Downloaded 80 times

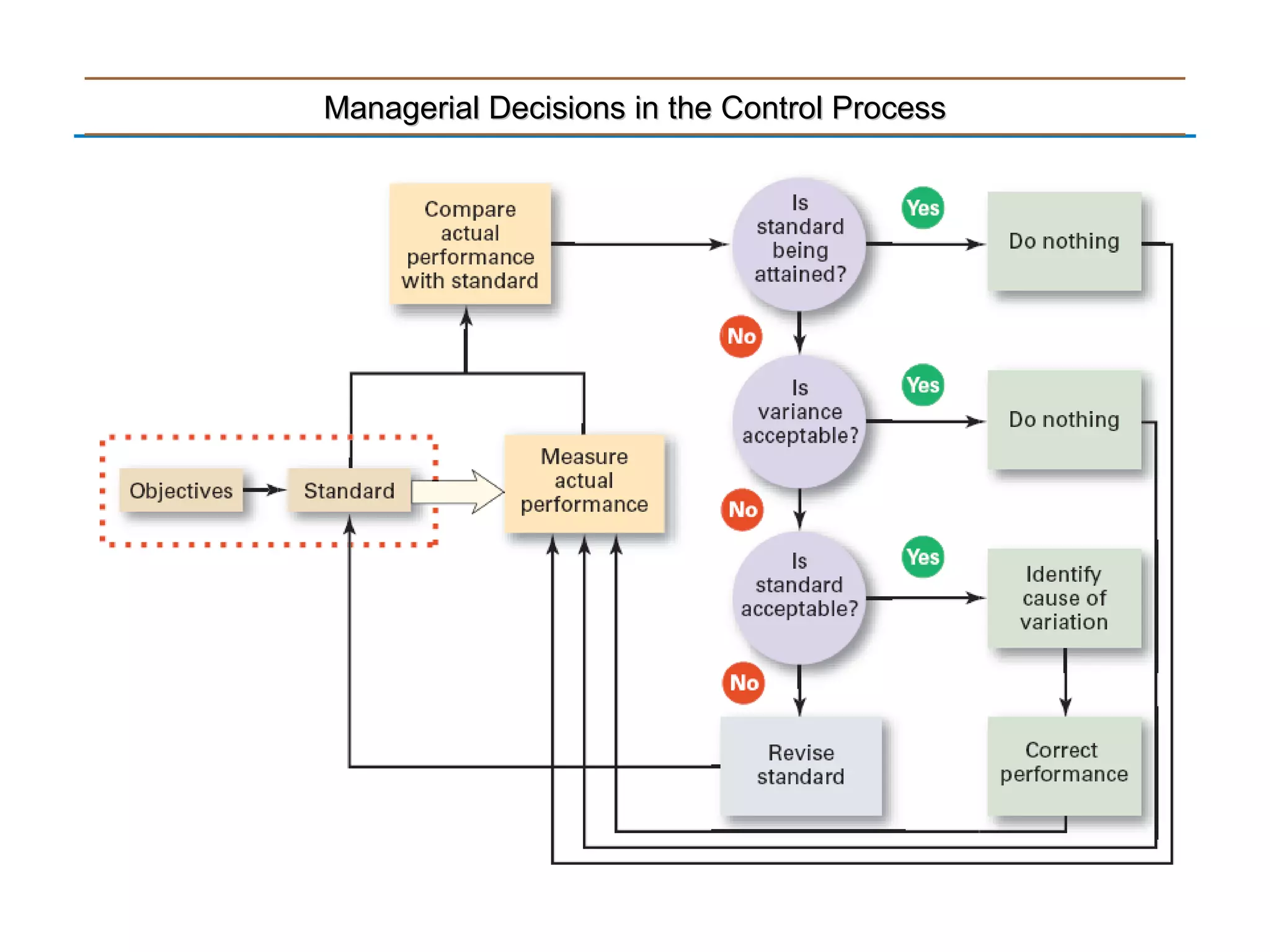

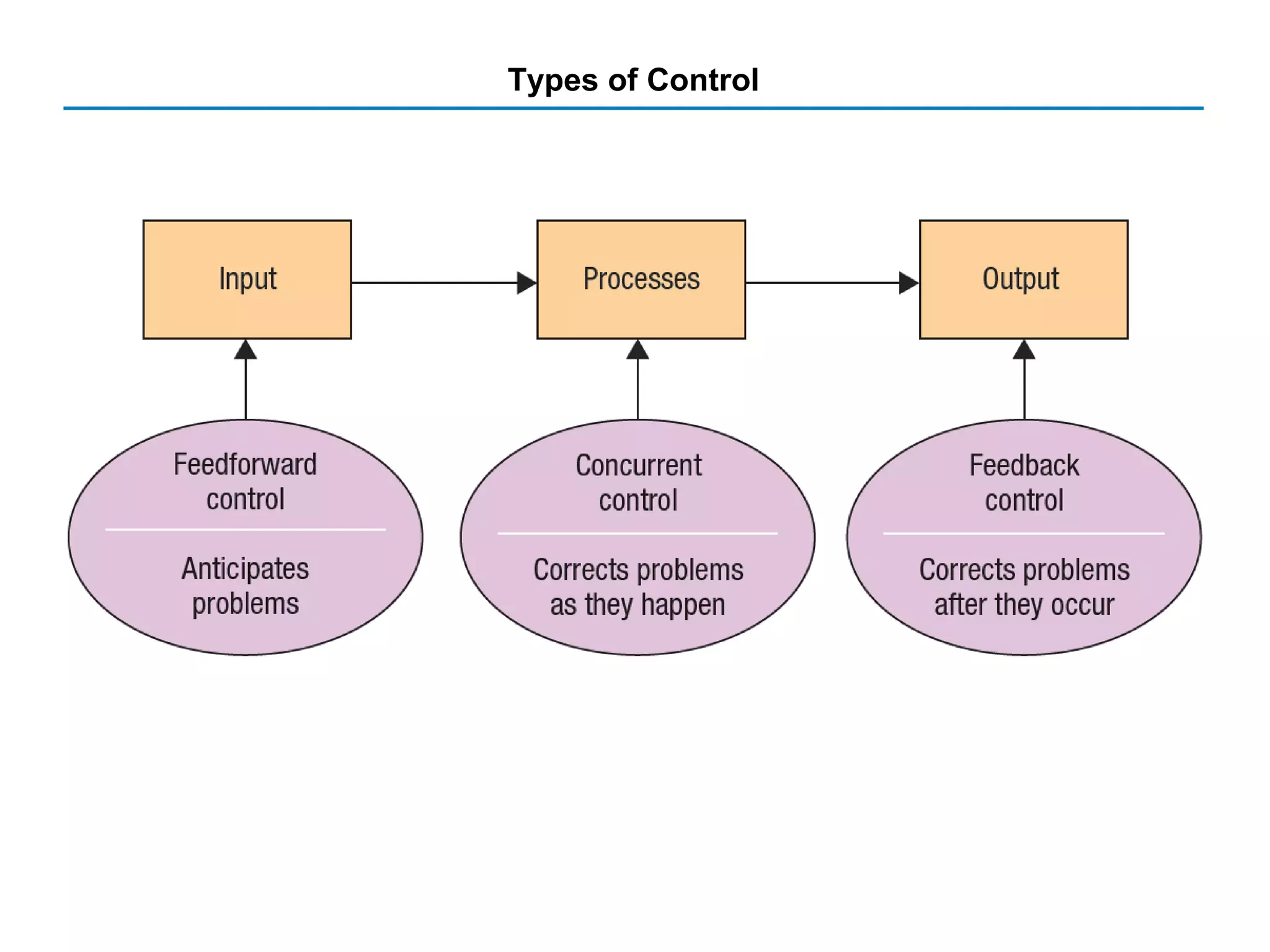

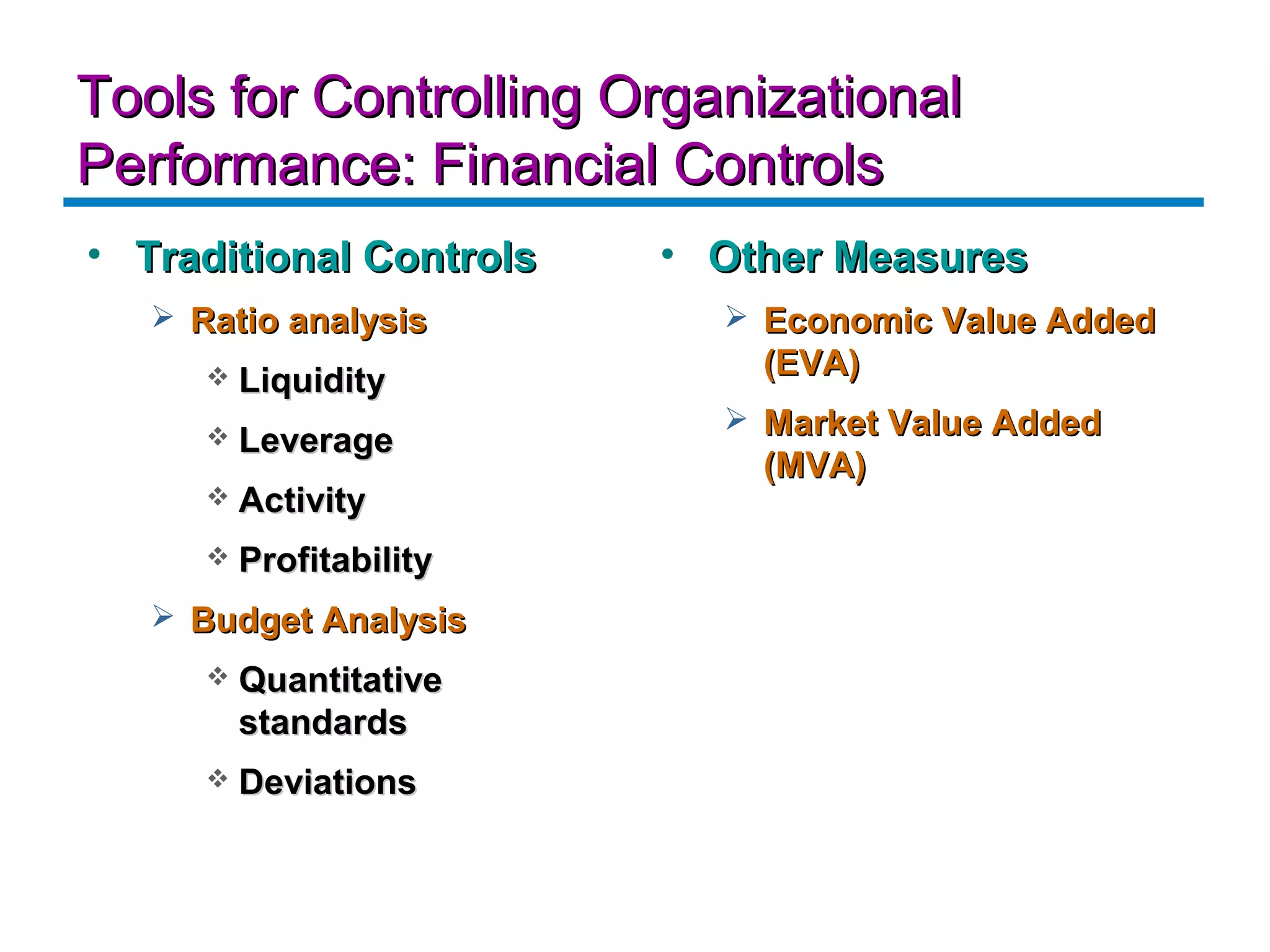

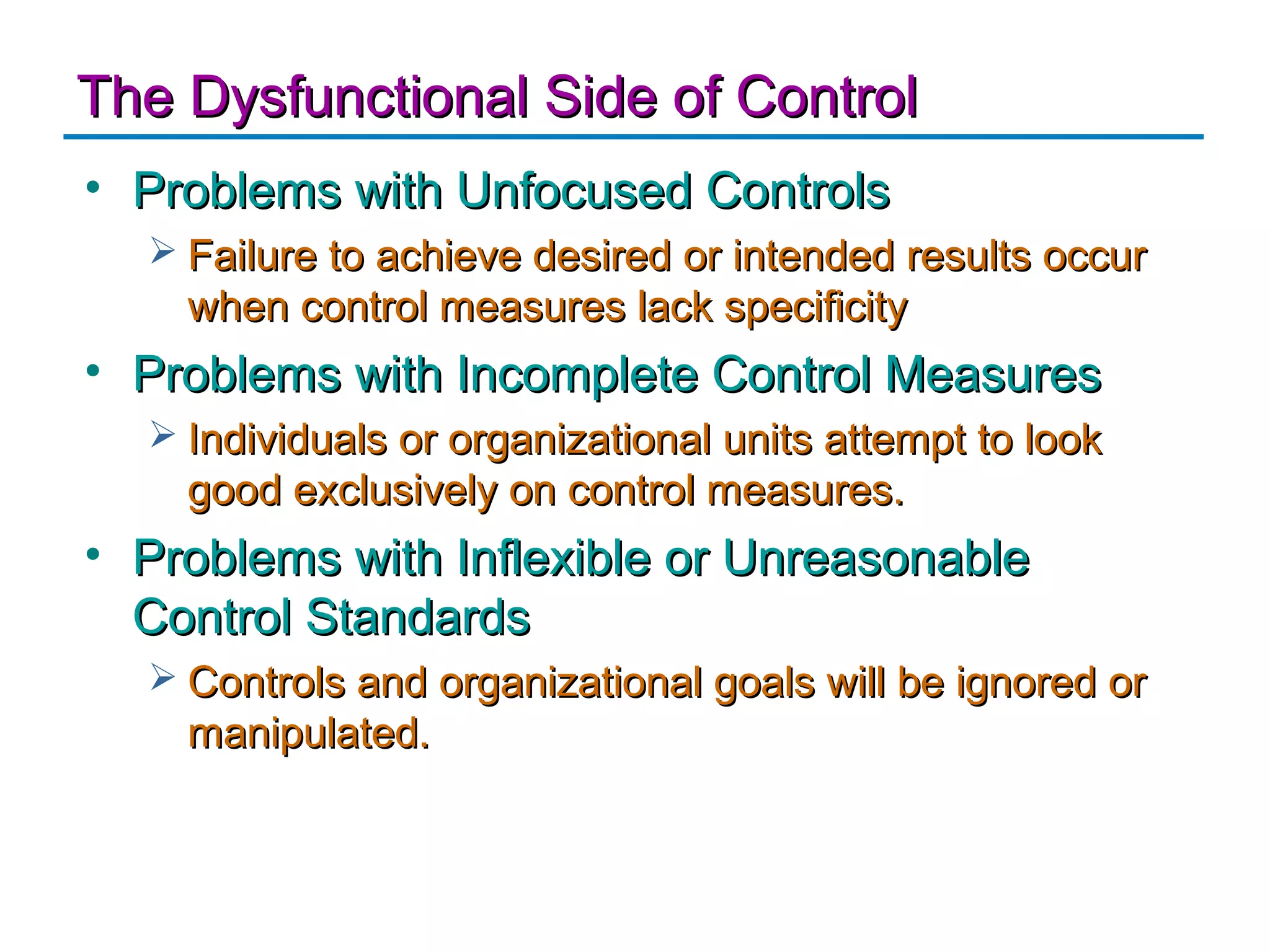

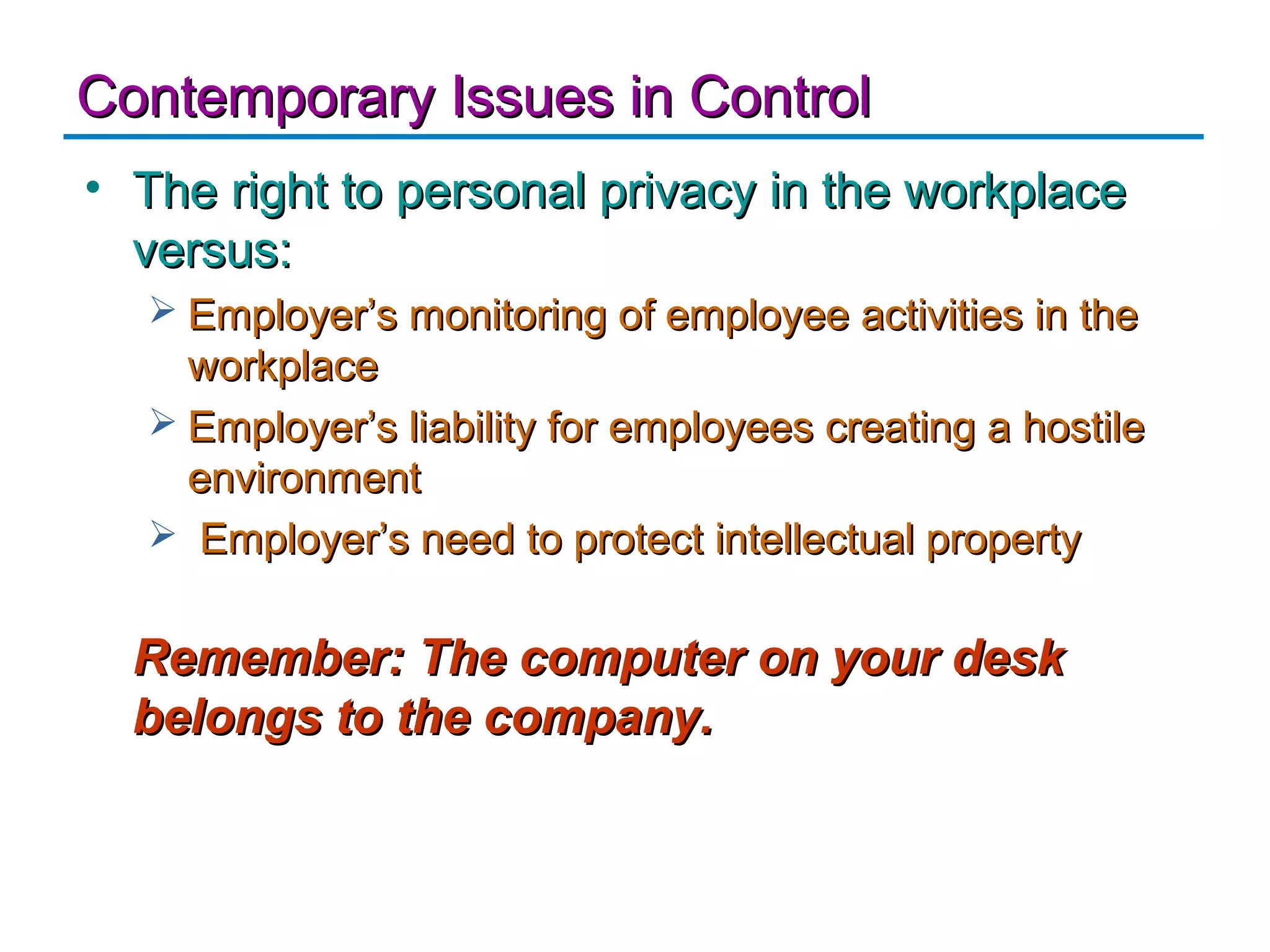

Control involves monitoring activities to ensure goals are met and correcting deviations. It is important as the final stage of management functions, providing feedback on performance and protecting the workplace. The control process involves measuring actual performance against standards, identifying variances, and taking action. Organizational performance measures include productivity, effectiveness, financial ratios, and balanced scorecards. Information and cultural controls vary across countries. Issues around privacy, monitoring, and intellectual property require balance.