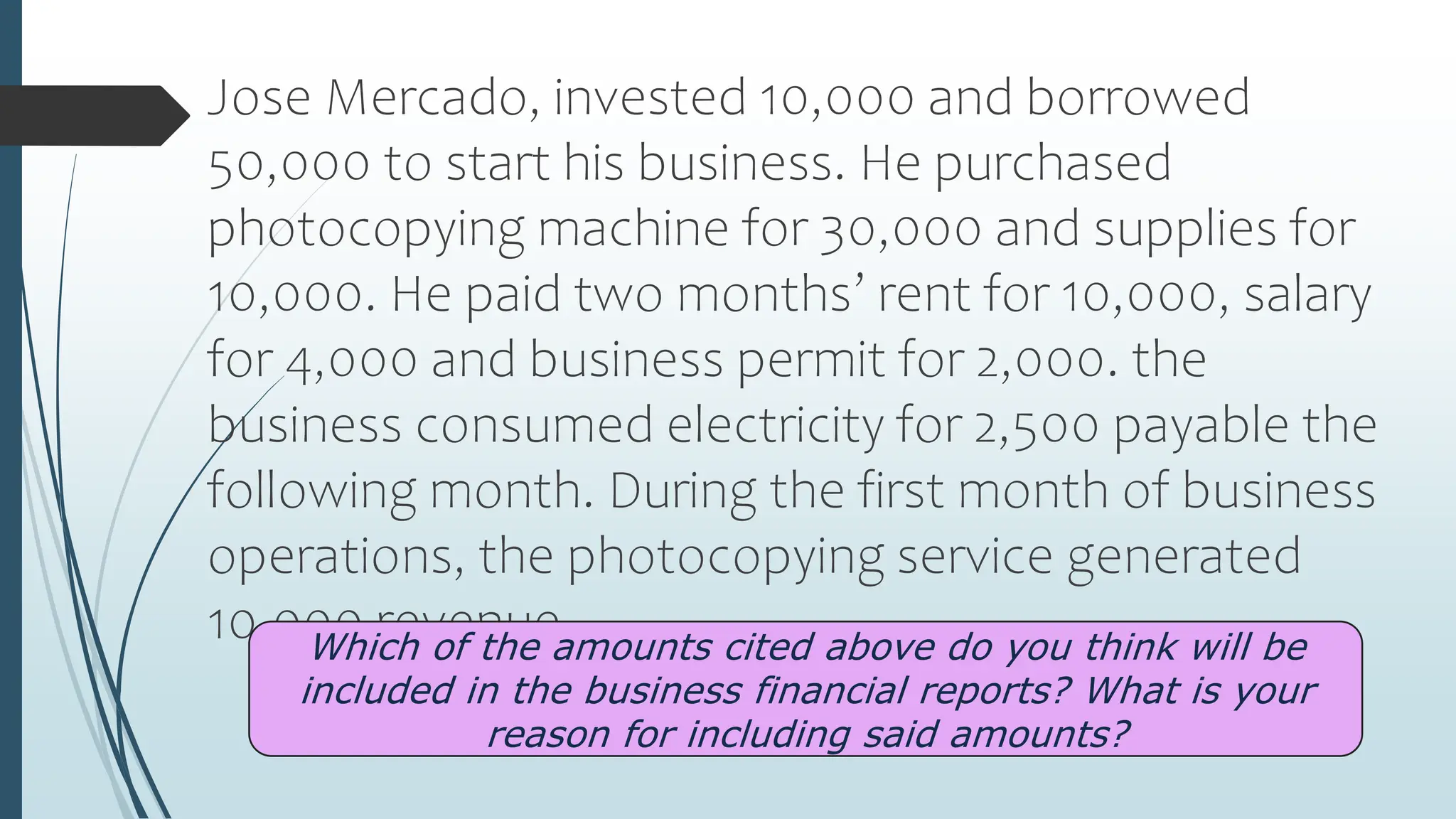

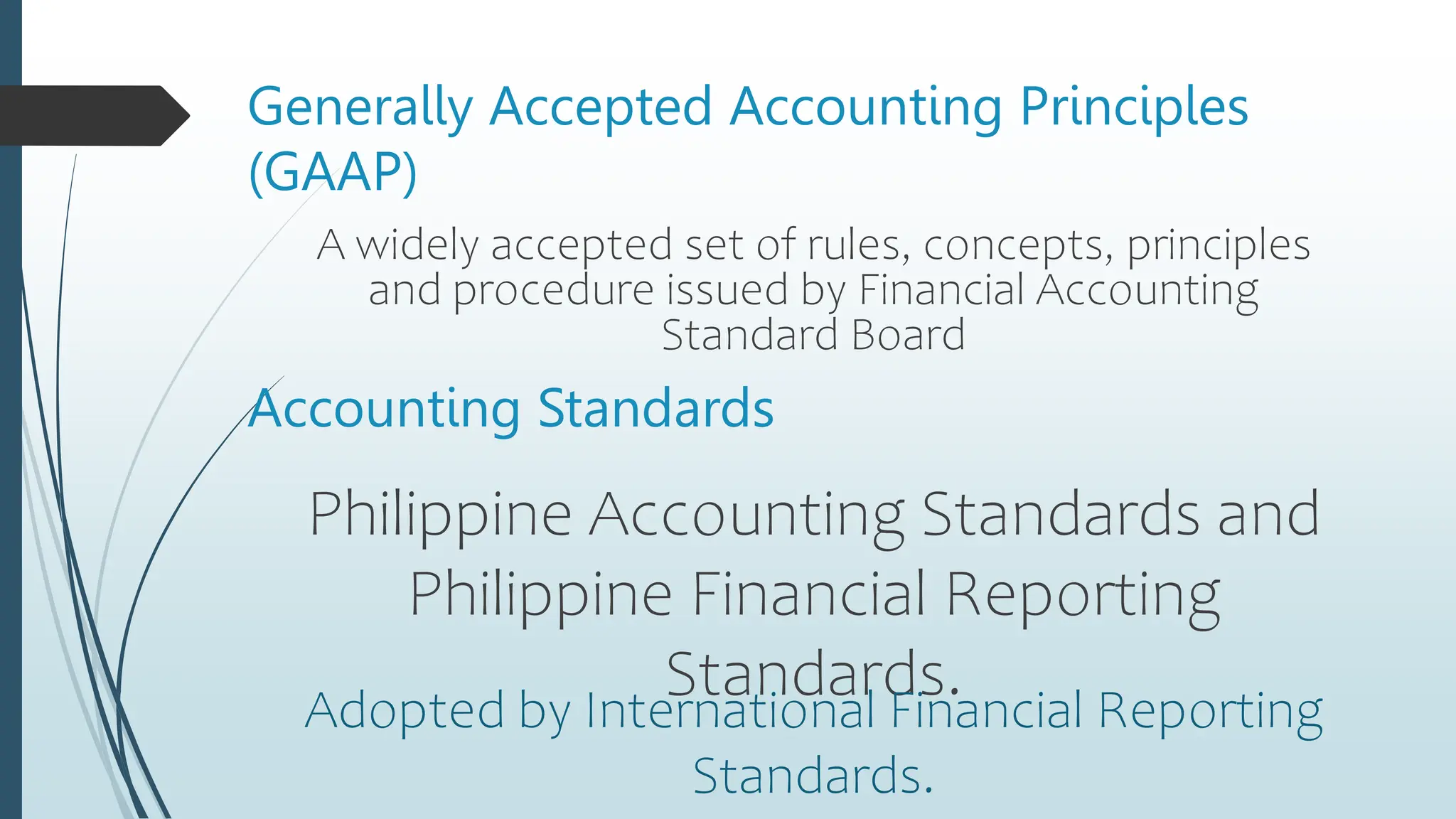

Jose Mercado started a photocopying business by investing 10,000 and borrowing 50,000. He used the funds to purchase a photocopying machine for 30,000, supplies for 10,000, pay two months rent of 10,000, salaries of 4,000 and a business permit of 2,000. Electricity costs of 2,500 were also incurred. In the first month of operations, the business generated 10,000 in revenue. The amounts that would be included in the business' financial reports are the investment of 10,000, borrowing of 50,000, expenses incurred such as rent, salaries, supplies and electricity, as well as the revenue generated according to accounting principles of accrual accounting and revenue