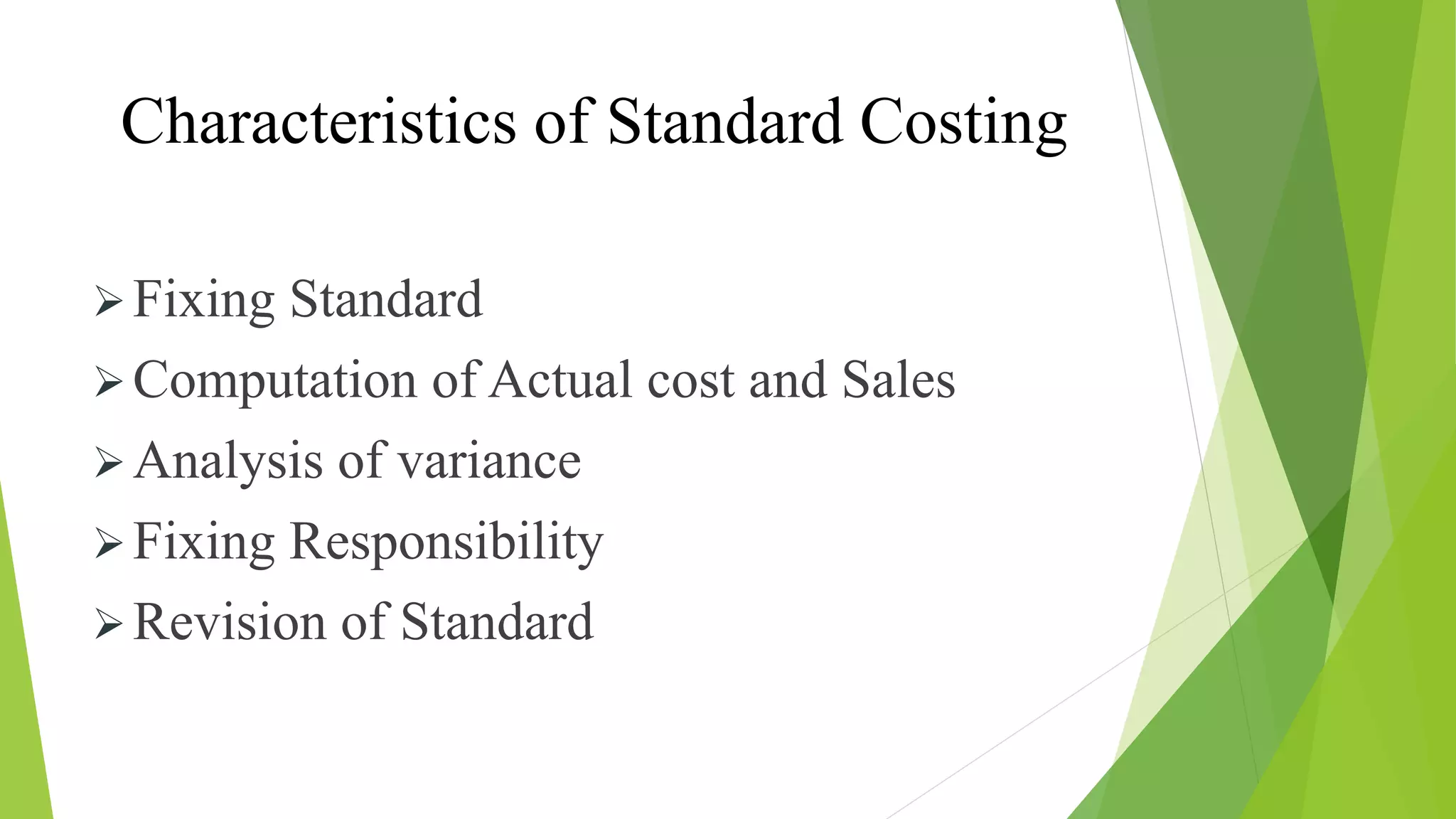

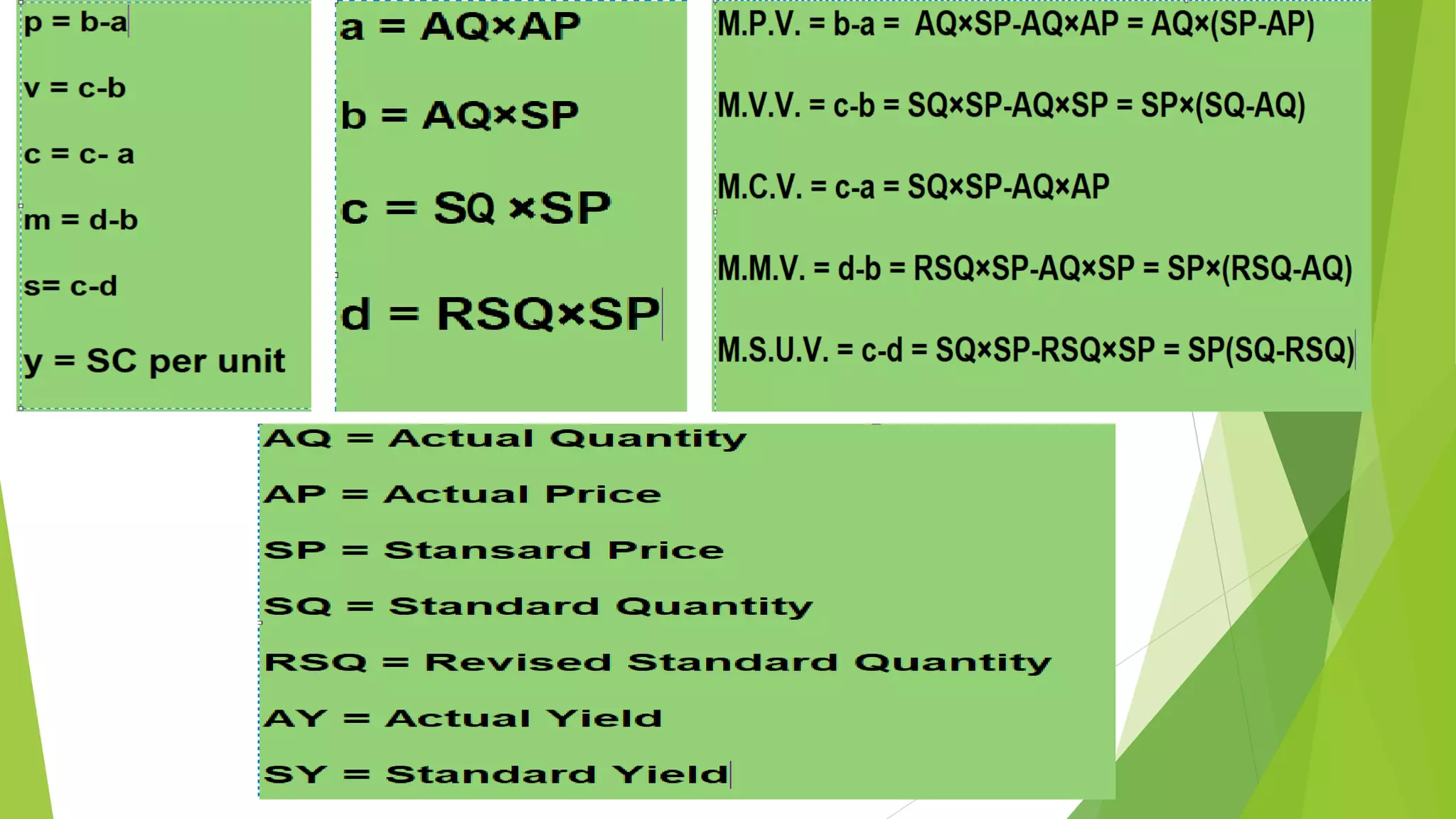

The document provides an overview of standard costing in cost accounting, including its definition, objectives, types, advantages, and limitations. Standard costing serves various purposes like performance assessment, cost control, and budgeting while distinguishing between current, basic, ideal, and attainable standards. It emphasizes the benefits, such as increased profits and productivity, while noting challenges like the need for technical skills and potential variance issues.