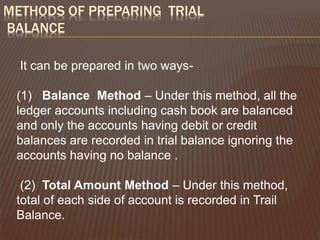

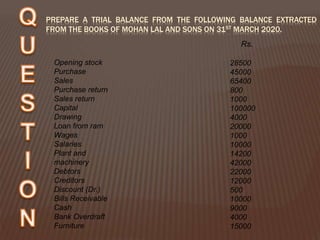

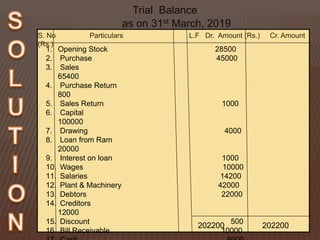

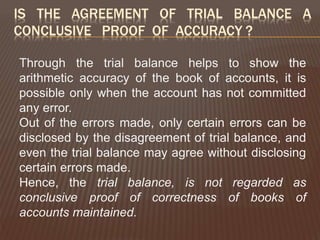

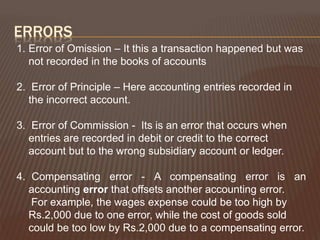

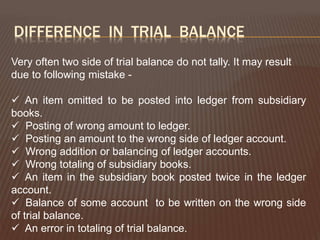

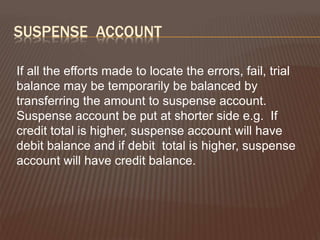

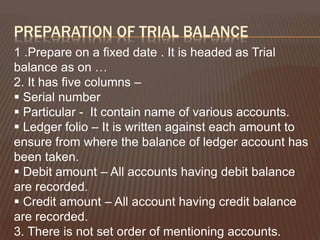

A trial balance is a financial statement that lists the debit and credit balances of all accounts in the general ledger. It is prepared to check the arithmetic accuracy of the ledger accounts and help detect errors. The trial balance is not a conclusive proof of accuracy as certain errors may remain undetected even if the debit and credit totals match. Common errors include omissions, incorrect postings, or wrong account balances. If errors cannot be found, a suspense account is used to temporarily balance the trial balance.

![RULES FOR PREPARATION OF

TRIAL BALANCE

While preparation of trial balances we must take care of

the following rules/points

1] The balances of the following accounts are always

found on the debit column of the trial balance

-Assets

-Expense Accounts

-Drawings Account

-Cash Balance

-Bank Balance

-Any losses

Contd](https://image.slidesharecdn.com/trialbalanceppt-210831140445/85/Trial-balance-ppt-8-320.jpg)

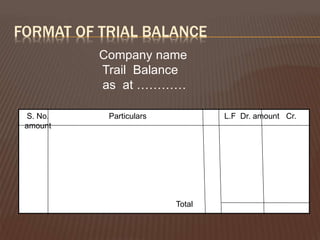

![2] And the following balances are placed on the credit

column of the trial balance

-Liabilities

-Income Accounts

-Capital Account

-Profits

3] Closing stock is usually not shown in Trail Balance. It

is shown below the trial balance as an additional

information.

It represent the unsold stock out of total opening stock

and purchase. However it can appear in trial balance by

making adjustment in purchase by passing following

entry. Closing stock A/C Dr.

To Purchase A/C](https://image.slidesharecdn.com/trialbalanceppt-210831140445/85/Trial-balance-ppt-9-320.jpg)