This document provides an overview of time series models and concepts. It discusses stochastic processes, stationarity, the Wold decomposition, impulse response analysis, and ARMA processes. The key points are:

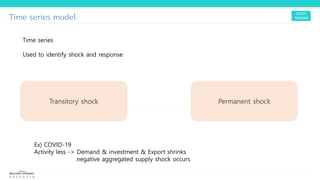

1) Time series models are used to identify shocks and responses over time from stochastic processes.

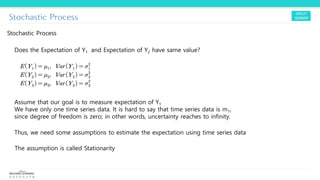

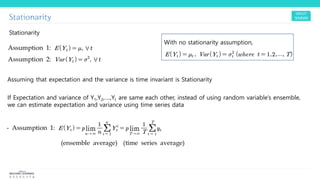

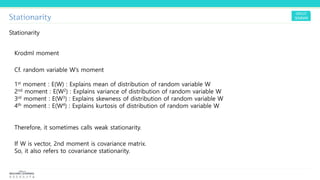

2) Stationarity assumptions are needed to estimate expectations and variances from time series data using the concept that these values are time-invariant.

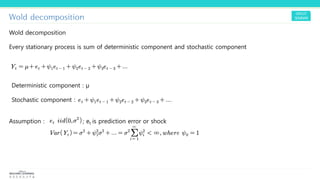

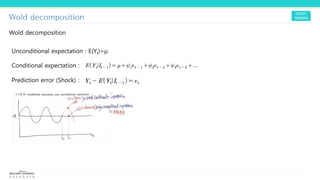

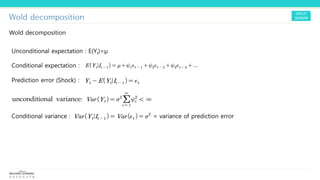

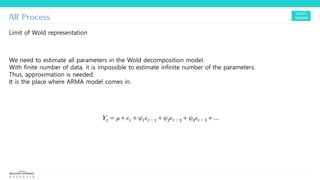

3) The Wold decomposition represents a stationary process as the sum of a deterministic component and stochastic prediction errors/shocks.

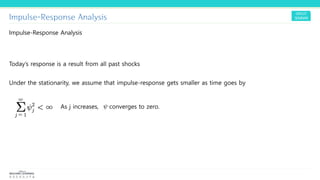

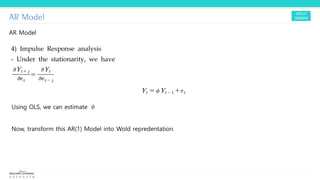

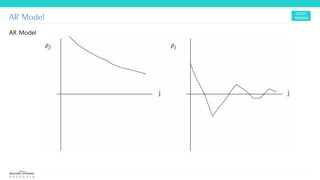

4) Impulse response analysis examines how past shocks continue to impact the present and future through their effect over time which decays as time

![ARIMA Models - [Lab 3]](https://cdn.slidesharecdn.com/ss_thumbnails/ydqcxn5vtqizjoun2as1-signature-e1de5ad681d661531c2467ca0d3e475440809ccfdbcb78c5369a1bb749945888-poli-141230090527-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)