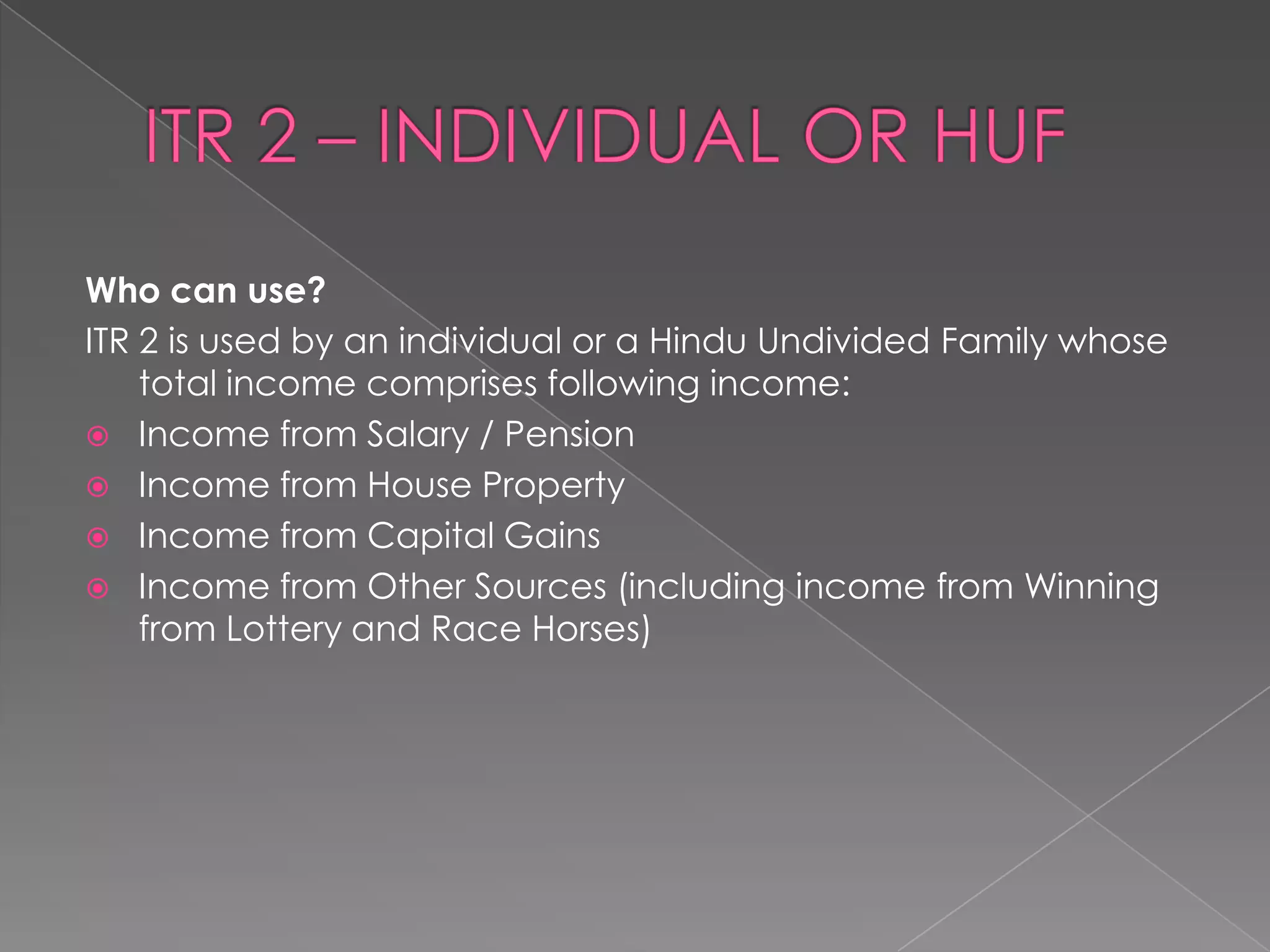

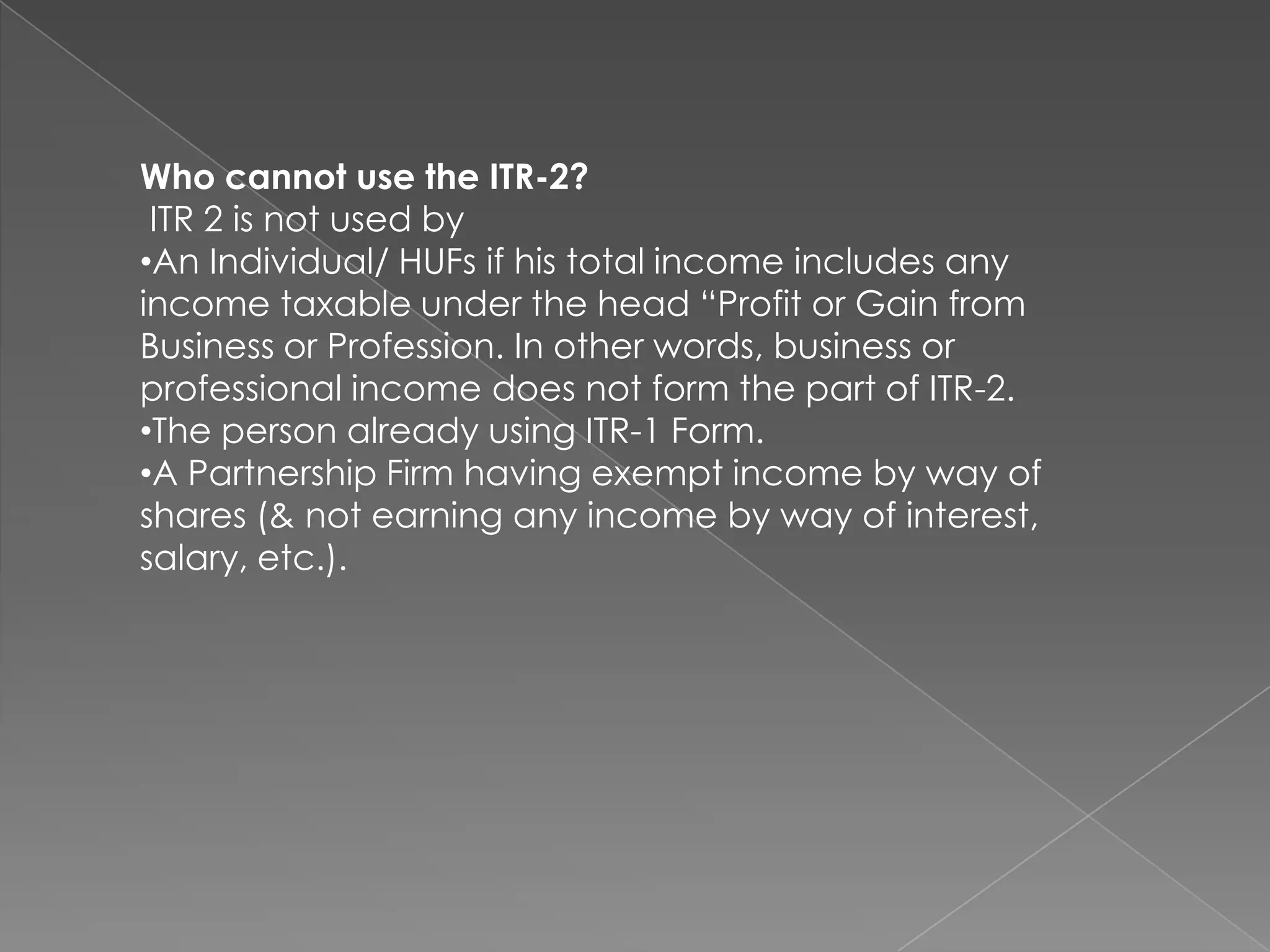

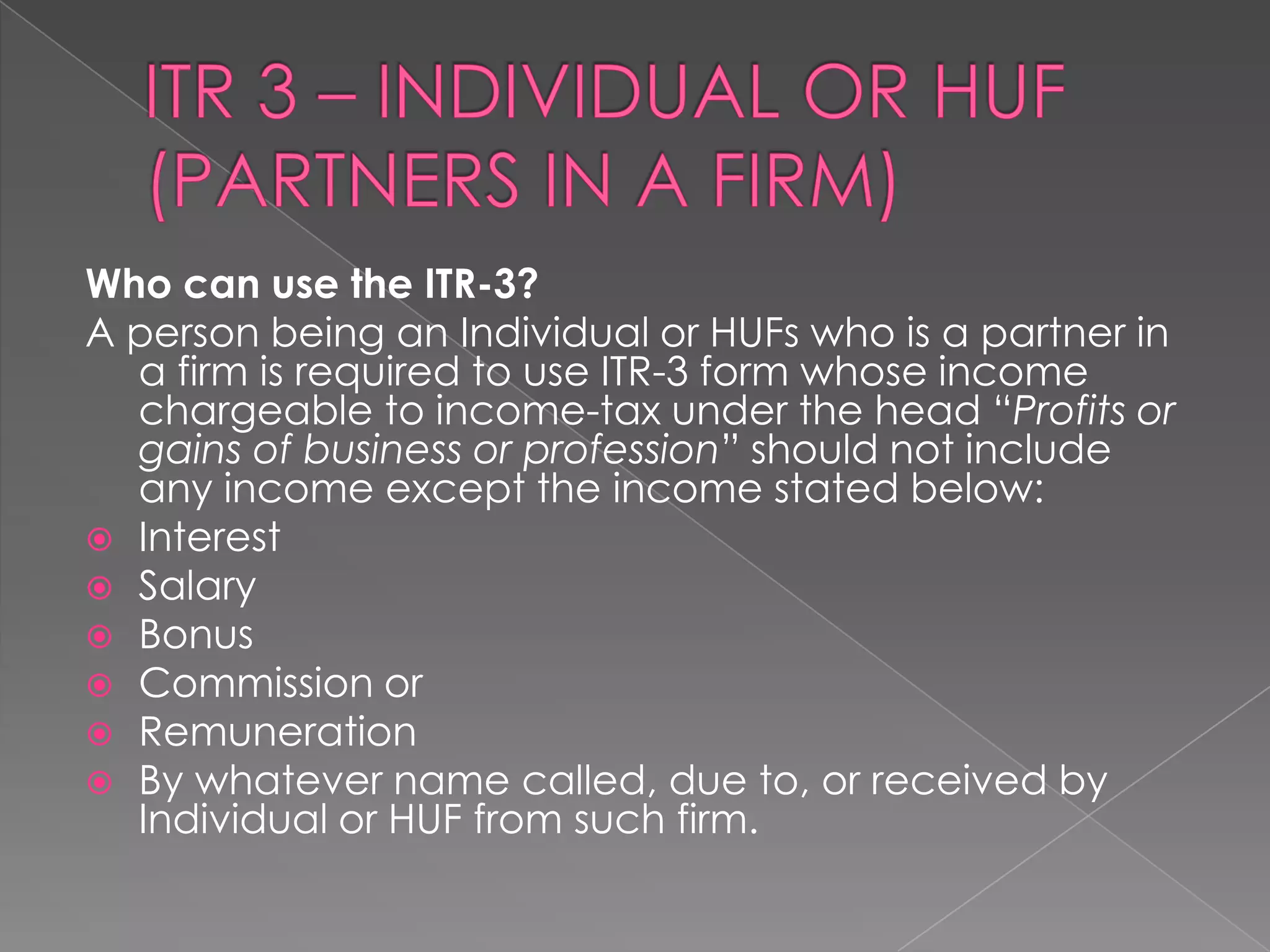

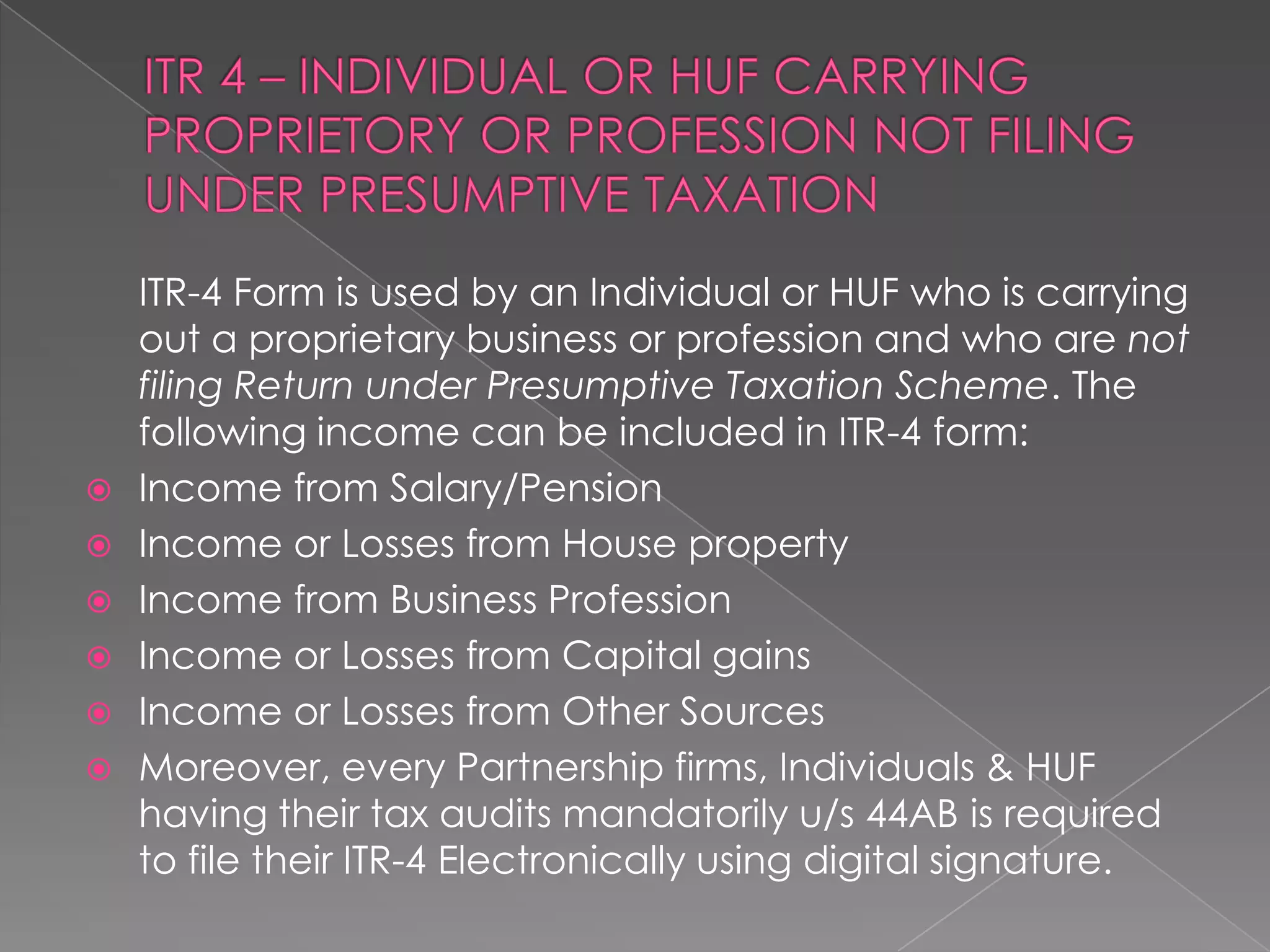

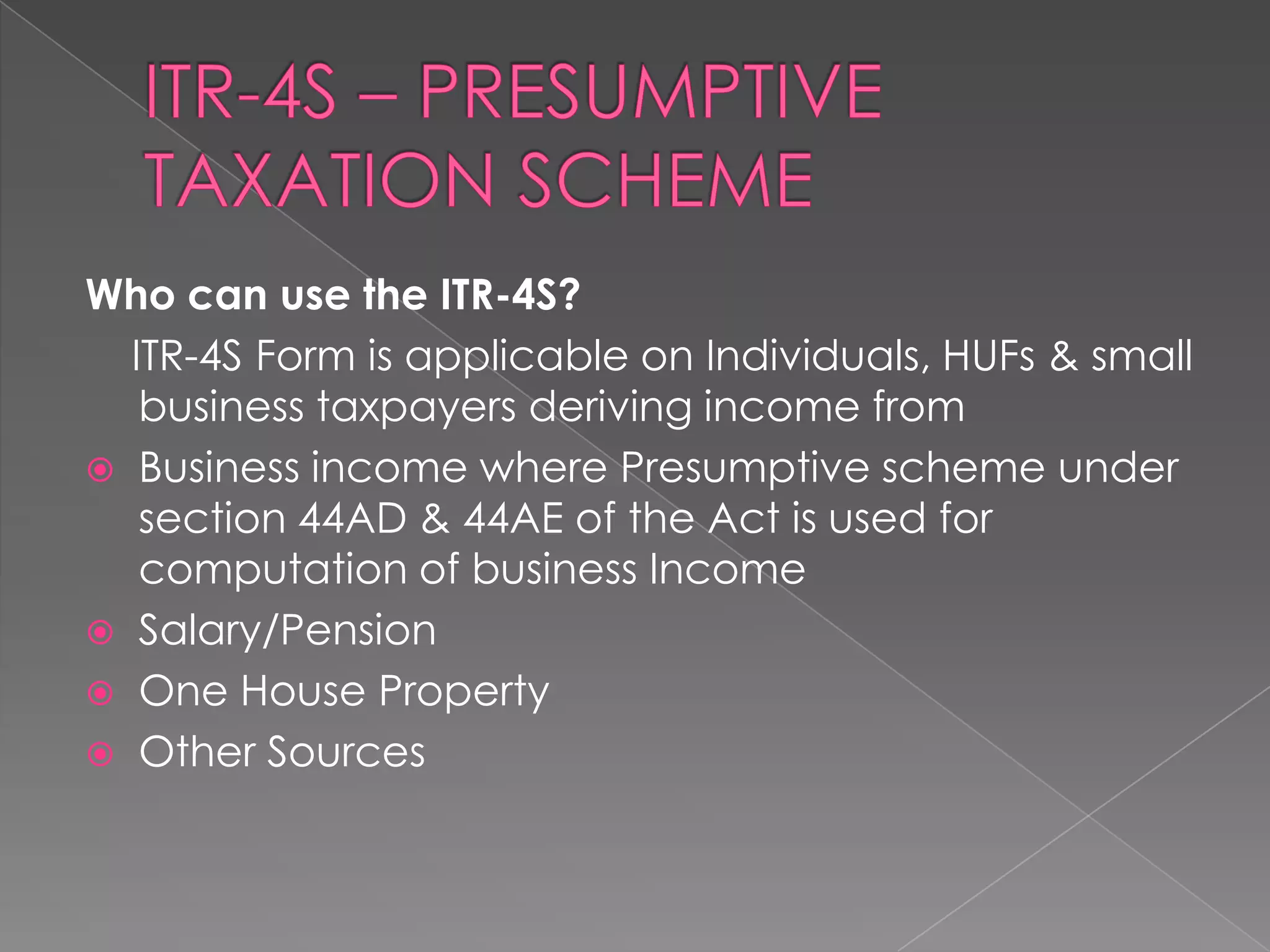

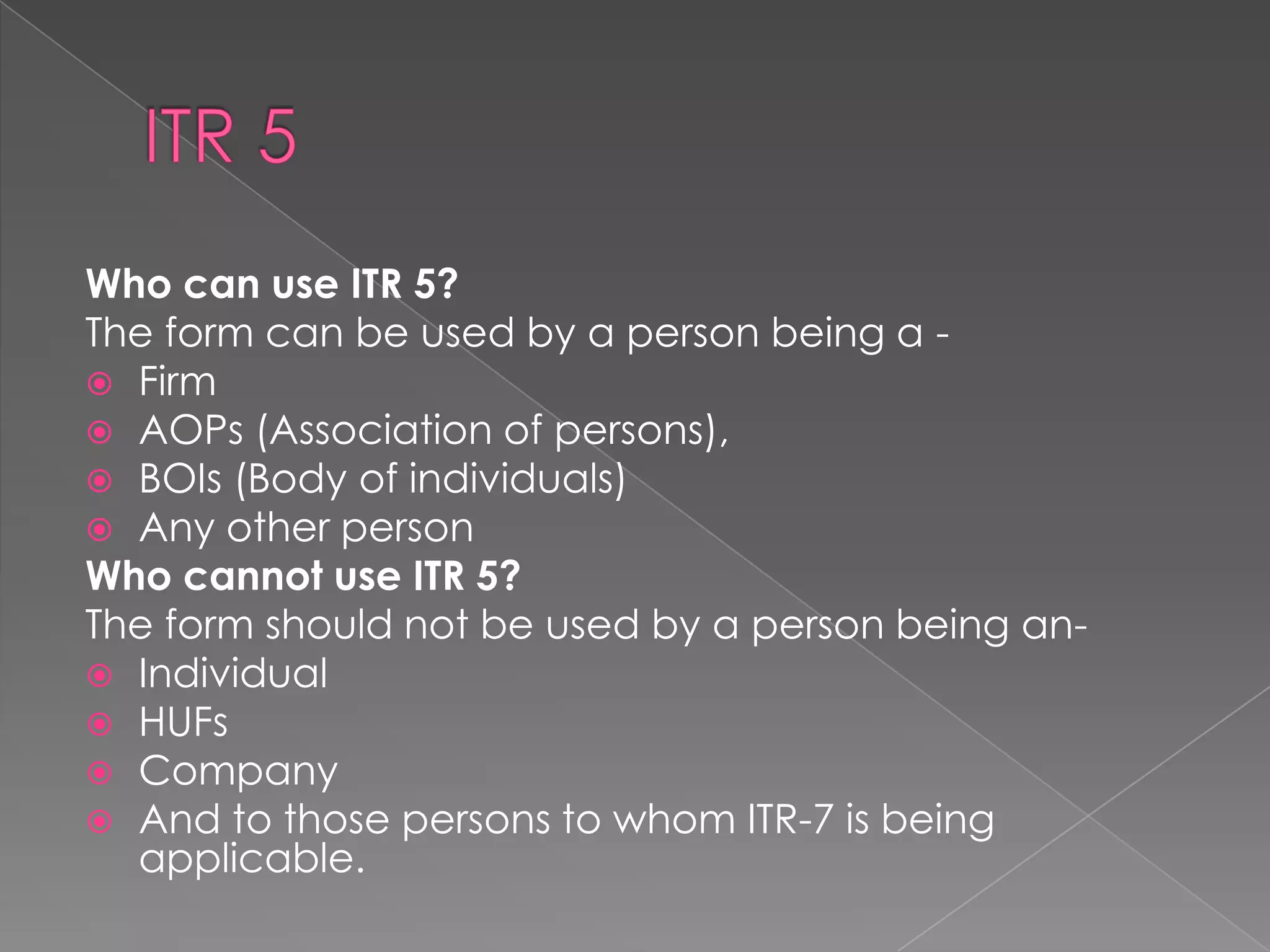

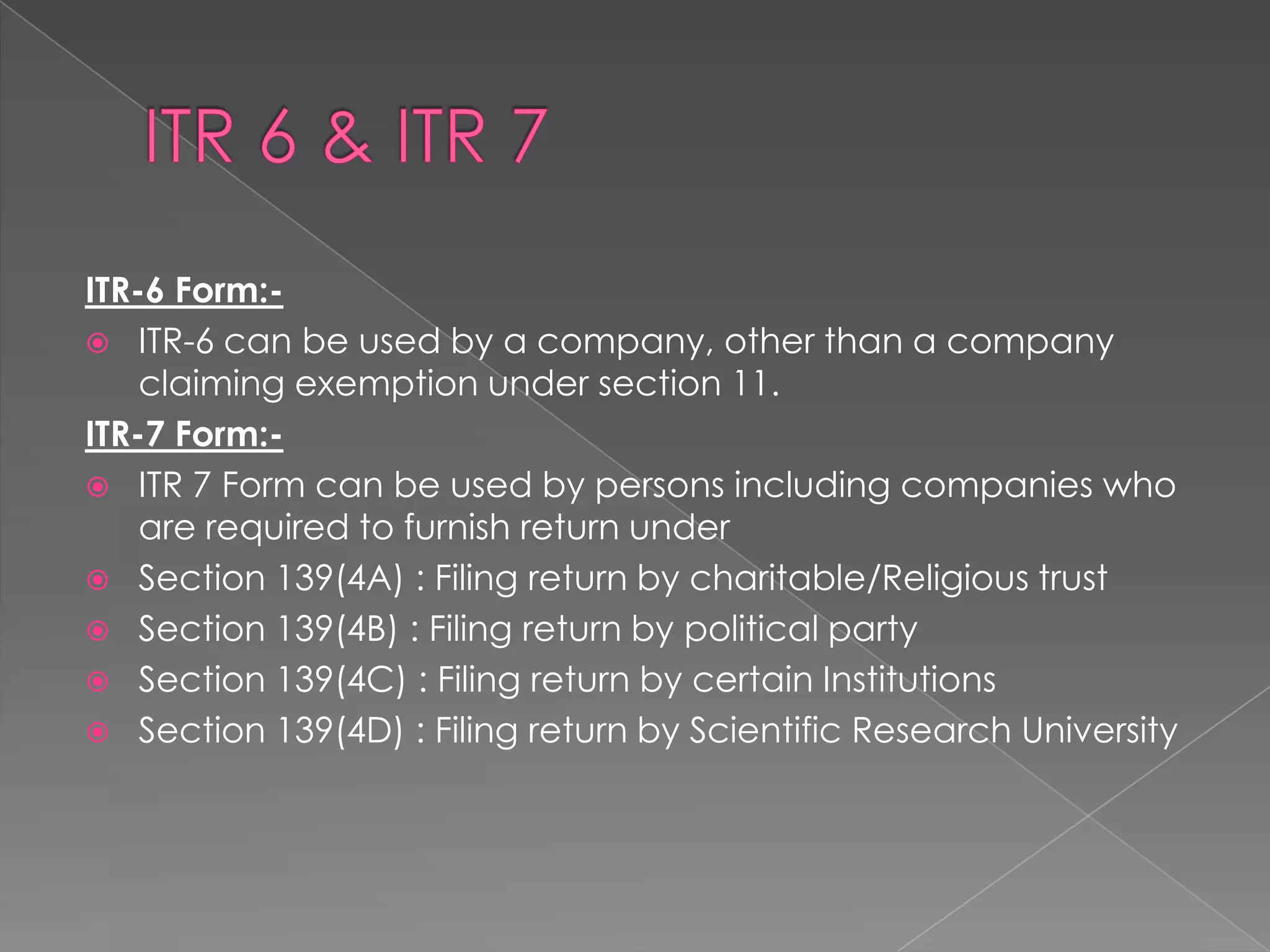

ITR-1 can be used by individuals with income from salary, one house property (without carried forward losses), and other sources excluding lottery/horse race winnings. ITR-2 can be used by individuals and HUFs with income from salary, house property, capital gains, and other sources including lottery/horse races, but excluding business income. ITR-3 must be used by individuals/HUFs who are firm partners with only interest, salary, bonus, commission, or remuneration from the firm. ITR-4 is for individuals/HUFs with proprietary business/profession income. ITR-4S is for small businesses using presumptive taxation. ITR-5 is for firms