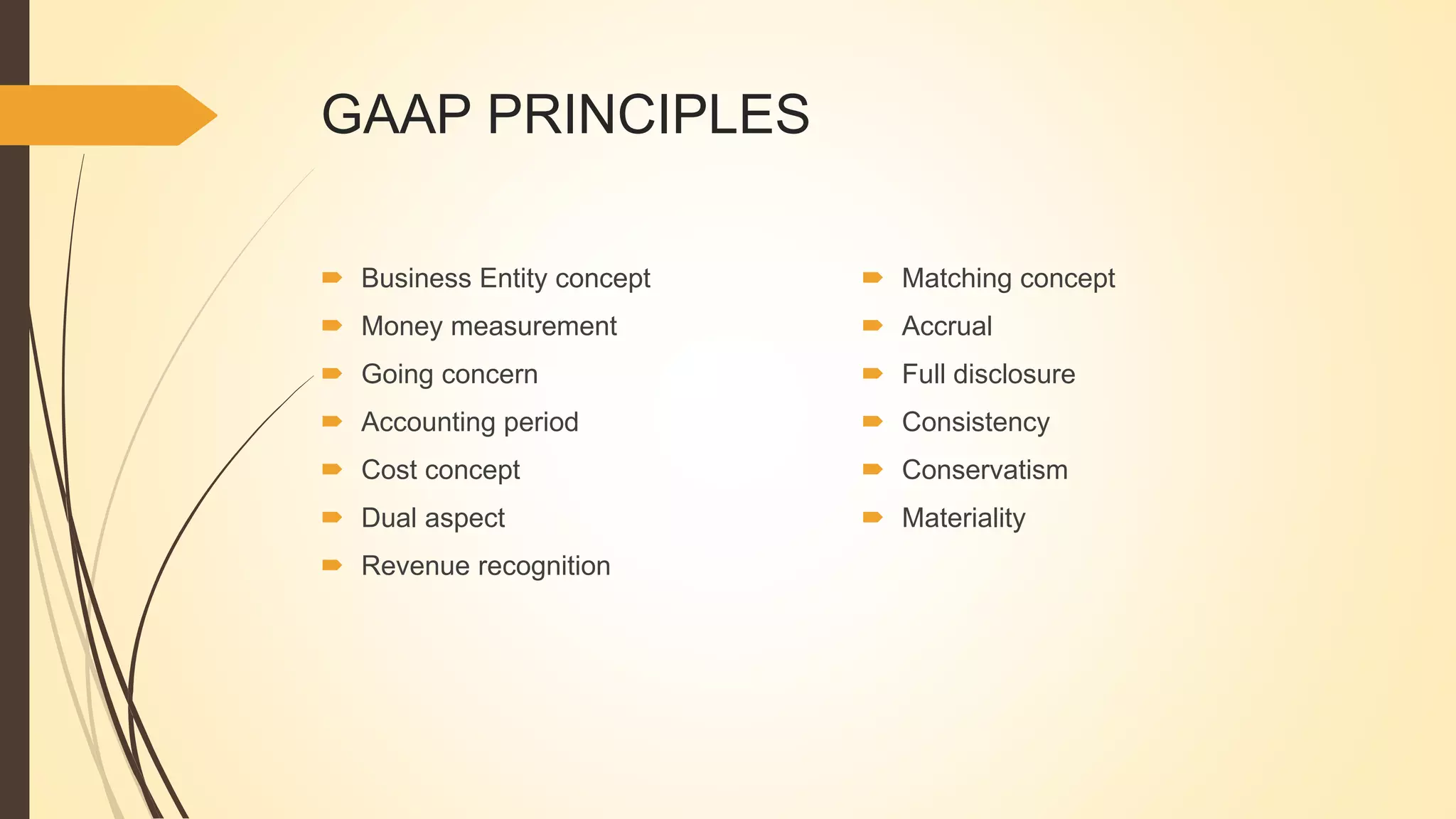

This document provides an overview of basic accounting principles for an 11th grade class. It defines accounting as recording, summarizing, reporting and analyzing financial transactions. Generally Accepted Accounting Principles (GAAP) establish uniform rules for recording transactions to bring consistency to financial statements. Key principles discussed include the business entity, money measurement, going concern, accounting period concepts as well as revenue recognition, matching, accrual, full disclosure, consistency and conservatism. The objectives are for students to understand and apply these principles when recording business transactions.