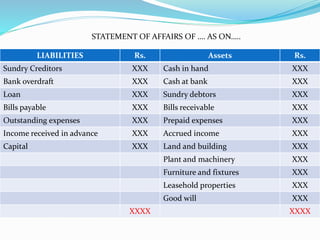

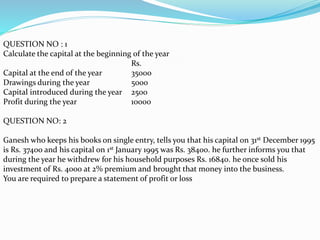

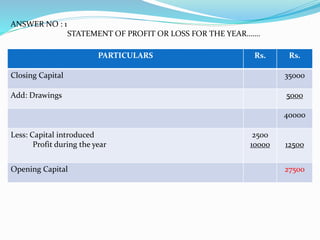

This document provides information about single entry bookkeeping systems. It defines single entry as an informal system without defined rules that is used by small sole proprietor businesses. Transactions are not systematically recorded. The document discusses two methods for single entry - the net worth method which uses statements of affairs to calculate profit or loss, and the conversion method which converts single entry records into a double entry format. It provides examples of accounting questions involving single entry systems, showing how to prepare statements of profit and loss and statements of financial position from incomplete single entry records.