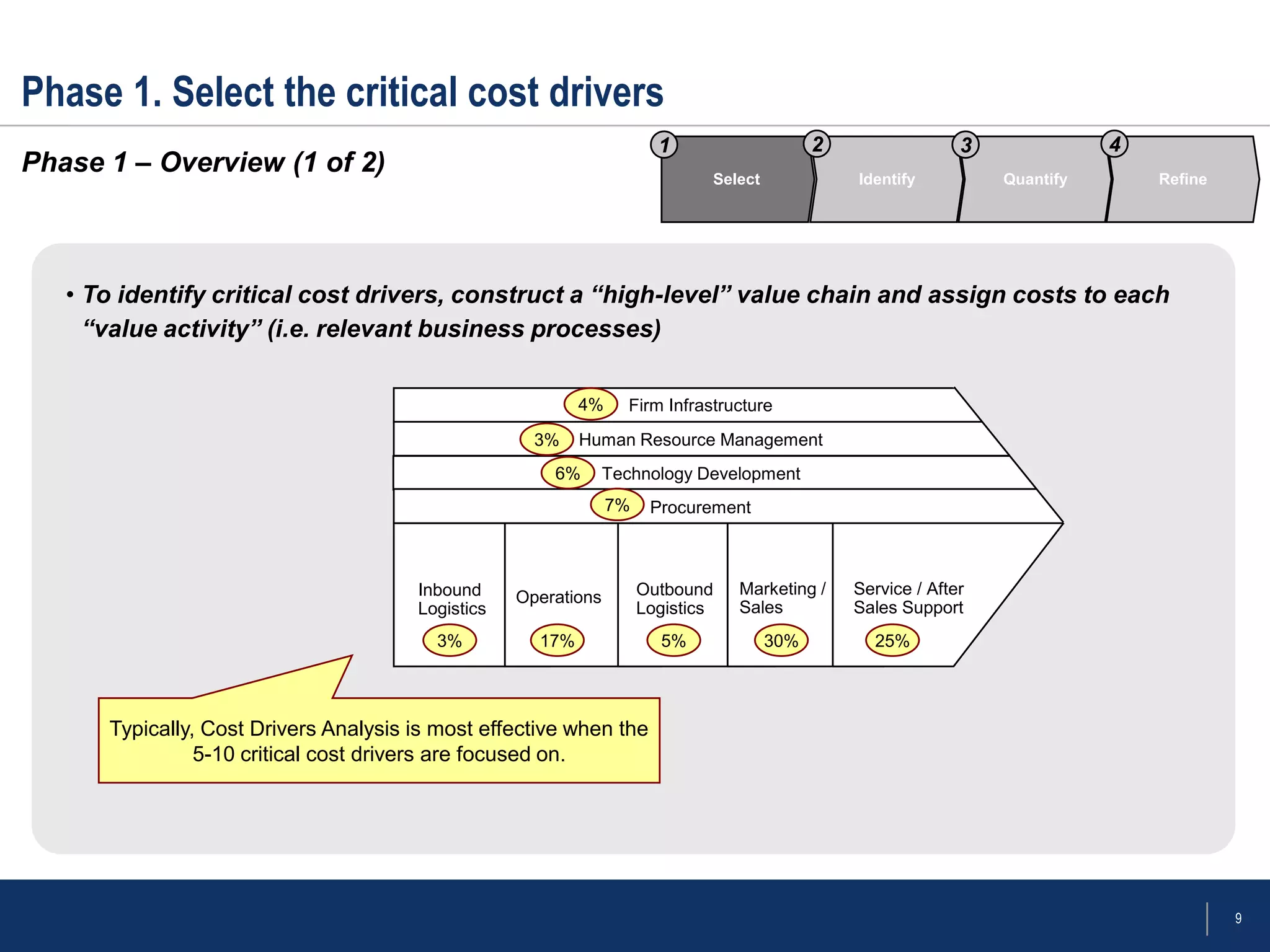

The document outlines a framework for conducting cost drivers analysis as part of competitive cost analysis, detailing techniques, phases of analysis, and benefits and limitations. It emphasizes identifying key cost drivers within a company's value chain, comparing them to competitors to uncover advantages, and quantifying these drivers for a clearer understanding of costs. The analysis involves selecting critical cost drivers, assessing structural differences among competitors, and validating hypotheses through detailed data examination.

![Strategic analysis case-framework.ppt[1]](https://cdn.slidesharecdn.com/ss_thumbnails/strategicanalysis-case-framework-ppt1-120426102932-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)