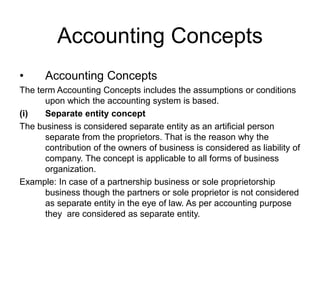

This document discusses key accounting concepts and conventions used in preparing financial statements according to Generally Accepted Accounting Principles (GAAP). It outlines concepts such as the separate entity concept, going concern concept, money measurement concept, and dual aspect concept. It also covers conventions like conservatism, full disclosure, consistency, and materiality that accountants should follow when preparing financial statements to provide an accurate representation of a company's financial position.

![Acounting Concepts and Conventions [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/acountingconceptsandconventionsautosaved-250421132407-1a5db1b2-thumbnail.jpg?width=640&height=640&fit=bounds)