The document discusses the Seasonal ARIMA method for time series analysis, detailing the drawbacks of traditional models and the process of identifying the appropriate ARIMA model using statistical techniques like ACF and PACF. It covers the importance of achieving stationarity through differencing and presents a case study on European quarterly retail trade data to illustrate the application of the Seasonal ARIMA model. Key components include the addition of seasonal terms and the use of R programming for modeling and forecasting.

Drawbacks of TraditionalModels

• There is no systematic approach for the identification and selection of an appropriate

model, and therefore, the identification process is mainly trial-and-error.

• There is difficulty in verifying the validity of the model:

• Most traditional methods were developed from intuitive and practical considerations rather

than from a statistical foundation.

BY JOUD KHATTAB

5.

ARIMA Models

• AutoRegressive Integrated Moving Average.

• A stochastic modeling approach that can be used to calculate the probability of a future

value lying between two specified limits.

BY JOUD KHATTAB

6.

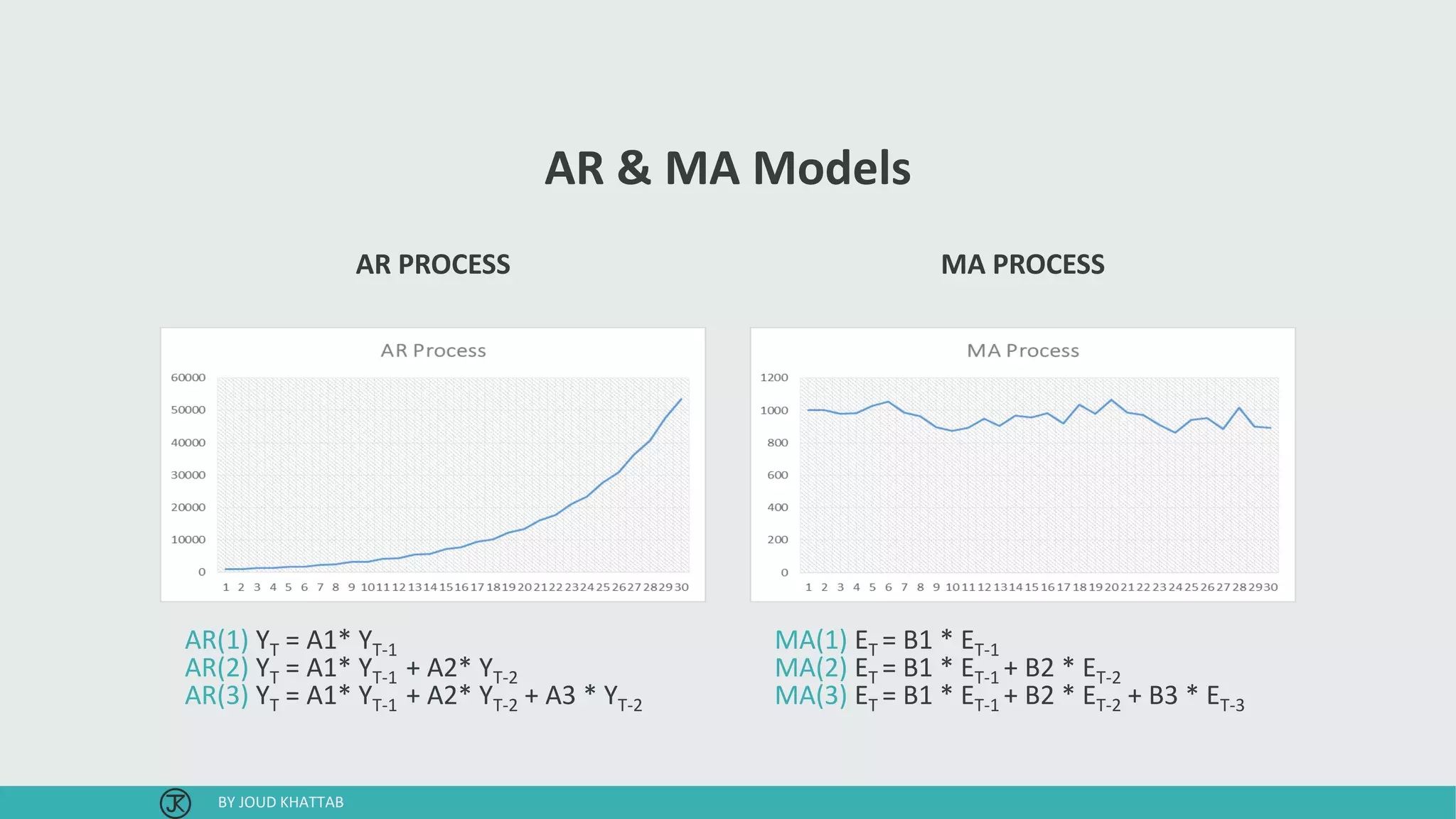

AR & MAModels

• Auto Regressive AR process:

• Series current values depend on its own previous values.

• AR(p) - Current values depend on its own p-previous values.

• P is the order of AR process.

• Moving Average MA process:

• The current deviation from mean depends on previous deviations.

• MA(q) - The current deviation from mean depends on q- previous deviations.

• q is the order of MA process.

• Autoregressive Moving average ARMA process.

BY JOUD KHATTAB

ARIMA (p,d,q) Modeling

•To build a time series model issuing ARIMA, we need to study the time series and

identify p,d,q.

1. Ensuring Stationarity:

• Determine the appropriate values of d.

2. Identification:

• Determine the appropriate values of p & q using the ACF, PACF.

3. Diagnostic checking:

• pick best model with well behaved residuals.

4. Forecasting:

• Produce out of sample forecasts or set aside last few data points for in-sample forecasting.

BY JOUD KHATTAB

9.

Achieving Stationarity

• Astationary time series is one whose statistical properties such as mean, variance,

autocorrelation, etc. are all constant over time.

• Differencing: Transformation of the series to a new time series where the values are the

differences between consecutive values.

• Procedure may be applied consecutively more than once.

BY JOUD KHATTAB

10.

Stationarity Example:

Avoiding CommonMistakes with Time Series

• A basic mantra in statistics and data science is correlation is not causation, meaning

that just because two things appear to be related to each other doesn’t mean that one

causes the other. This is a lesson worth learning.

BY JOUD KHATTAB

11.

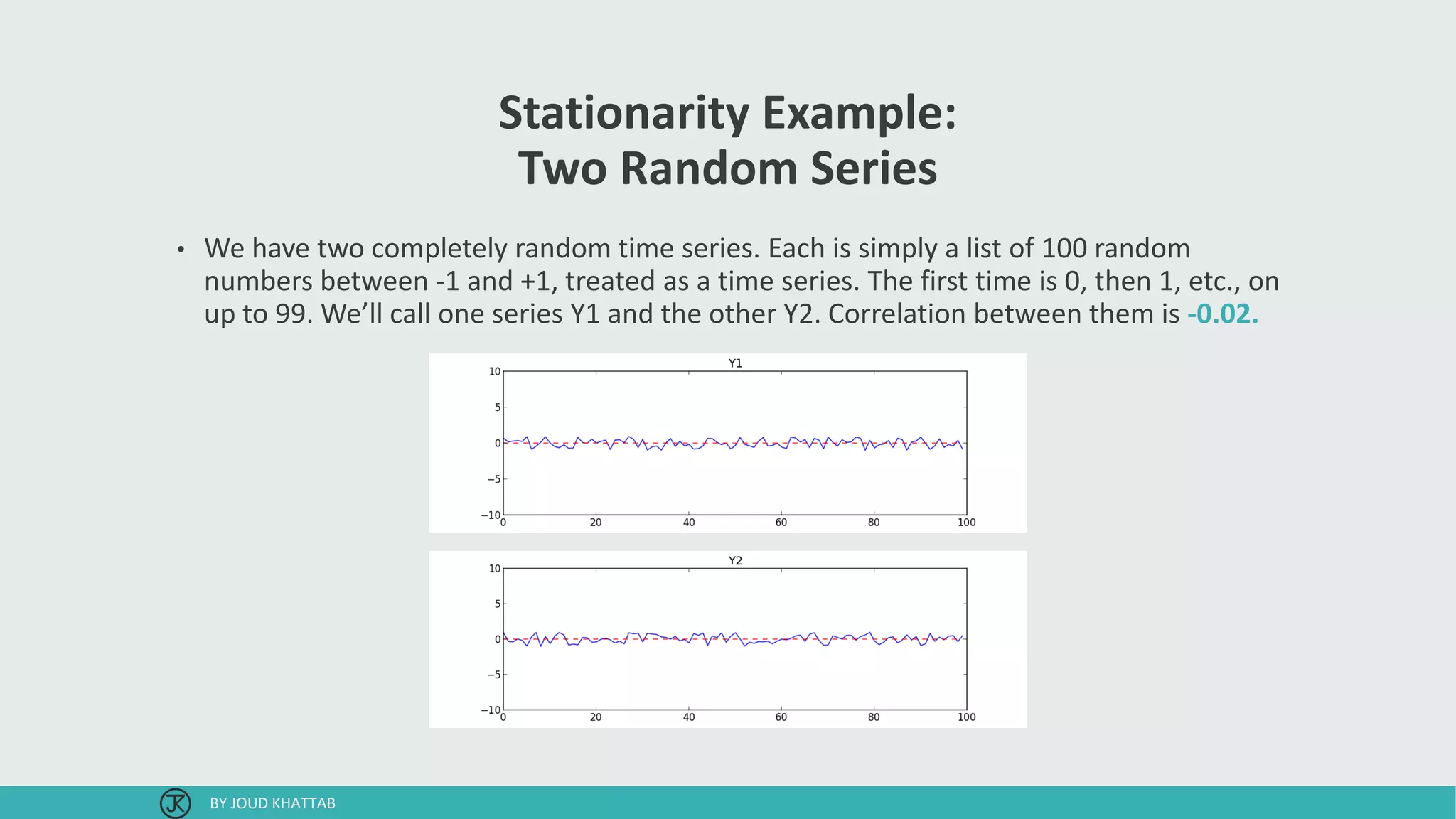

Stationarity Example:

Two RandomSeries

• We have two completely random time series. Each is simply a list of 100 random

numbers between -1 and +1, treated as a time series. The first time is 0, then 1, etc., on

up to 99. We’ll call one series Y1 and the other Y2. Correlation between them is -0.02.

BY JOUD KHATTAB

12.

Stationarity Example:

Adding trend

•Now let’s tweak the time series by adding a slight rise to each. Specifically, to each

series we simply add points from a slightly sloping line from (0,-3) to (99,+3). Now let’s

repeat the same tests on these new series. We get surprising results: the correlation

coefficient is 0.96.

BY JOUD KHATTAB

13.

Stationarity Example:

Dealing WithTrend

• What’s going on? The two time series are no more related than before. By introducing a

trend, we’ve made Y1 dependent on X, and Y2 dependent on X as well. In a time series,

X is time. Correlating Y1 and Y2 will uncover their mutual dependence.

• One such method for removing trend is called first differences. With first differences,

you subtract from each point the point that came before it:

• y'(t) = y(t) – y(t-1)

BY JOUD KHATTAB

Identification “p” and“q” Orders

• We need to learn about ACF & PACF to identify p,q.

• Once we are working with a stationary time series, we can examine the ACF and PACF

to help identify the proper number of lagged y (AR) terms and ε (MA) terms.

BY JOUD KHATTAB

16.

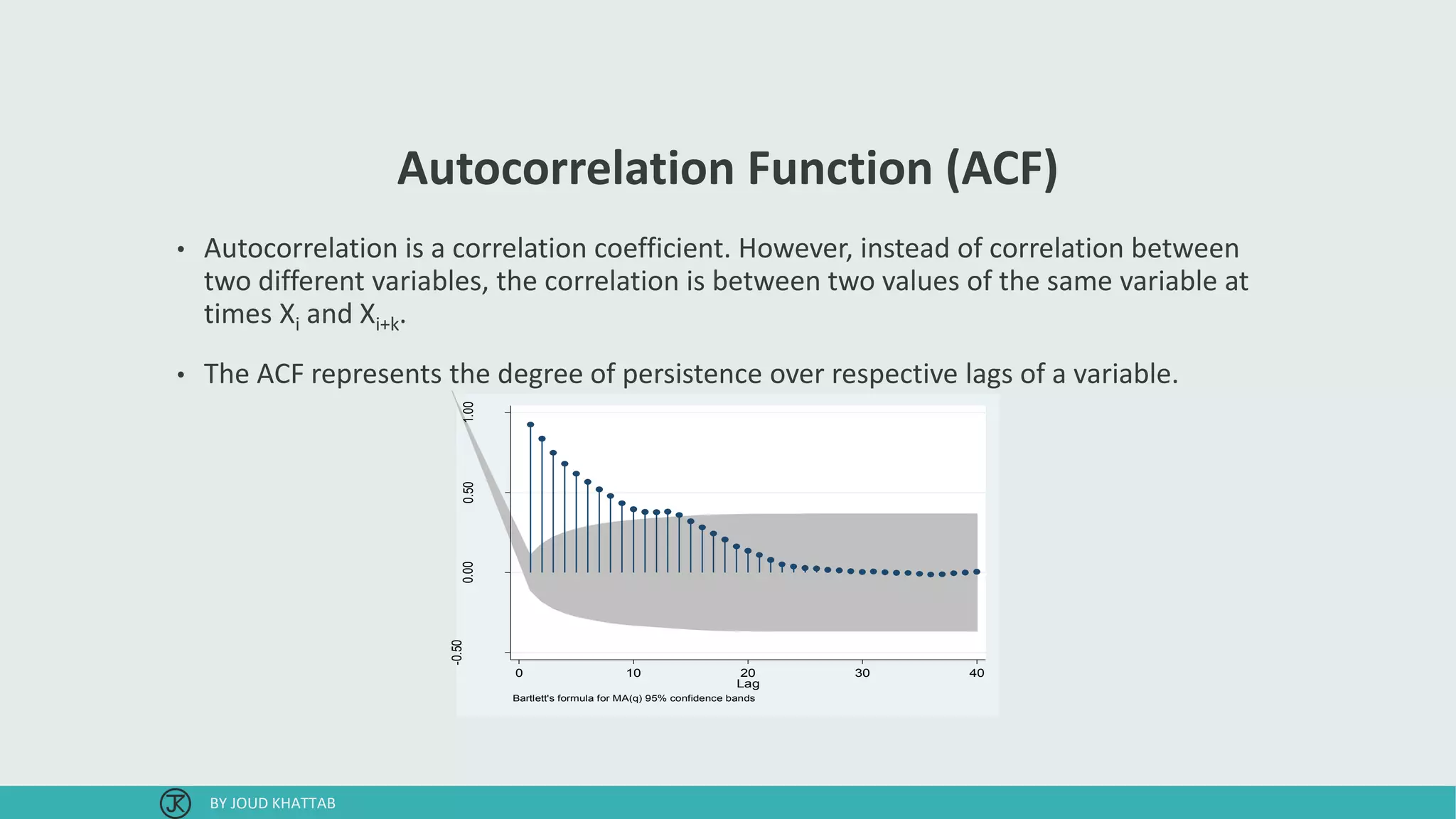

Autocorrelation Function (ACF)

•Autocorrelation is a correlation coefficient. However, instead of correlation between

two different variables, the correlation is between two values of the same variable at

times Xi and Xi+k.

• The ACF represents the degree of persistence over respective lags of a variable.

-0.50

0.000.501.00

Autocorrelationsofpresap

0 10 20 30 40

Lag

Bartlett's formula for MA(q) 95% confidence bands

BY JOUD KHATTAB

17.

Partial Autocorrelation Function(PACF)

• Partial correlation measures the degree of association between two random variables,

with the effect of a set of controlling random variables removed.

-0.50

0.000.501.00

Partialautocorrelationsofpresap

0 10 20 30 40

Lag

95% Confidence bands [se = 1/sqrt(n)]

BY JOUD KHATTAB

18.

Identification of ARProcesses & its order (p)

• For AR models, the ACF will dampen exponentially.

• The PACF will identify the order of the AR model:

• The AR(1) model would have one significant spike at lag 1 on the PACF.

• The AR(3) model would have significant spikes on the PACF at lags 1, 2, & 3.

-0.50

0.000.501.00

Autocorrelationsofpresap

0 10 20 30 40

Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.50

0.000.501.00

Partialautocorrelationsofpresap

0 10 20 30 40

Lag

95% Confidence bands [se = 1/sqrt(n)]

BY JOUD KHATTAB

19.

Identification of MAProcesses & its order (q)

• The PACF will dampen exponentially.

• The ACF will be used to identify the order of the MA process.

• The MA(1) has one significant spike in the ACF at lag 1.

• The MA(3) has three significant spikes in the ACF at lags 1, 2, & 3.

-0.50

0.000.501.00

Autocorrelationsofpresap

0 10 20 30 40

Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.50

0.000.501.00

Partialautocorrelationsofpresap

0 10 20 30 40

Lag

95% Confidence bands [se = 1/sqrt(n)]

BY JOUD KHATTAB

Seasonal Time Series

•A seasonal pattern exists when a series is influenced by seasonal factors (e.g., the

quarter of the year, the month, or day of the week). Seasonality is always of a fixed and

known period.

BY JOUD KHATTAB

23.

Seasonal ARIMA

• Aseasonal ARIMA model is formed by including additional seasonal terms in the

ARIMA models we have seen so far. It is written as follows:

• Where m = number of periods per season.

• We use uppercase notation for the seasonal parts of the model, and lowercase notation

for the non-seasonal parts of the model.

BY JOUD KHATTAB

24.

Seasonal ARIMA

• Theseasonal part consists of terms that are very similar to the non-seasonal

components of the model, but they involve backshifts of the seasonal period.

• For example, an ARIMA(1,1,1)(1,1,1)4 model is for quarterly data (m=4).

• The additional seasonal terms are simply multiplied with the non-seasonal terms.

BY JOUD KHATTAB

25.

ACF & PACF

•The seasonal part of an AR or MA model will be seen in the seasonal lags of the PACF and

ACF.

• For example, an ARIMA(0,0,0)(0,0,1)12 model will show:

• A spike at lag 12 in the ACF but no other significant spikes.

• The PACF will show exponential decay in the seasonal lags; that is, at lags 12, 24, 36, ….

• Similarly, an ARIMA(0,0,0)(1,0,0)12 model will show:

• Exponential decay in the seasonal lags of the ACF.

• A single significant spike at lag 12 in the PACF.

• In considering the appropriate seasonal orders for an ARIMA model, restrict attention to the

seasonal lags.

• The modelling procedure is almost the same as for non-seasonal data, except that we need

to select seasonal AR and MA terms as well as the non-seasonal components of the model.

BY JOUD KHATTAB

European Quarterly RetailTrade

• We will describe the seasonal ARIMA modelling procedure using quarterly European

retail trade data from 1996 to 2011.

• We will use Forecast Library in R studio.

plot(euretail, ylab="Retail index", xlab="Year")

BY JOUD KHATTAB

29.

Make It Stationary

•The data are clearly non-stationary, with some seasonality, so we will first take a

seasonal difference.

tsdisplay( diff(euretail,4) )

BY JOUD KHATTAB

30.

Make It Stationary

•These also appear to be non-stationary, and so we take an additional first difference.

tsdisplay( diff( diff(euretail,4) ) )

BY JOUD KHATTAB

31.

Find Appropriate ARIMAModel

• Based on the ACF and PACF shown:

• The significant spike at lag 1 in the ACF

suggests a non-seasonal MA(1)

component.

• The significant spike at lag 4 in the ACF

suggests a seasonal MA(1) component.

• Consequently, we begin with an

ARIMA(0,1,1)(0,1,1)4 model, indicating

a first and seasonal difference, and

non-seasonal and seasonal MA(1)

components.

BY JOUD KHATTAB

32.

Find Appropriate ARIMAModel

ARIMA(0,1,1)(0,1,1)4

• Both the ACF and PACF show significant

spikes at lag 2, and almost significant

spikes at lag 3, indicating some

additional non-seasonal terms need to

be included in the model.

• The AICc of:

• ARIMA(0,1,2)(0,1,1)4 model is 74.36.

• ARIMA(0,1,3)(0,1,1)4 model is 68.53.

• We tried other models with AR terms

as well, but none that gave a smaller

AICc value.

fit <- Arima(euretail, order=c(0,1,1), seasonal=c(0,1,1))

tsdisplay(residuals(fit))

BY JOUD KHATTAB

33.

Find Appropriate ARIMAModel

ARIMA(0,1,3)(0,1,1)4

• All the spikes are now within the

significance limits, and so the residuals

appear to be white noise.

• A Ljung-Box test also shows that the

residuals have no remaining

autocorrelations.

fit3 <- Arima(euretail, order=c(0,1,3), seasonal=c(0,1,1))

res <- tsdisplay(residuals(fit3))

Box.test(res, lag=16, fitdf=4, type="Ljung")

BY JOUD KHATTAB

34.

Forecast Model

• Forecastsfrom the model for the next

six years as shown.

• Notice how the forecasts follow the

recent trend in the data (this occurs

because of the double differencing).

• The large and rapidly increasing

prediction intervals show that the retail

trade index could start increasing or

decreasing at any time while the point

forecasts trend downwards.

plot( forecast(fit3, h=24) )

BY JOUD KHATTAB

35.

Forecast Without Seasonality

fit<- Arima(euretail, order=c(1,2,0))

tsdisplay(residuals(fit))

plot(forecast(fit, h=24))

BY JOUD KHATTAB

36.

Find Appropriate ARIMAModel

Other Method

• We could have used auto.arima() to do

most of this work for us. It would have

given the following result.

> auto.arima(euretail, stepwise=FALSE,

approximation=FALSE)

ARIMA(0,1,3)(0,1,1)[4]

Coefficients:

ma1 ma2 ma3 sma1

0.2625 0.3697 0.4194 -0.6615

s.e. 0.1239 0.1260 0.1296 0.1555

sigma^2 estimated as 0.1451: log likeliho

od=-28.7

AIC=67.4 AICc=68.53 BIC=77.78

BY JOUD KHATTAB

![Partial Autocorrelation Function (PACF)

• Partial correlation measures the degree of association between two random variables,

with the effect of a set of controlling random variables removed.

-0.50

0.000.501.00

Partialautocorrelationsofpresap

0 10 20 30 40

Lag

95% Confidence bands [se = 1/sqrt(n)]

BY JOUD KHATTAB](https://image.slidesharecdn.com/sarima-170726162611/75/Seasonal-ARIMA-17-2048.jpg)

![Identification of AR Processes & its order (p)

• For AR models, the ACF will dampen exponentially.

• The PACF will identify the order of the AR model:

• The AR(1) model would have one significant spike at lag 1 on the PACF.

• The AR(3) model would have significant spikes on the PACF at lags 1, 2, & 3.

-0.50

0.000.501.00

Autocorrelationsofpresap

0 10 20 30 40

Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.50

0.000.501.00

Partialautocorrelationsofpresap

0 10 20 30 40

Lag

95% Confidence bands [se = 1/sqrt(n)]

BY JOUD KHATTAB](https://image.slidesharecdn.com/sarima-170726162611/75/Seasonal-ARIMA-18-2048.jpg)

![Identification of MA Processes & its order (q)

• The PACF will dampen exponentially.

• The ACF will be used to identify the order of the MA process.

• The MA(1) has one significant spike in the ACF at lag 1.

• The MA(3) has three significant spikes in the ACF at lags 1, 2, & 3.

-0.50

0.000.501.00

Autocorrelationsofpresap

0 10 20 30 40

Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.50

0.000.501.00

Partialautocorrelationsofpresap

0 10 20 30 40

Lag

95% Confidence bands [se = 1/sqrt(n)]

BY JOUD KHATTAB](https://image.slidesharecdn.com/sarima-170726162611/75/Seasonal-ARIMA-19-2048.jpg)

![Find Appropriate ARIMA Model

Other Method

• We could have used auto.arima() to do

most of this work for us. It would have

given the following result.

> auto.arima(euretail, stepwise=FALSE,

approximation=FALSE)

ARIMA(0,1,3)(0,1,1)[4]

Coefficients:

ma1 ma2 ma3 sma1

0.2625 0.3697 0.4194 -0.6615

s.e. 0.1239 0.1260 0.1296 0.1555

sigma^2 estimated as 0.1451: log likeliho

od=-28.7

AIC=67.4 AICc=68.53 BIC=77.78

BY JOUD KHATTAB](https://image.slidesharecdn.com/sarima-170726162611/75/Seasonal-ARIMA-36-2048.jpg)

![[DSC Europe 25] Dusan Jovicic - AI Story: From on-prem to cloud and back agai...](https://cdn.slidesharecdn.com/ss_thumbnails/8kp49m6uq22ifnbwhfnk-2-251205085715-964d11a6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Vid Stimac - Policy Parsimony: Between Oversimplifying and Ov...](https://cdn.slidesharecdn.com/ss_thumbnails/eqlepagzqp2rhg3gbluh-dsc-stimac-251120-251205090438-059e7f54-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Bogdan Daniel Maruneac - AI - It starts with you.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/odov3snhrcqs9hx5ny2n-4-251205085715-f1daacfe-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Dragana Ilic - AI for Big Data in Astronomy.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/8palya86qaatvjhva1ms-2-dragana-ilic-ai-ilic-251208151906-652b819c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Max Talanov - Non digital NNs.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/wif8tr3gtua74qvtopke-non-digital-nns-251205090438-26b0eea6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Marija Vlajkovic & Andrea Radonjanin - Integration of AI tool...](https://cdn.slidesharecdn.com/ss_thumbnails/qf1jrglttoc3bm8s3aop-final-integration-of-ai-tools-251208151905-394f3a6a-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Petar Zivanov - AI meets documents From chatbots to AI-powere...](https://cdn.slidesharecdn.com/ss_thumbnails/xer2bb6nrdc8pdpev0pc-8-251204082258-7c2fa4a1-thumbnail.jpg?width=640&height=640&fit=bounds)