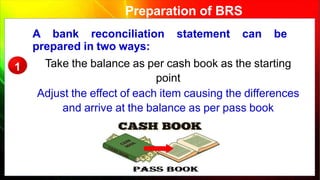

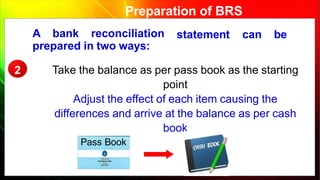

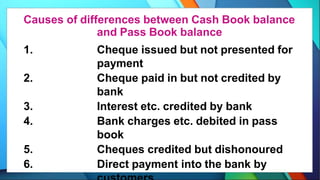

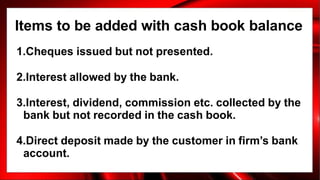

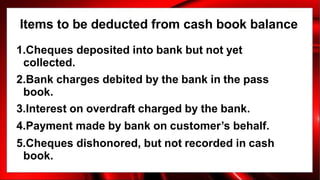

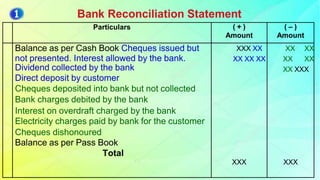

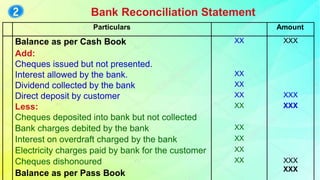

The document discusses bank reconciliation statements (BRS). A BRS is prepared by a depositor to reconcile the balance in their cash book with the balance in their bank passbook. There are typically differences between these balances due to timing of transaction recording or errors. The BRS lists adjustments for items like outstanding checks, interest/fees, that cause the differences and reconciles the two balances. It can be prepared by starting with either the cash book or pass book balance and adjusting the other balance accordingly.