Download as PDF, PPTX

![MODELVALIDATION

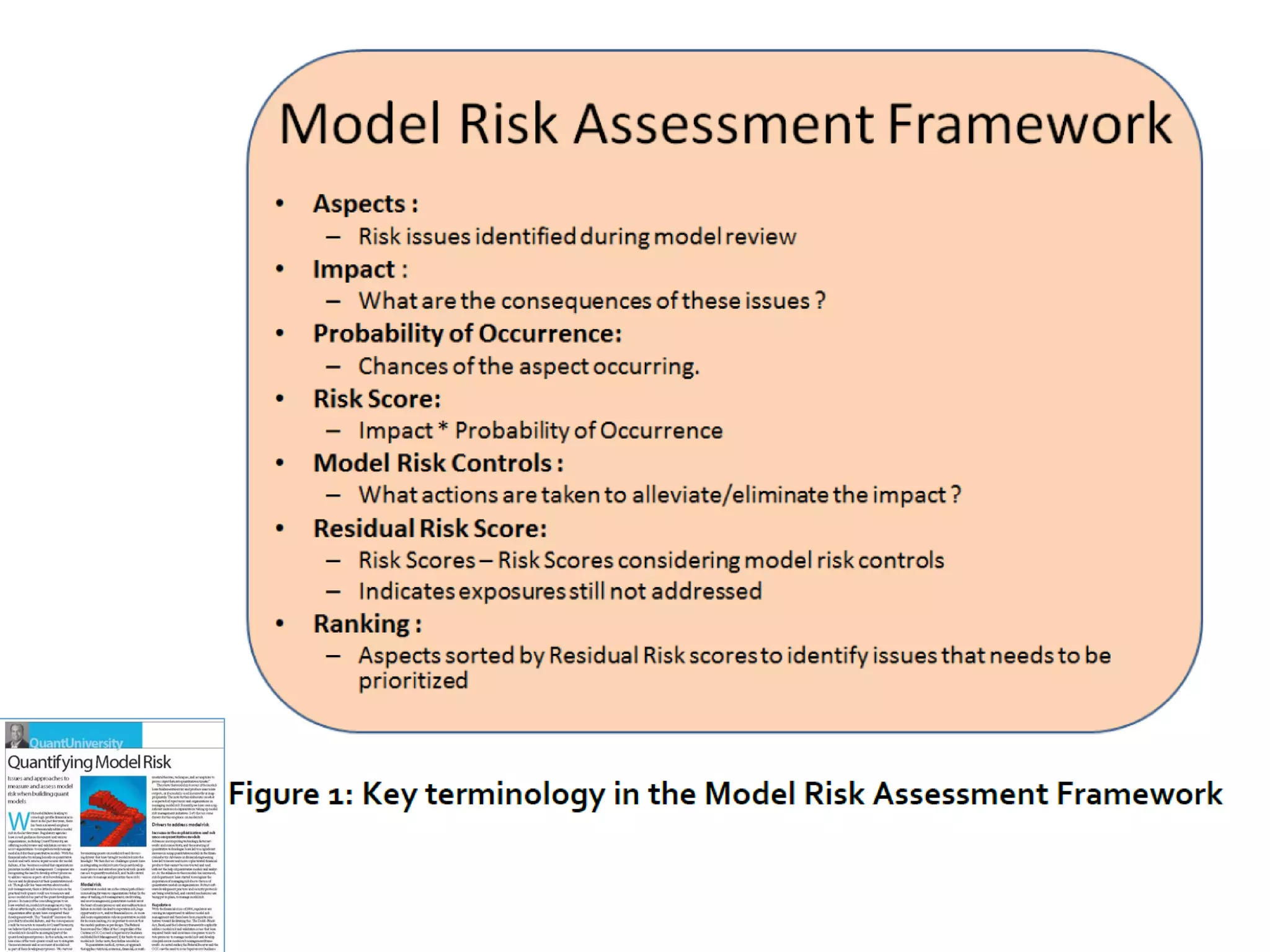

“Model risk is the potential for adverse consequences from

decisions based on incorrect or misused model outputs and

reports. “ [1]

“Model validation is the set of processes and activities

intended to verify that models are performing as expected, in

line with their design objectives and business uses. ” [1]

Ref:

[1] . Supervisory Letter SR 11-7 on guidance on Model Risk

Model Risk and Validation](https://image.slidesharecdn.com/quantuniversitypresentation-160819011349/75/Model-Risk-Management-Best-Practices-7-2048.jpg)

The document presents best practices for managing model risk in financial analytics, detailing concepts such as stress testing, scenario testing, and model validation. It outlines challenges in implementing model risk management and proposes solutions leveraging advanced technologies for analytics scalability, alongside methodologies for value-at-risk calculations. Additionally, it offers insights into model lifecycle management and invites participation in a beta program for its model risk analytics system.