Downloaded 17 times

![Cont.

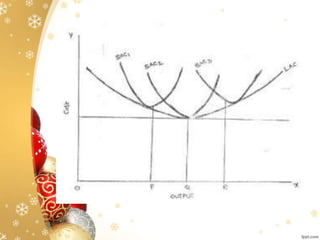

Economies of scale

Internal Economies

I. Managerial Economies

II. Financial Economies

III. Technical Economies

IV. Trade Economies

External Economies

I. Economies of Concentration [localized economies]

II. Economies of Dis-integration

III. Economies of Information](https://image.slidesharecdn.com/unit4meproductionfunction-161009192446/85/Unit-4-me-production-function-15-320.jpg)

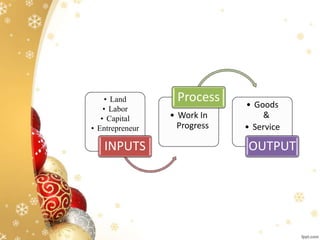

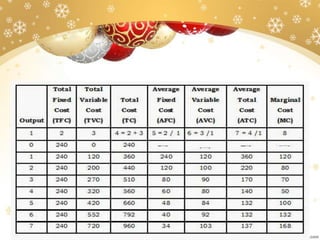

The document discusses production functions and costs. It defines a production function as the relationship between inputs like labor, capital, land, and entrepreneurship and the volume of output. It describes how productivity curves show different combinations of inputs that can produce certain outputs. It also discusses concepts like economies of scale, fixed vs variable costs, and how average and marginal costs change with different levels of output in the short run and long run.