Downloaded 26 times

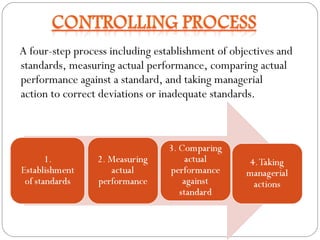

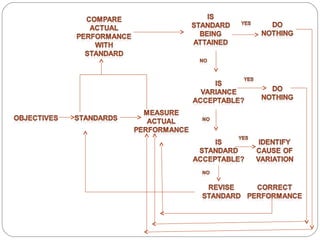

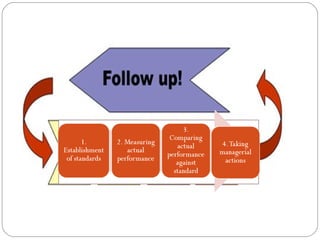

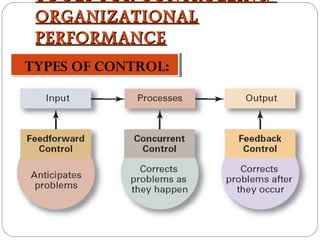

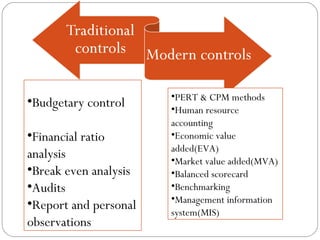

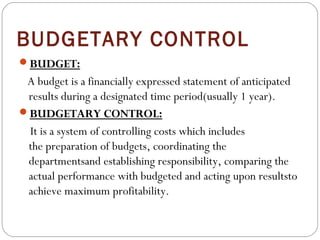

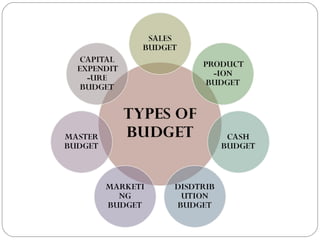

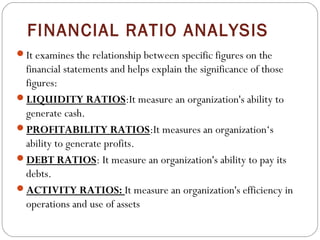

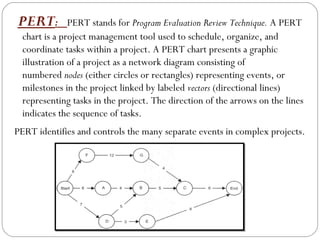

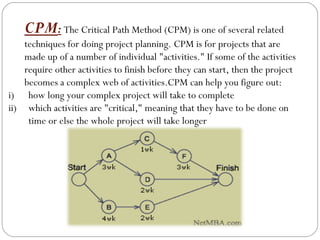

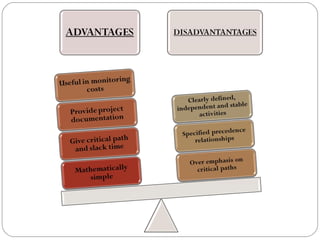

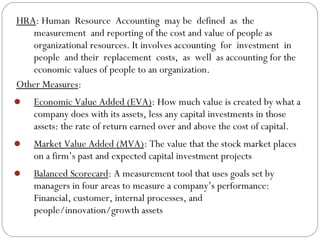

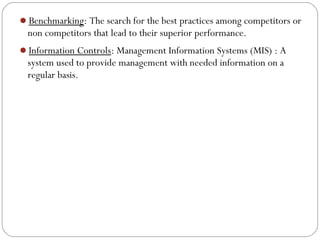

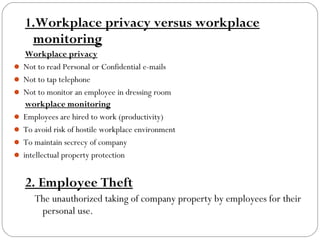

The document discusses the topic of controlling in management. It provides a 4-step controlling process: 1) establishing objectives and standards, 2) measuring actual performance, 3) comparing actual performance to standards, and 4) taking corrective actions. It also discusses different tools that can be used for organizational control, such as budgetary control, financial ratio analysis, PERT/CPM methods, and balanced scorecards. Contemporary issues in control mentioned include workplace privacy vs monitoring, employee theft, workplace violence, and corporate governance.

![Controlling techniques [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/controllingtechniquesautosaved-220710030149-eddfb7f3-thumbnail.jpg?width=640&height=640&fit=bounds)