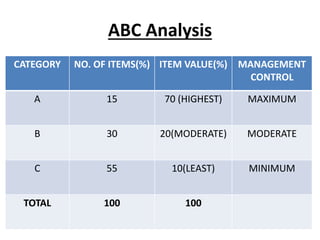

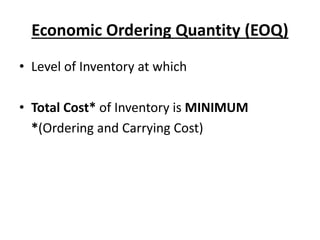

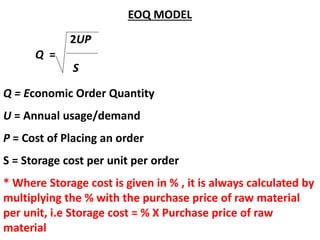

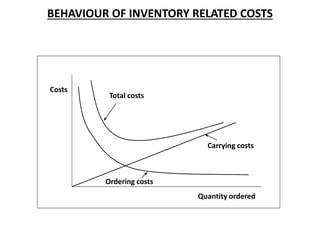

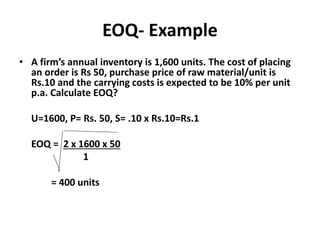

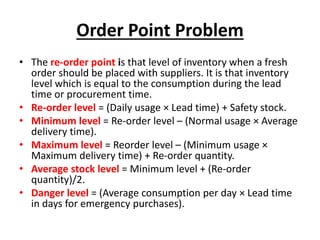

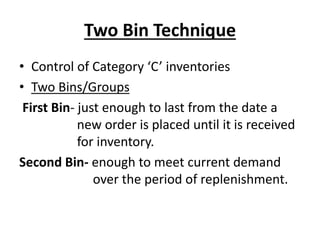

This document discusses inventory management. It defines inventory as items held for sale or used in production. The objectives of inventory management are to minimize investment in inventory while meeting product demand. Holding inventory incurs costs like ordering, carrying, and opportunity costs. There is also risk of price declines, deterioration, and obsolescence. Tools for inventory management include ABC analysis, economic order quantity (EOQ), order point problems, two bin technique, and just-in-time (JIT) systems. JIT aims to maintain minimal inventory levels and rely on suppliers for just-in-time delivery, compared to traditional just-in-case systems with higher safety stocks.