Downloaded 84 times

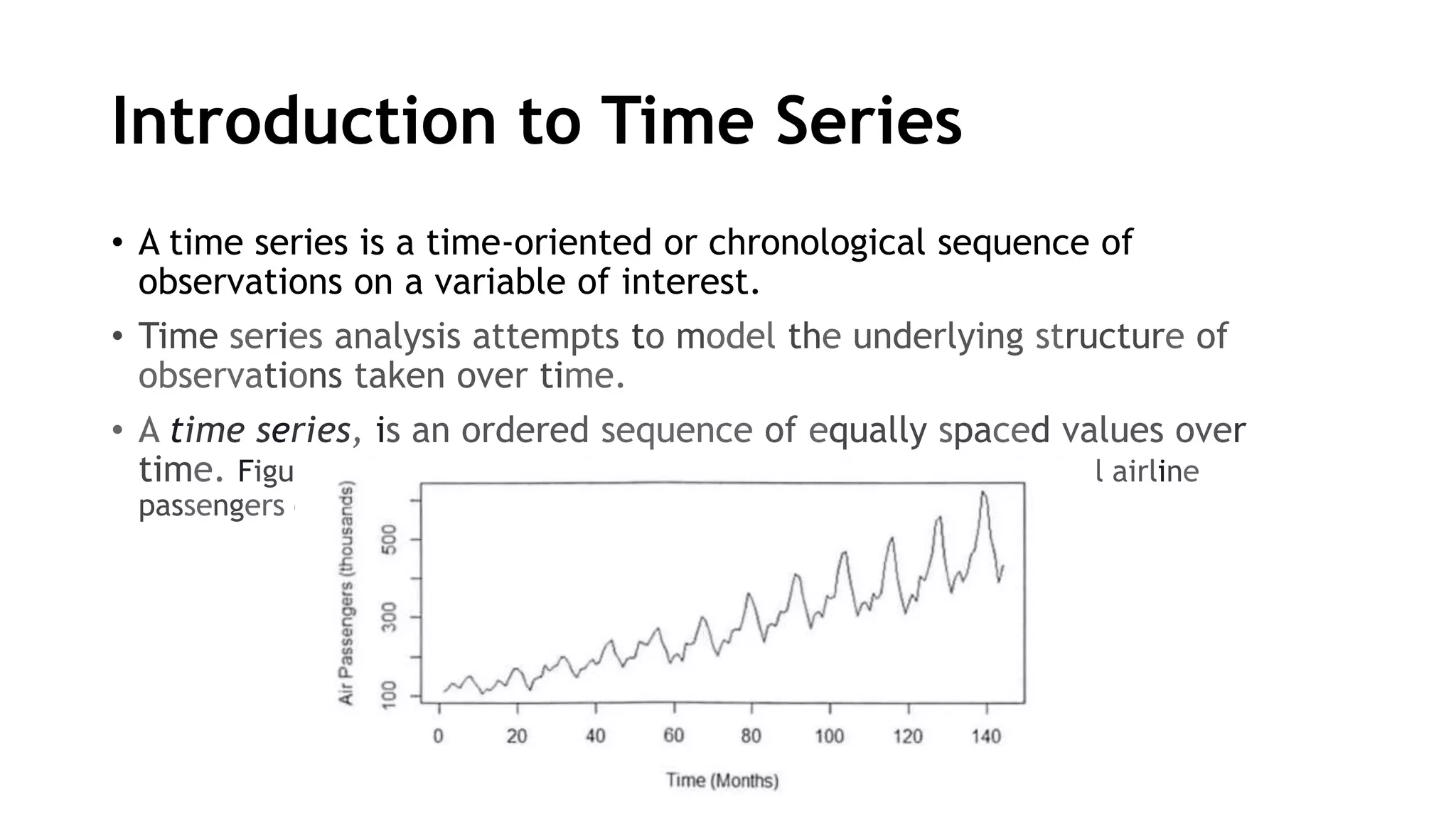

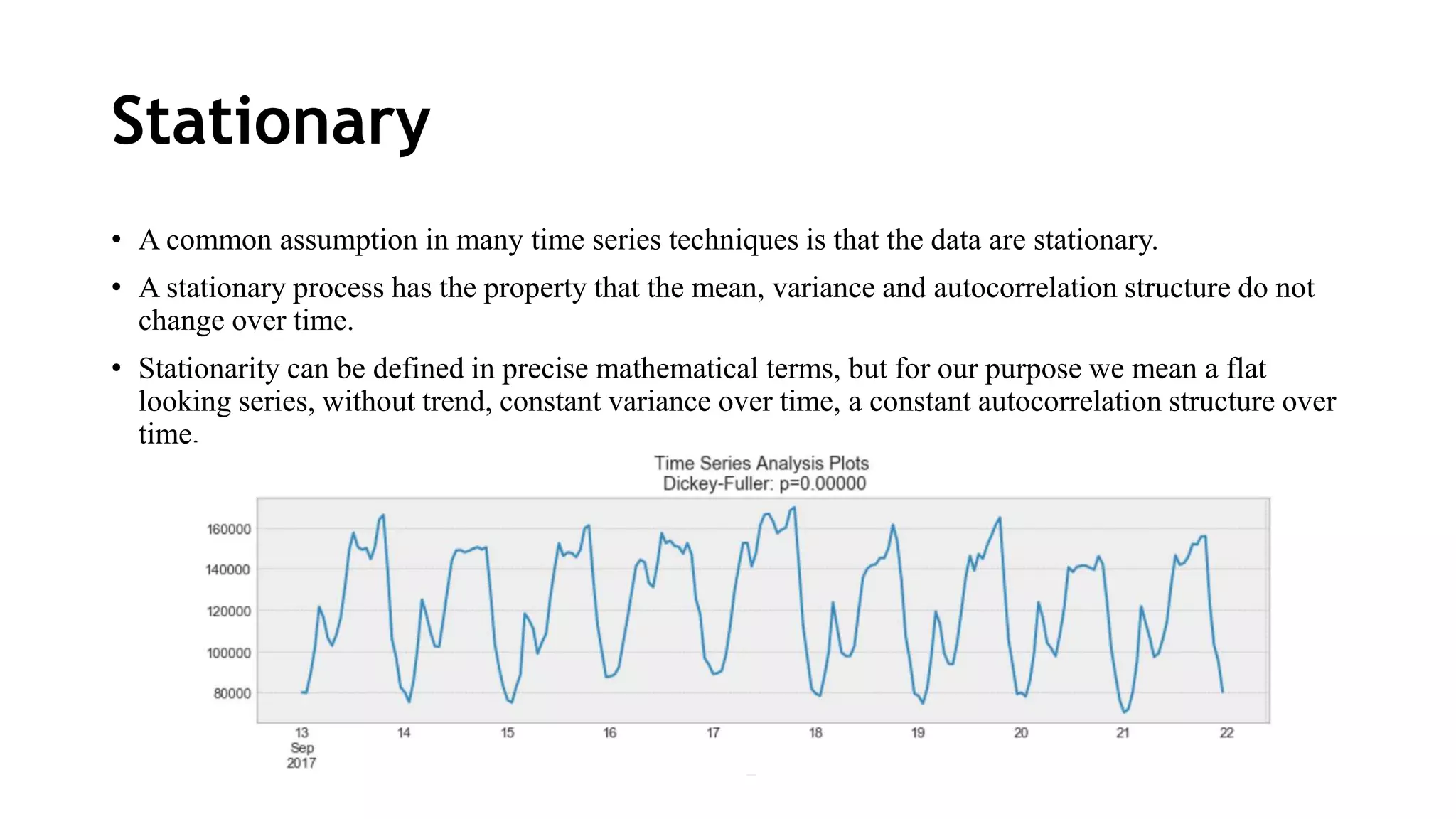

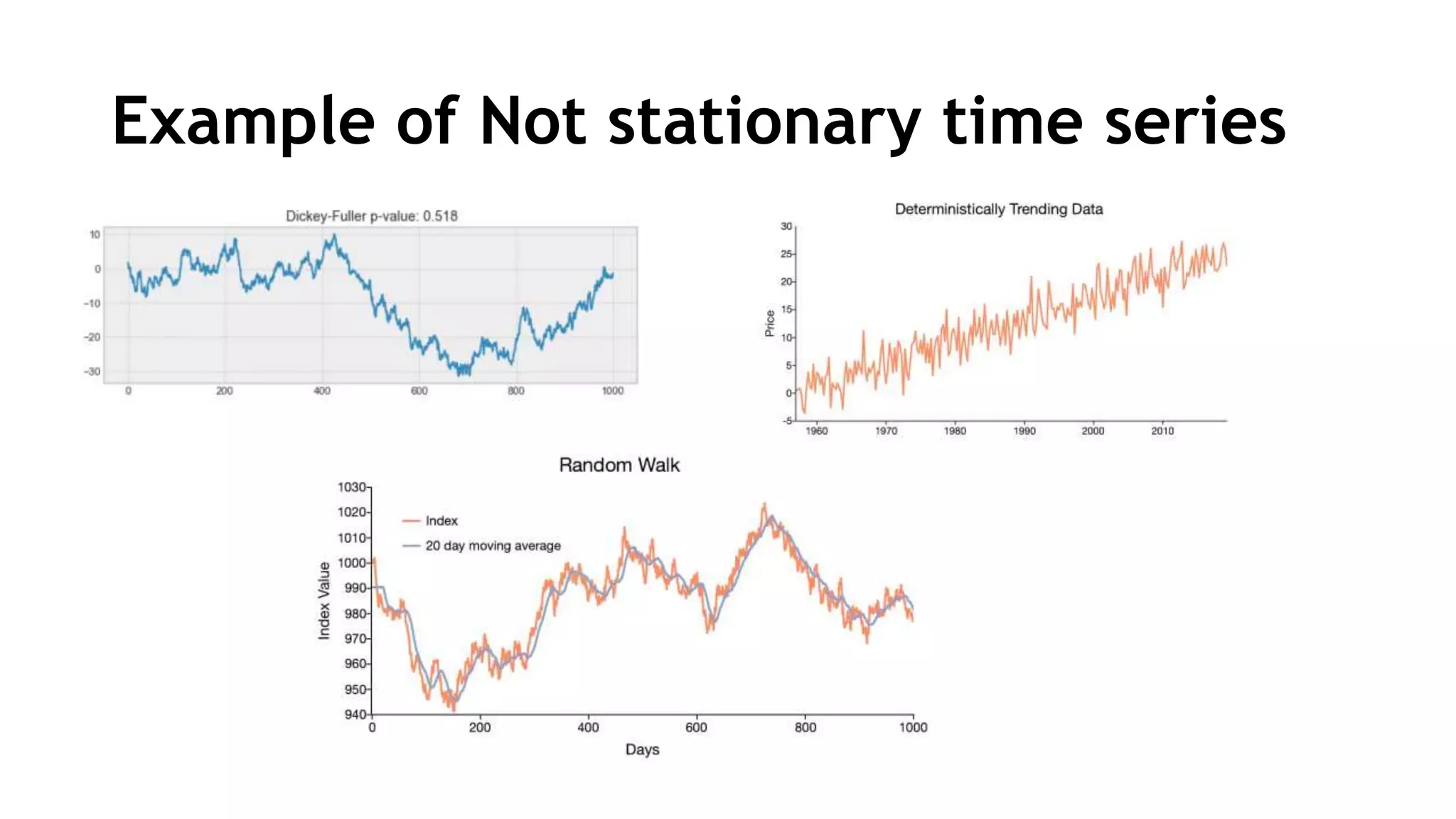

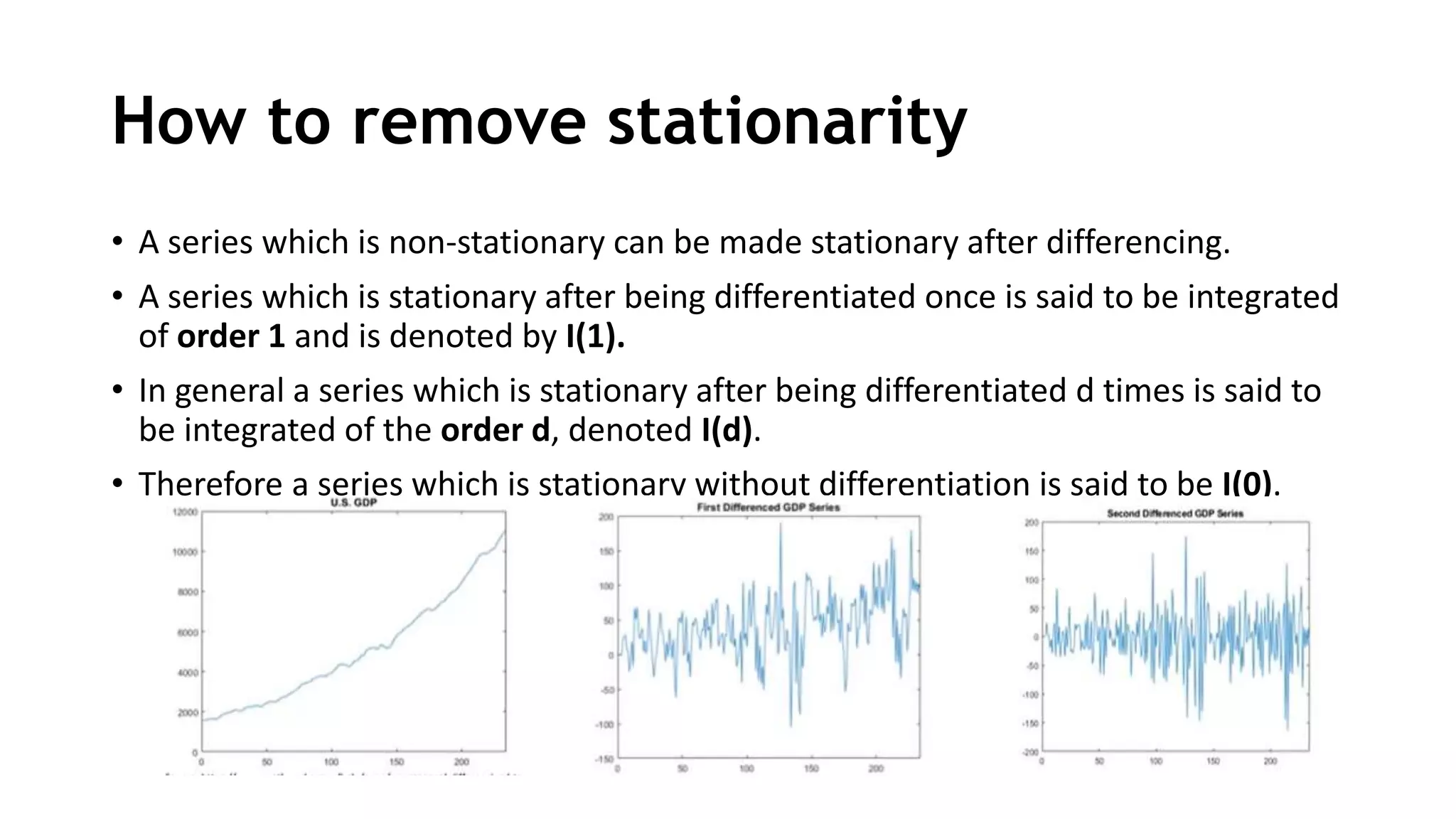

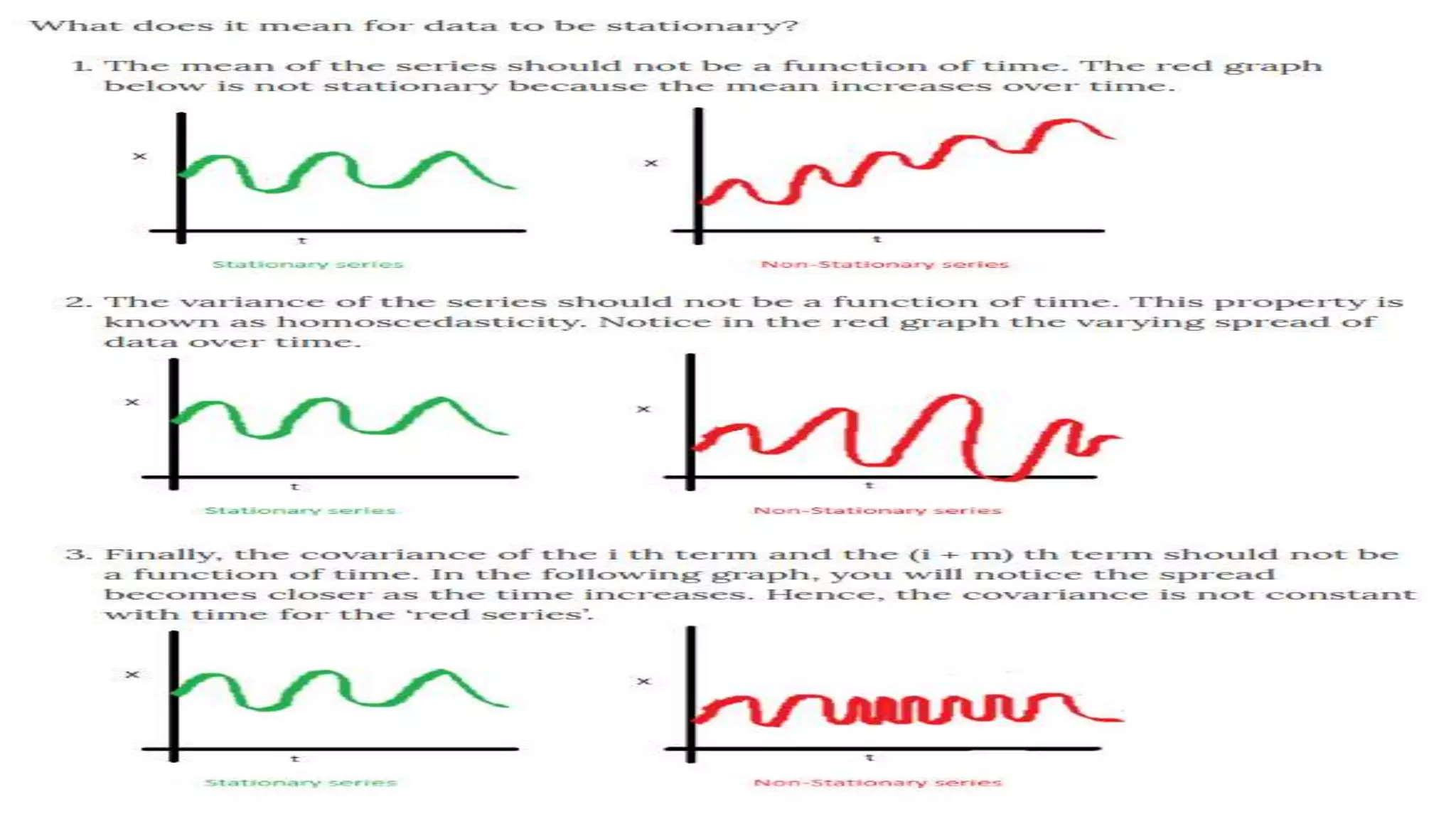

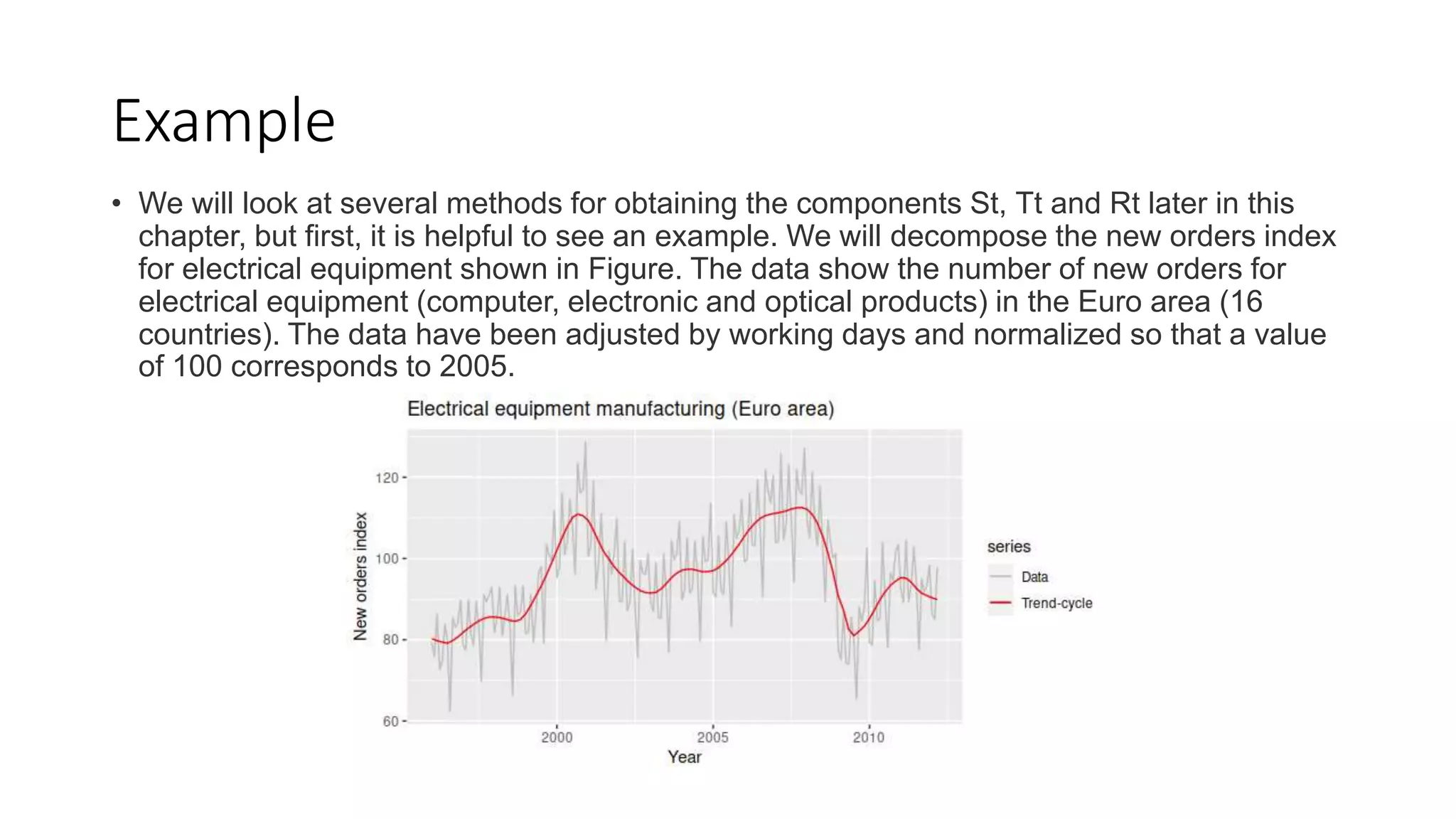

The document provides an overview of time series analysis. It discusses key concepts like components of a time series, stationarity, autocorrelation functions, and various forecasting models including AR, MA, ARMA, and ARIMA. It also covers exponential smoothing and how to decompose, validate, and test the accuracy of forecasting models. Examples are given of different time series patterns and how to make non-stationary data stationary.