Download as PDF, PPTX

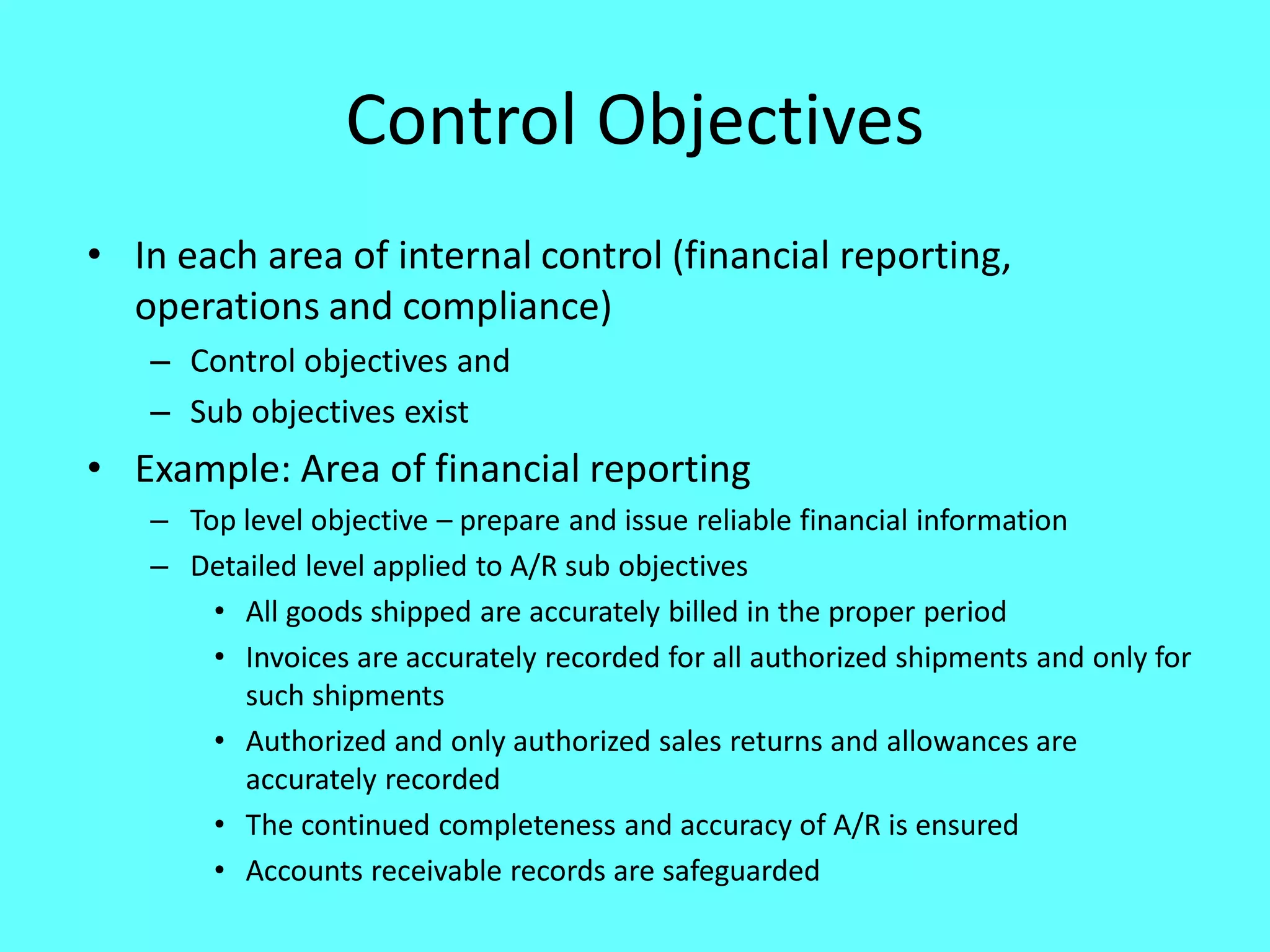

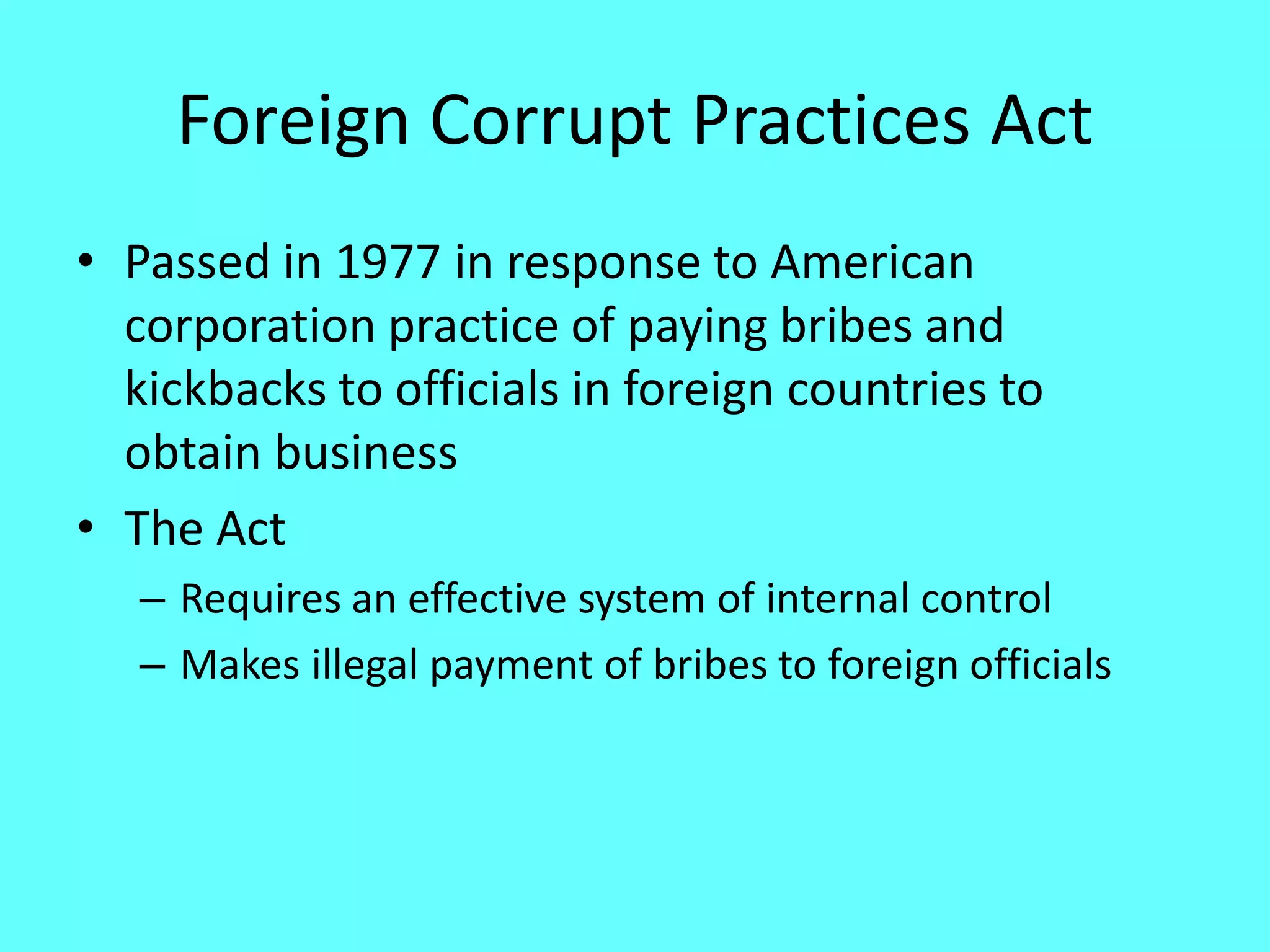

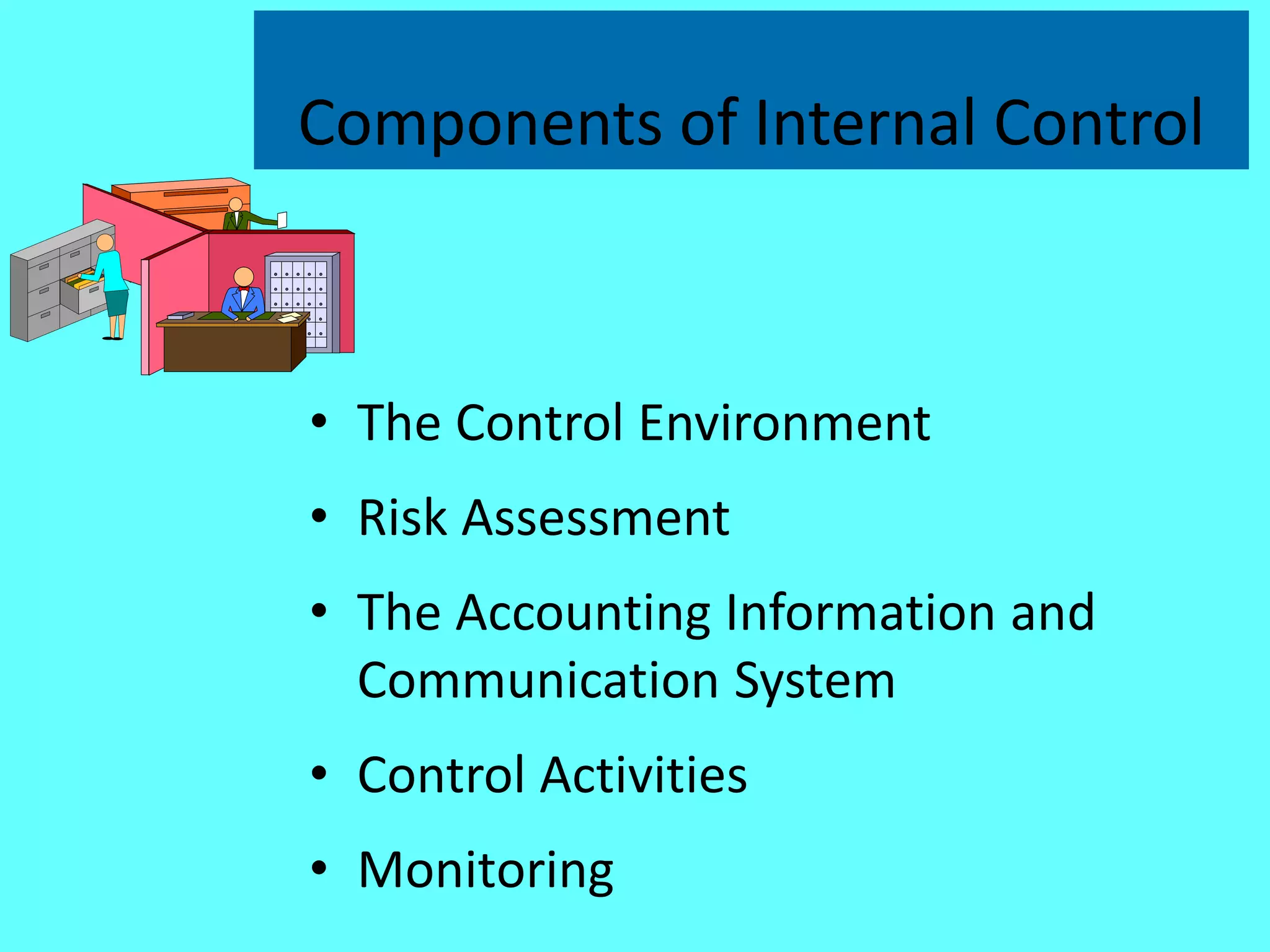

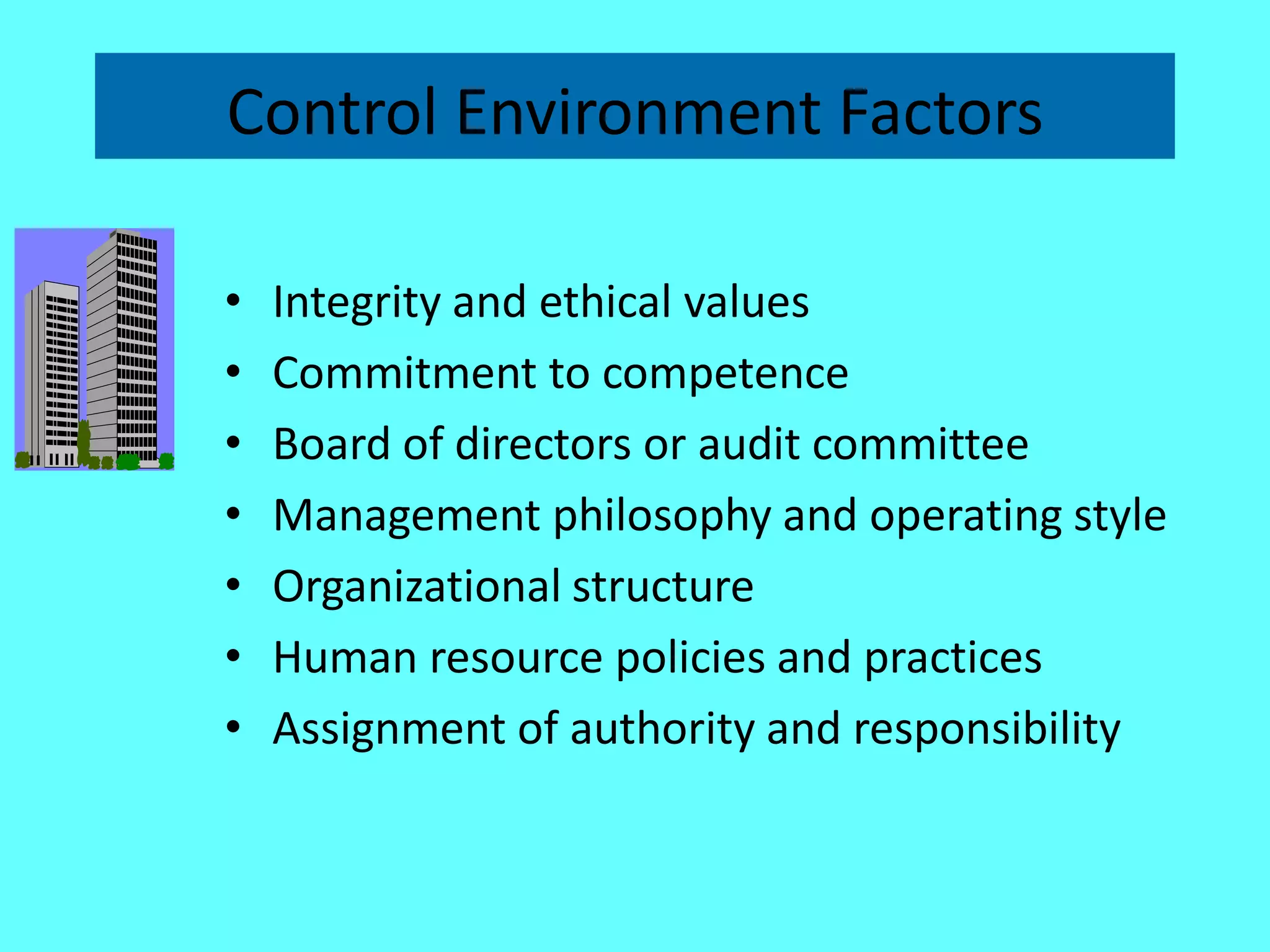

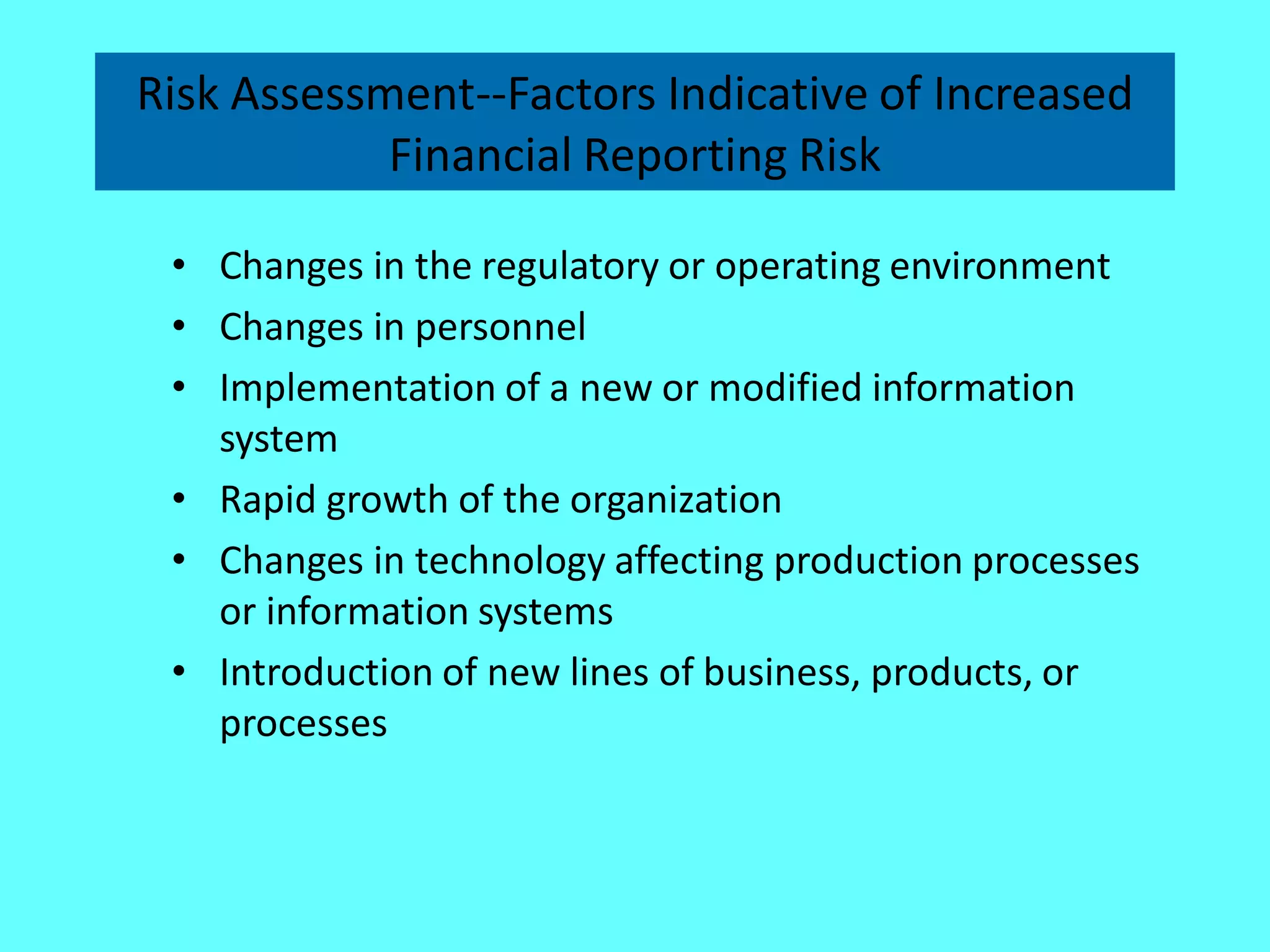

Internal control is a process designed to provide reasonable assurance regarding the achievement of objectives relating to operations, reporting, and compliance. It consists of five components: control environment, risk assessment, control activities, information and communication, and monitoring activities. The components work together to help ensure reliable financial reporting, effective and efficient operations, and compliance with laws and regulations. Internal control is important for both management and external auditors, and while it cannot provide absolute assurance, it helps reduce risks of failure to achieve goals.