Download to read offline

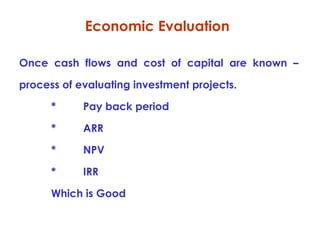

This document discusses international capital budgeting and the foreign investment decision process. It outlines several key steps in the process, including assessing the political climate of the host country, performing a cash flow analysis from the perspective of both the subsidiary and parent company, determining the required rate of return or cost of capital, evaluating projects using techniques like NPV and IRR, selecting projects, analyzing risk, implementing projects, and conducting post audits. International capital budgeting involves additional complexities over domestic capital budgeting, such as accounting for political risk, exchange rate changes, and cash flows to both the subsidiary and parent company.