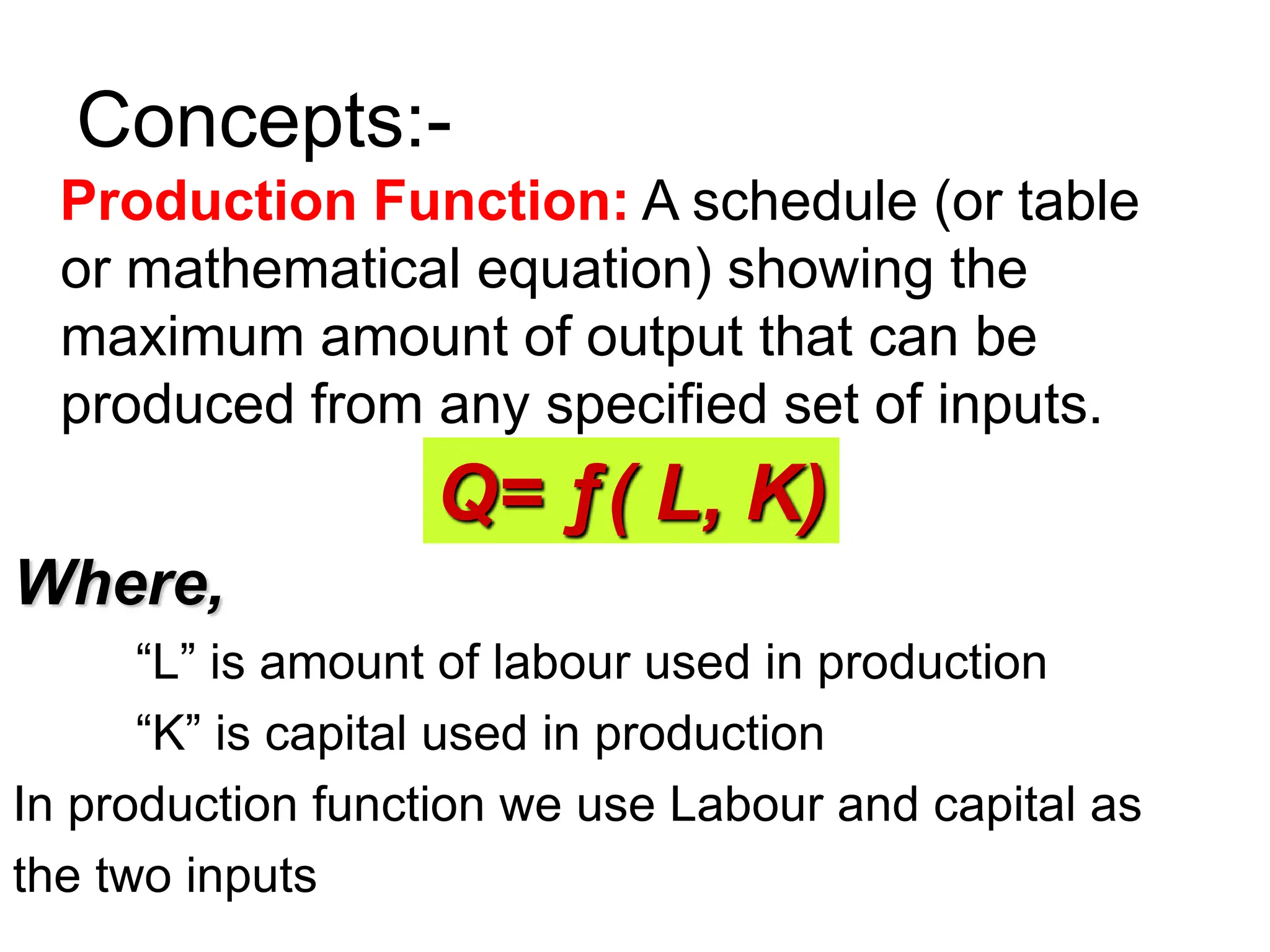

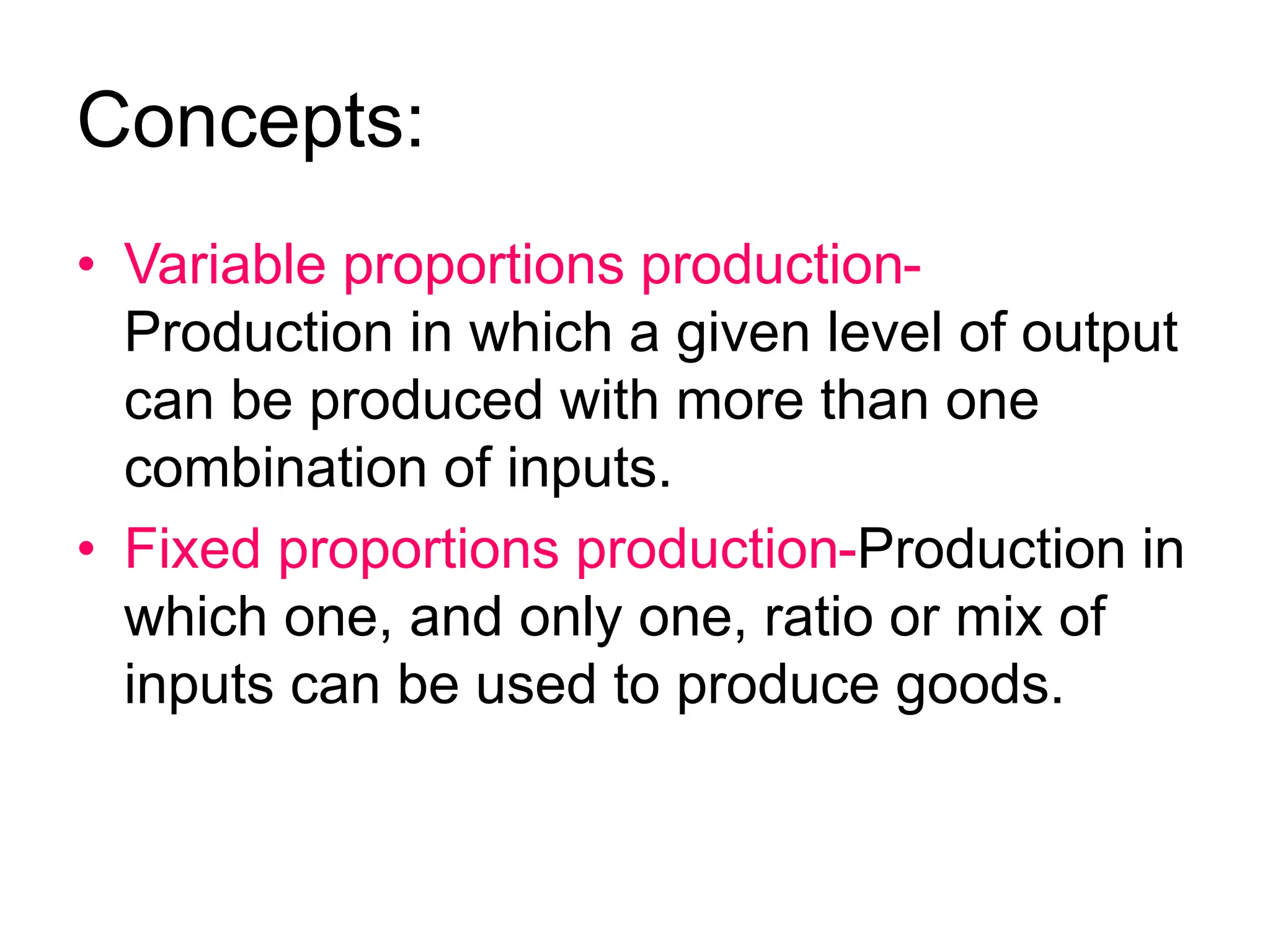

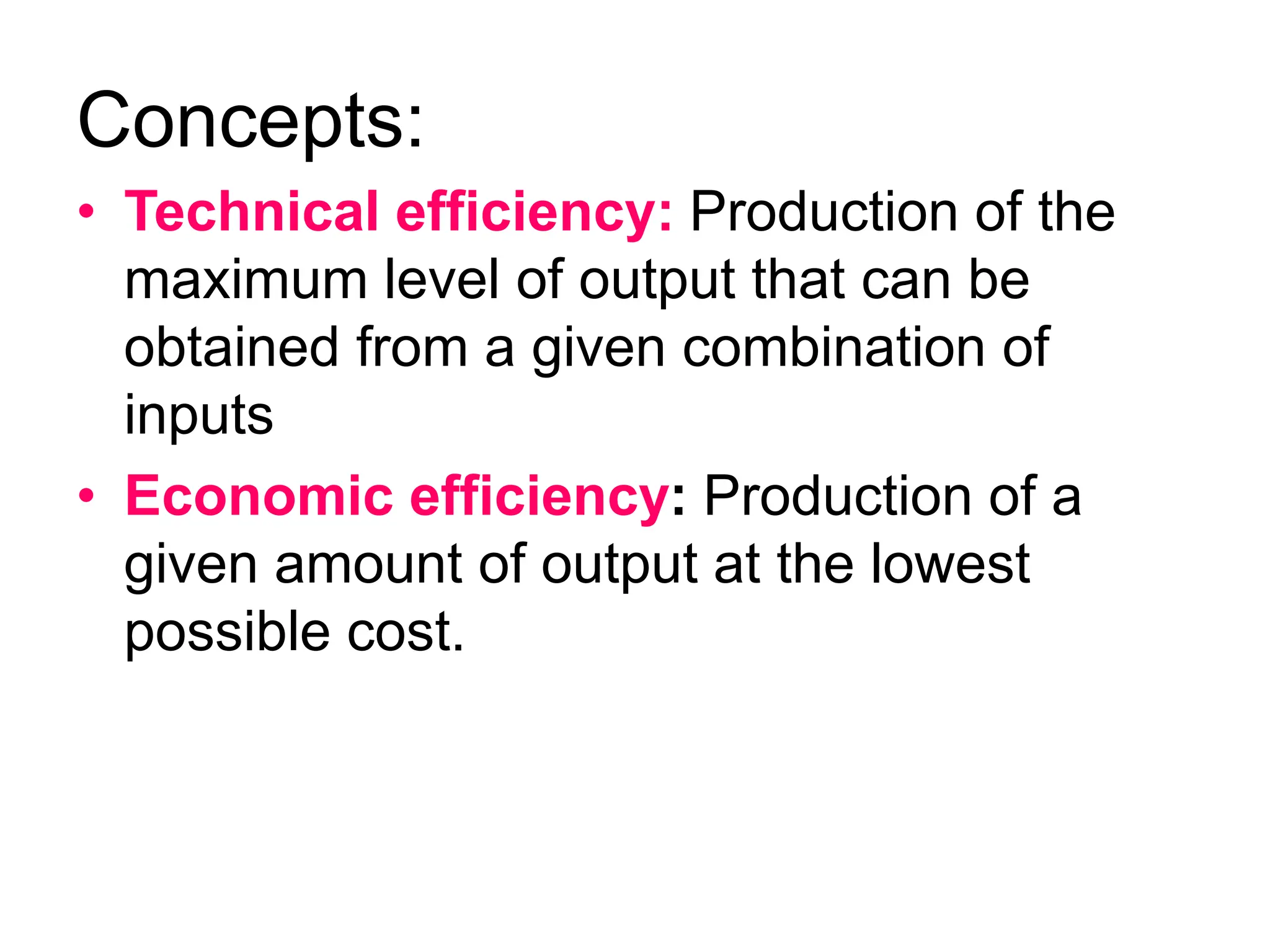

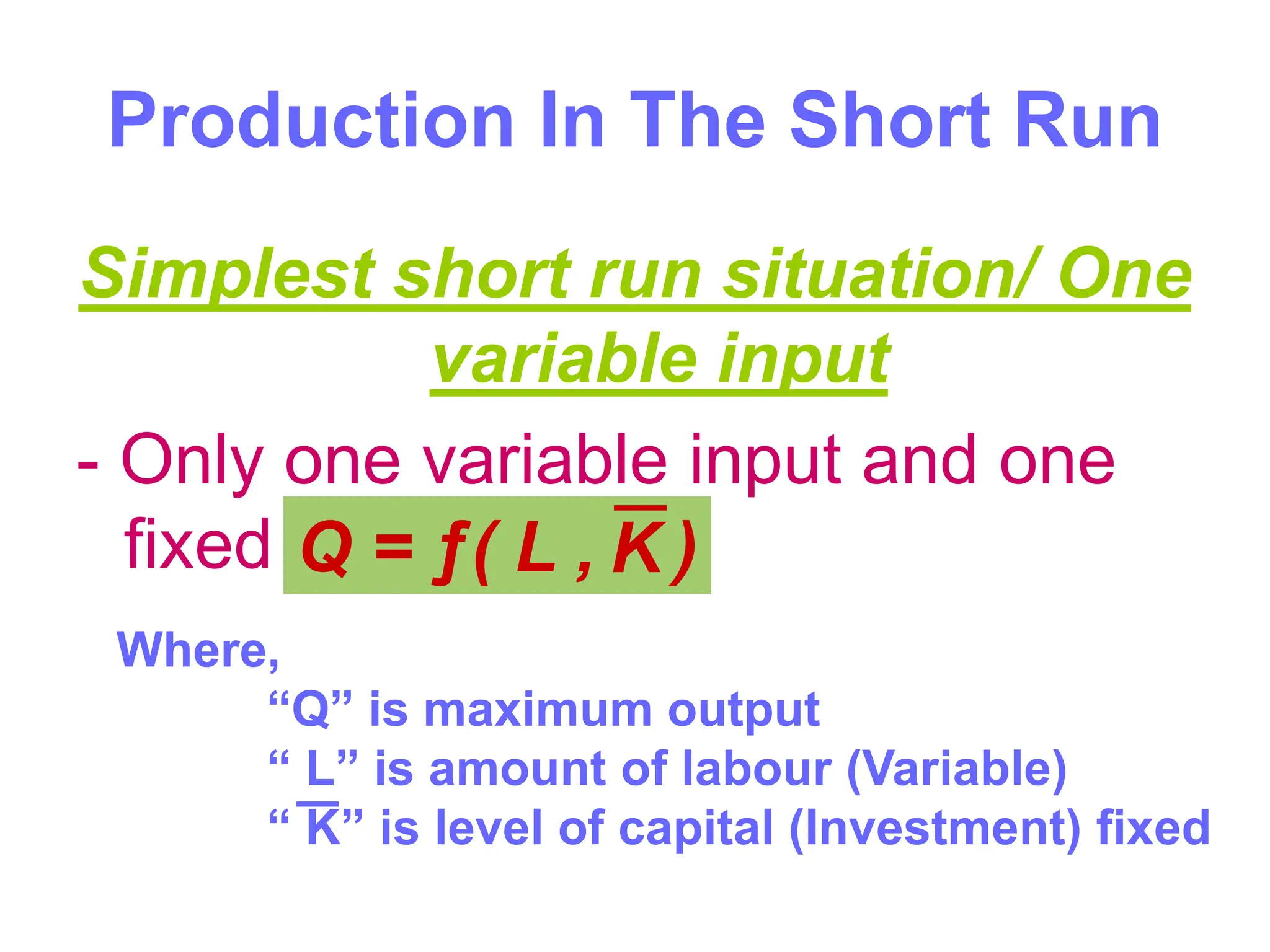

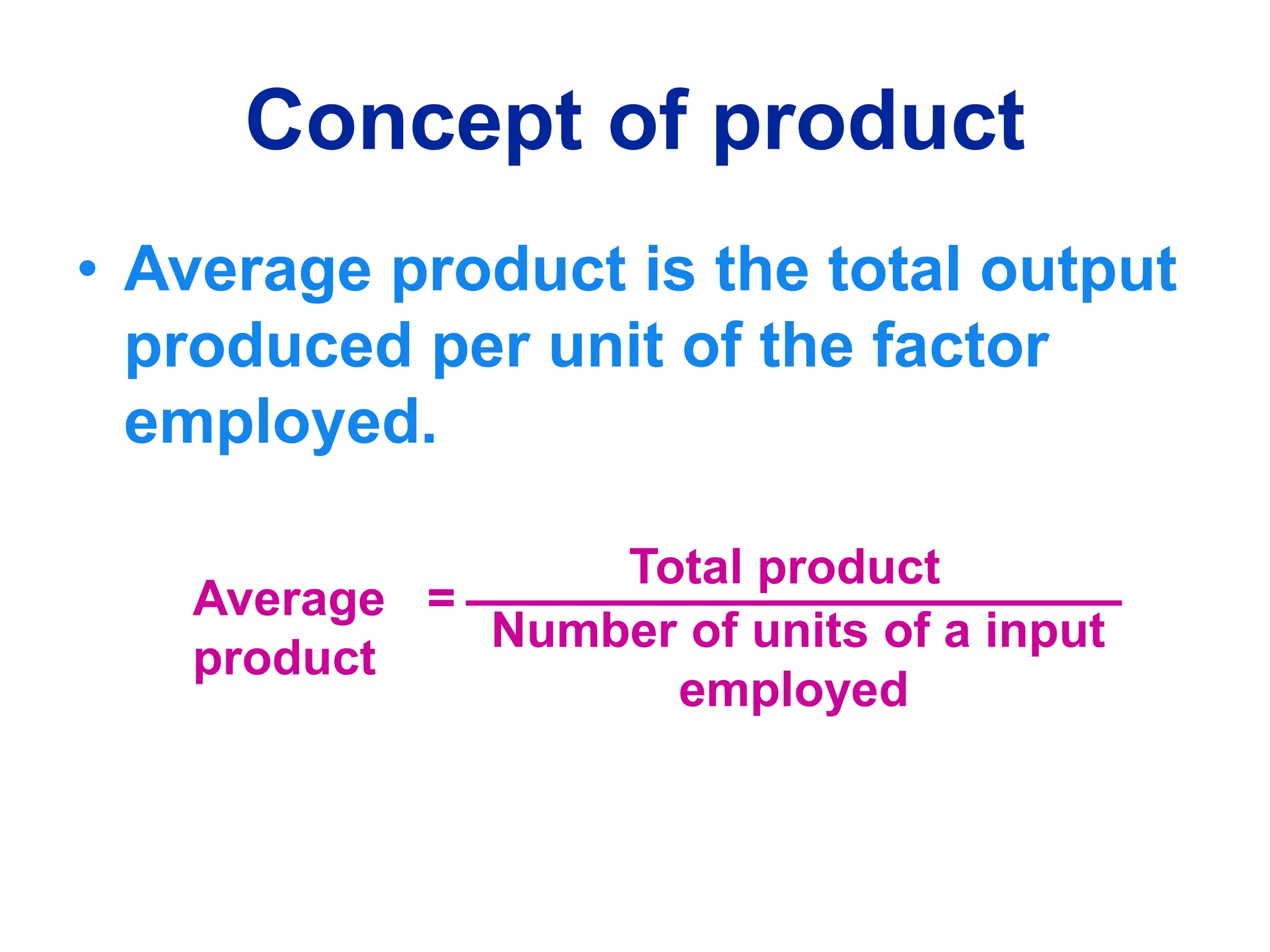

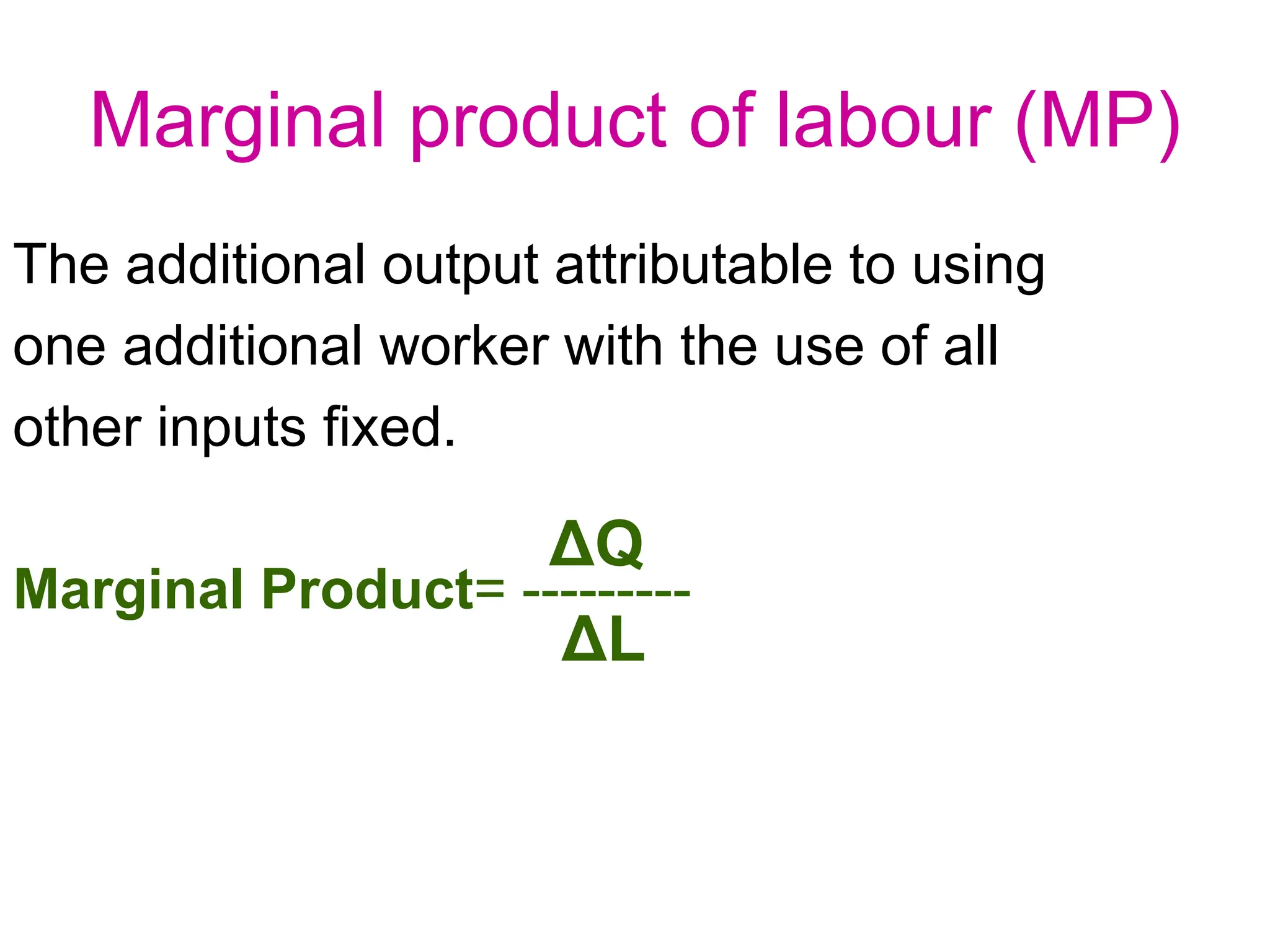

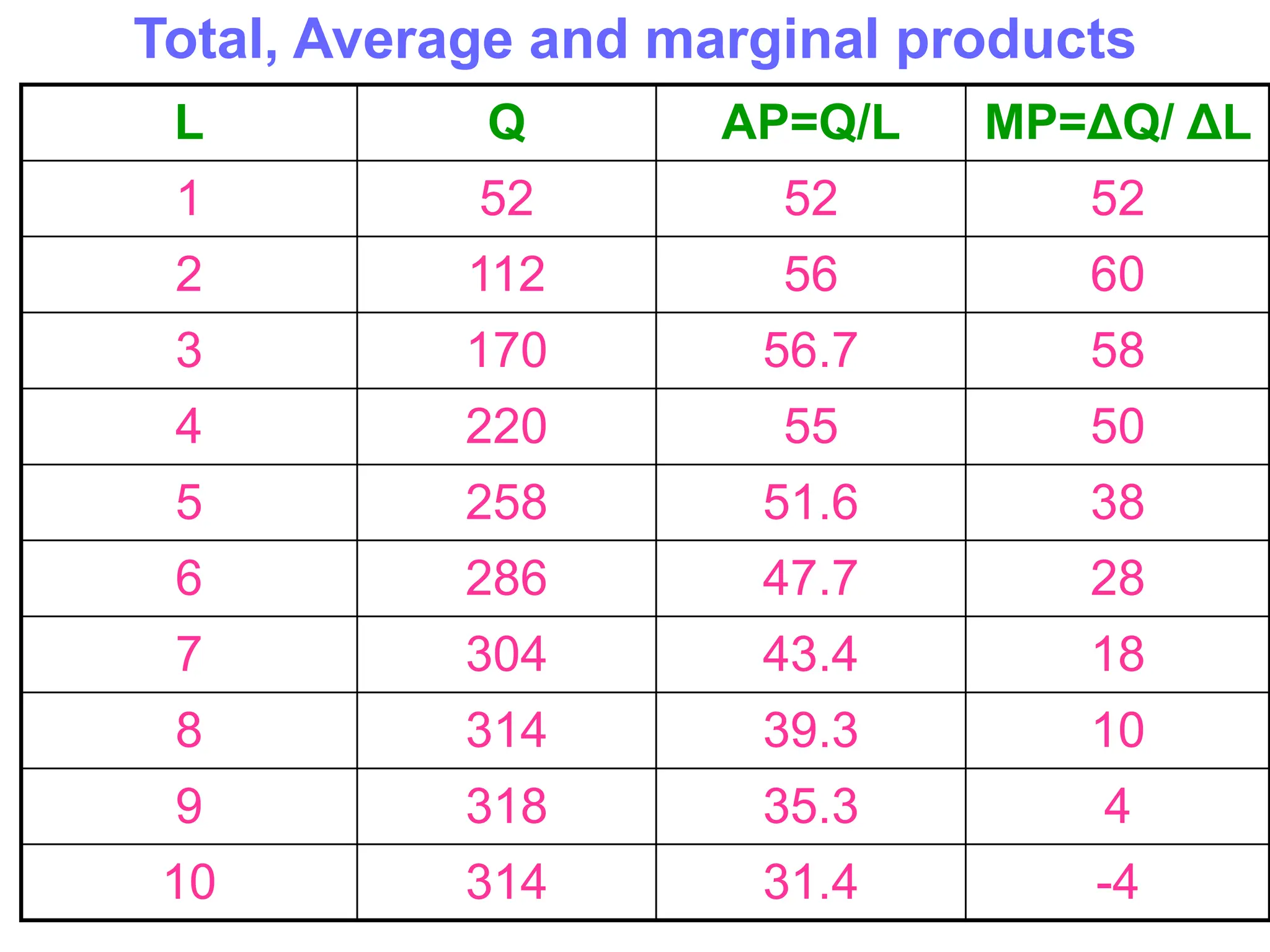

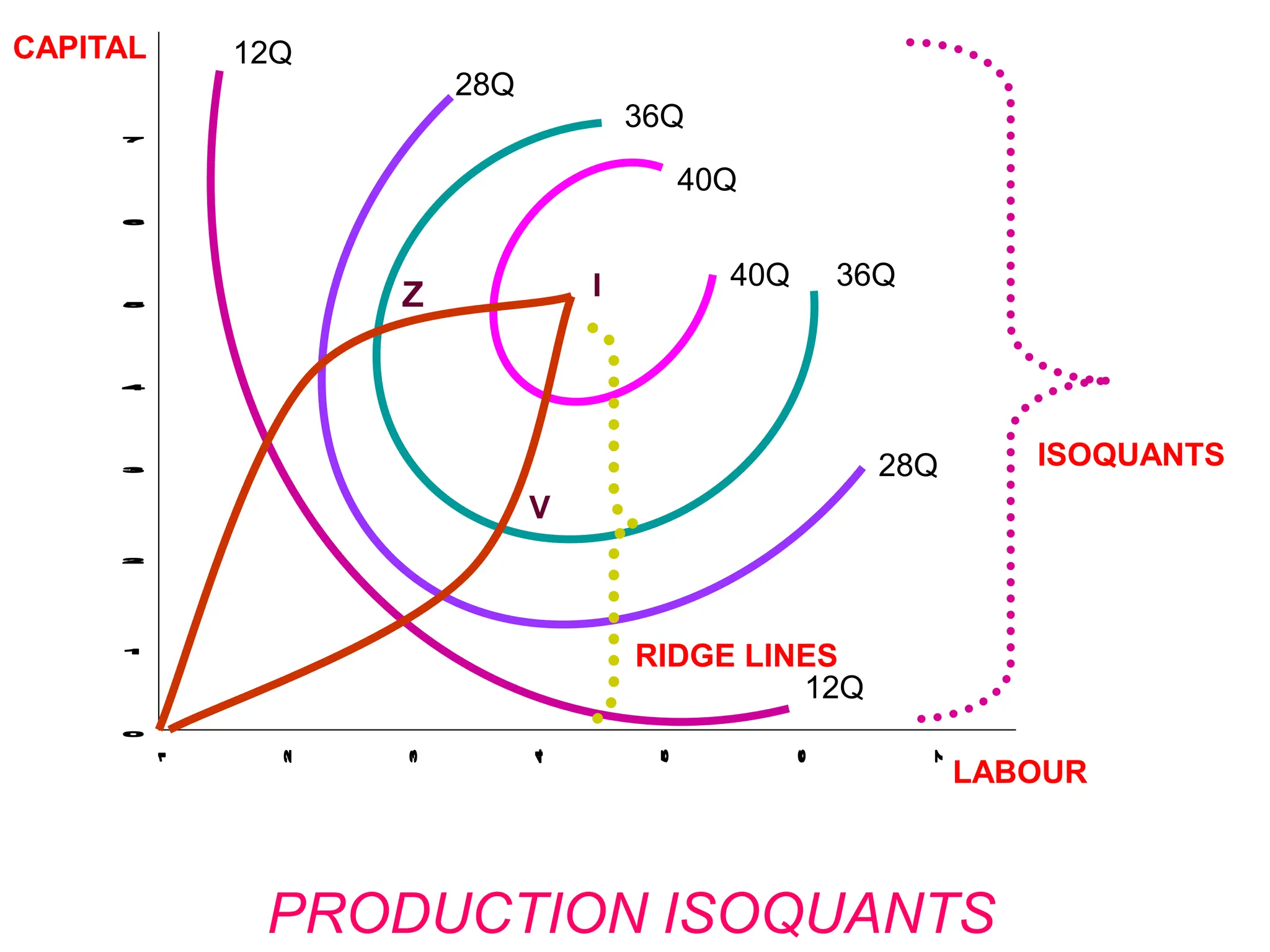

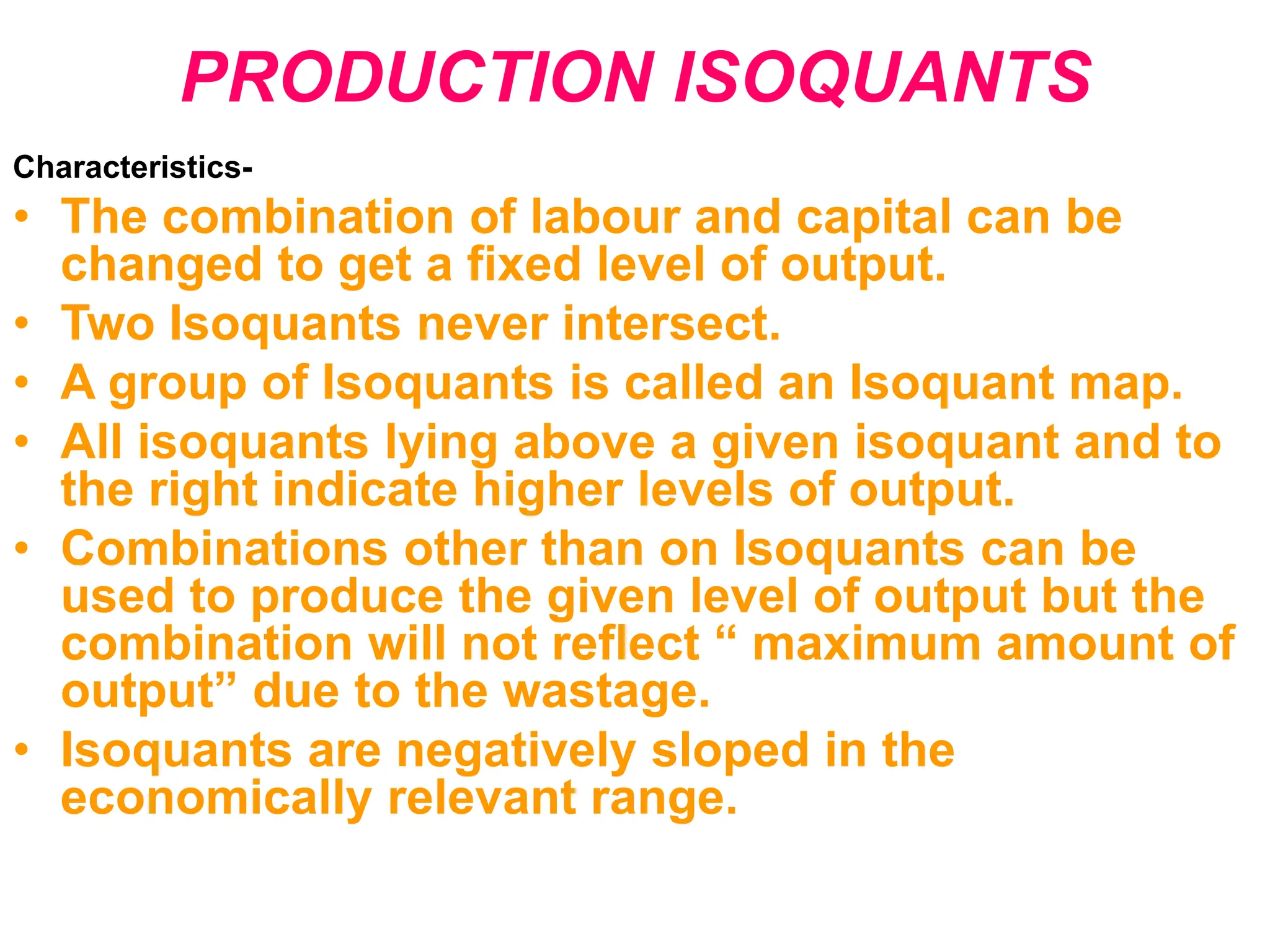

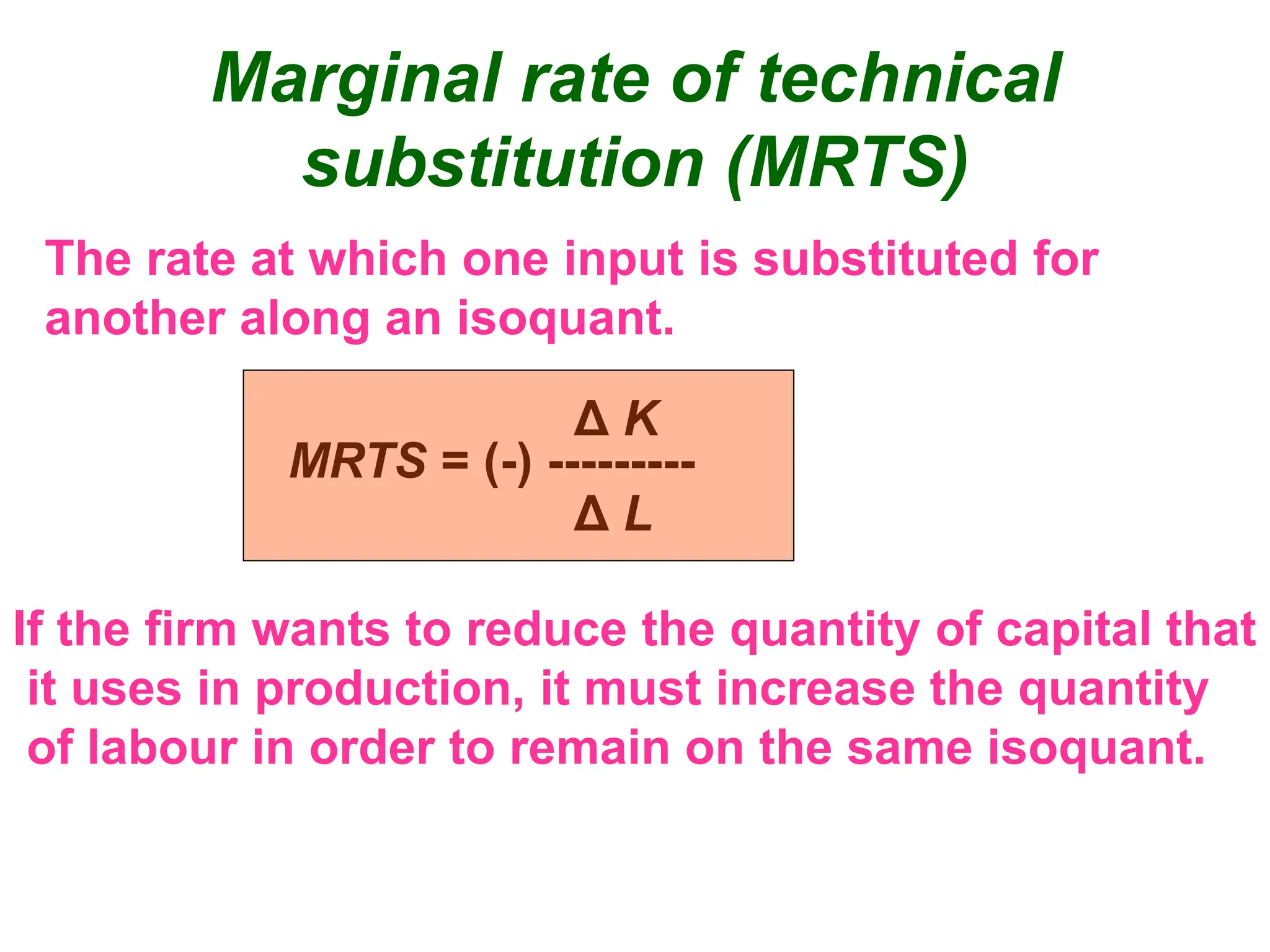

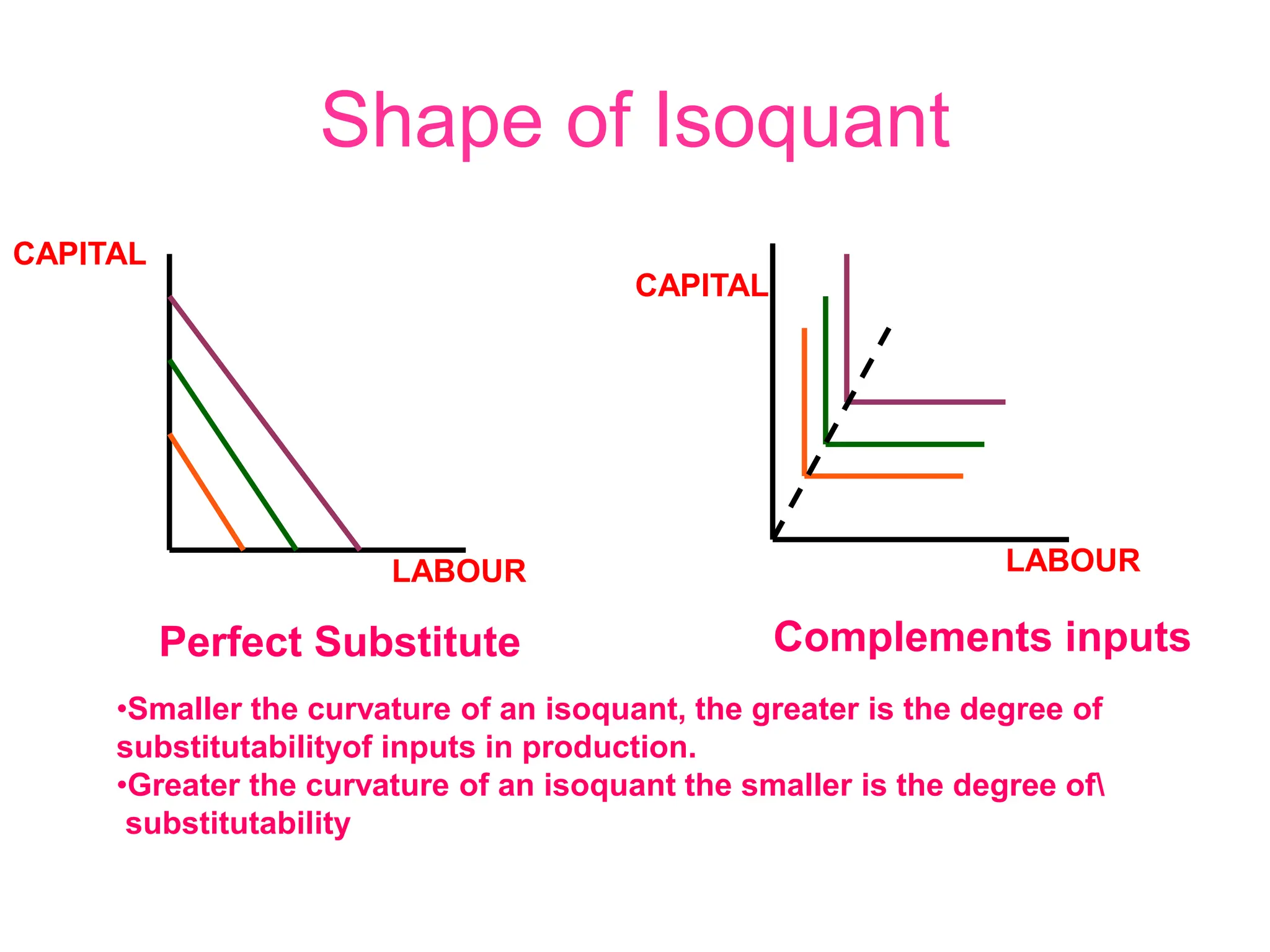

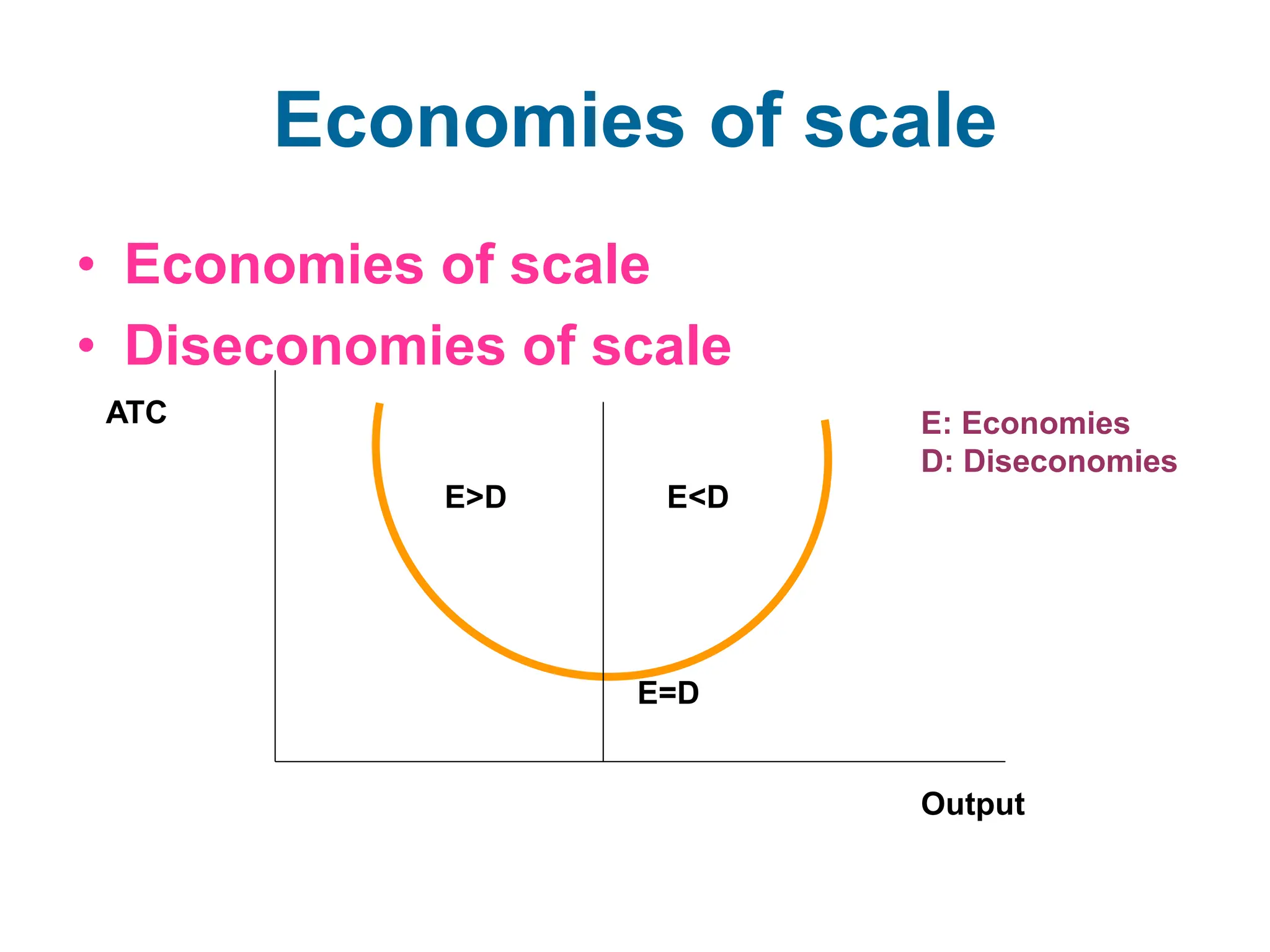

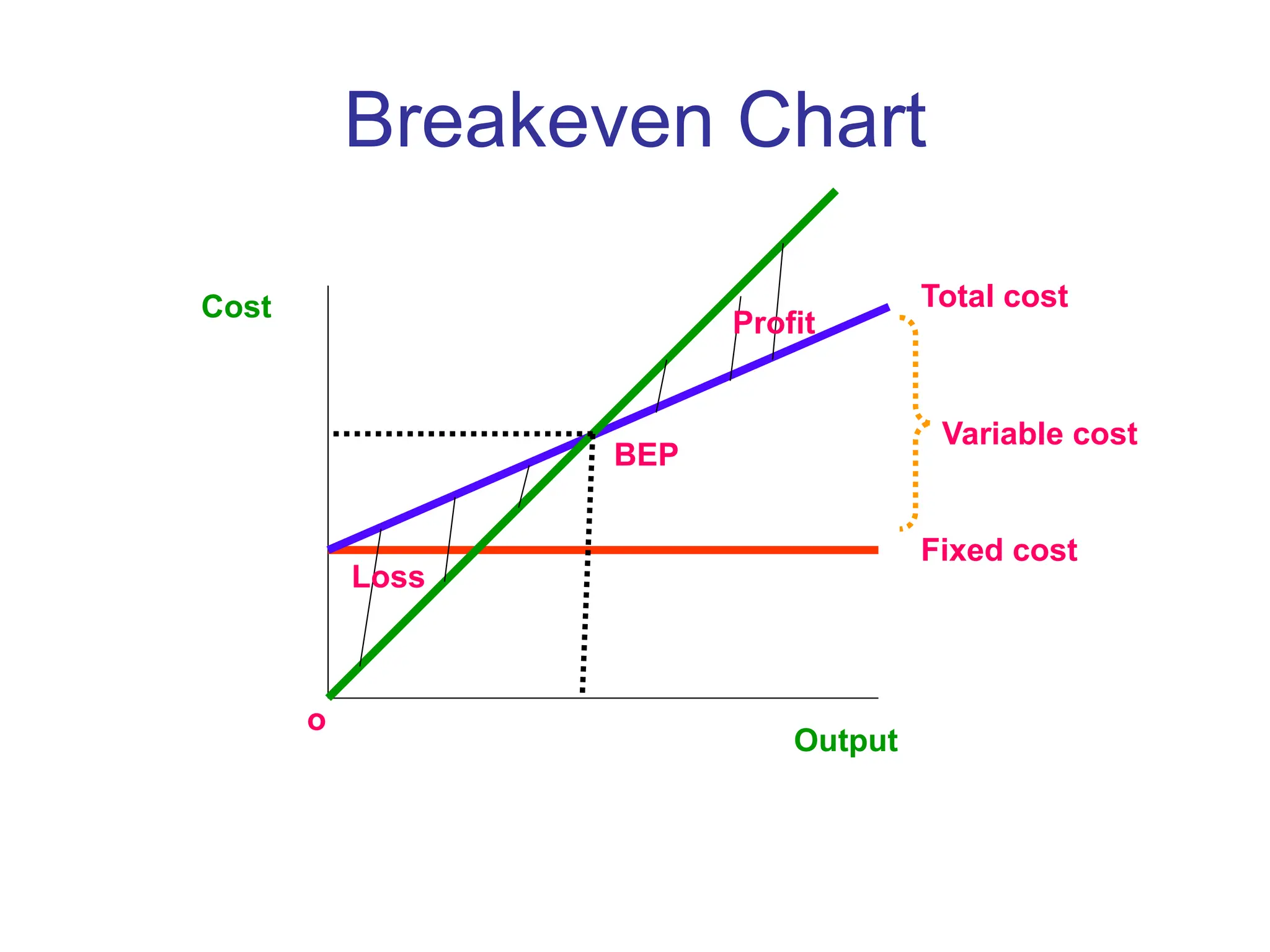

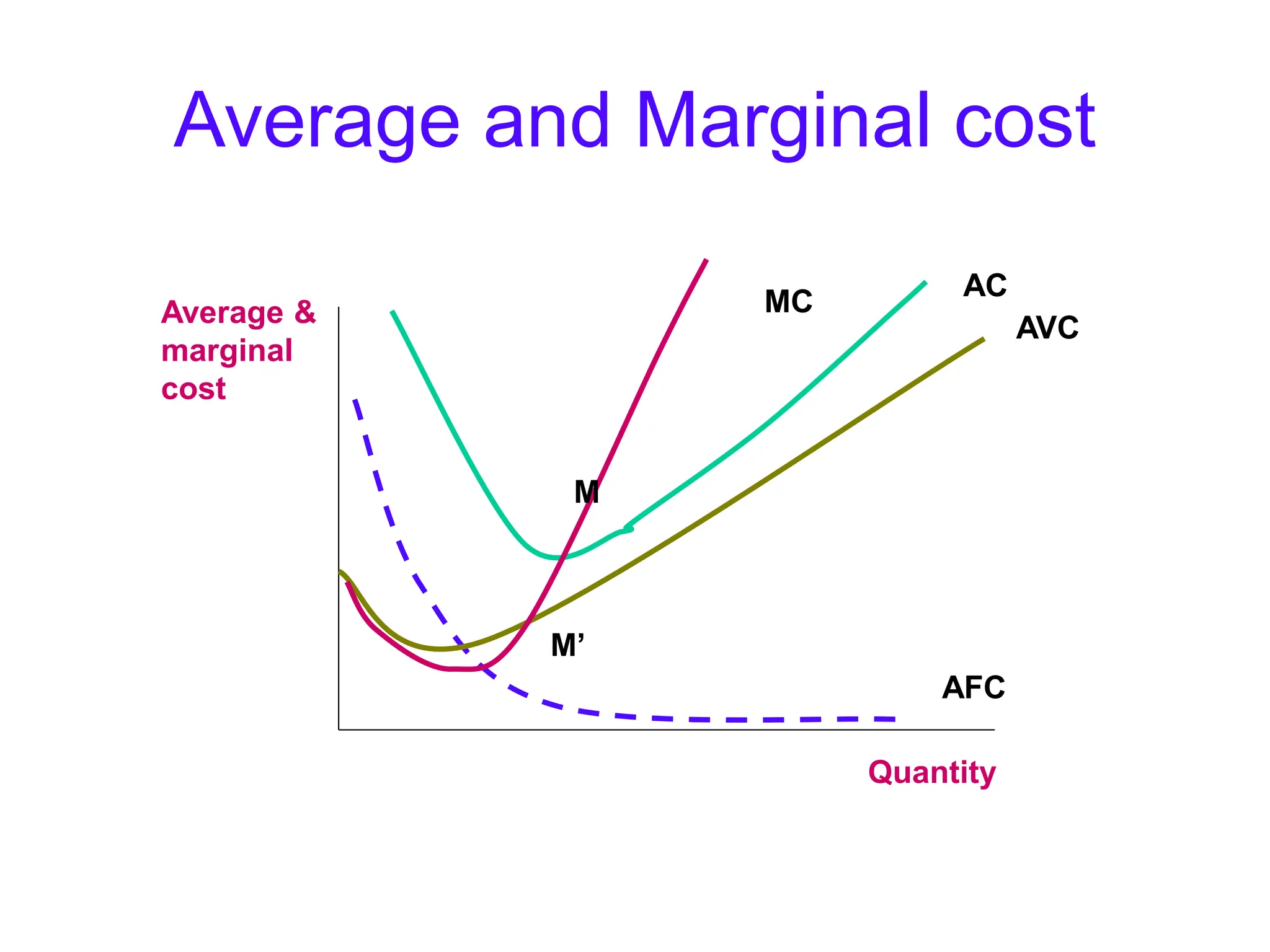

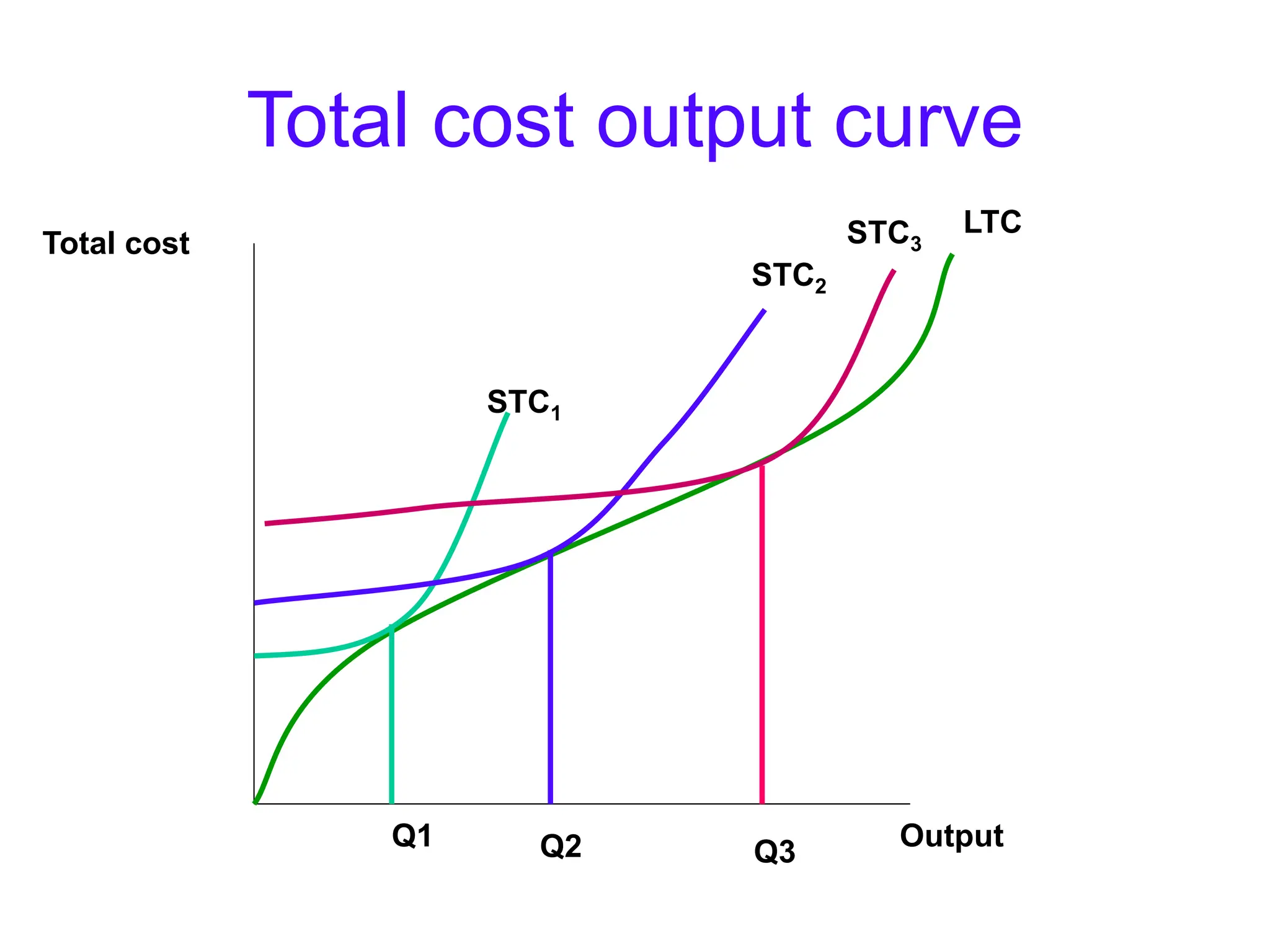

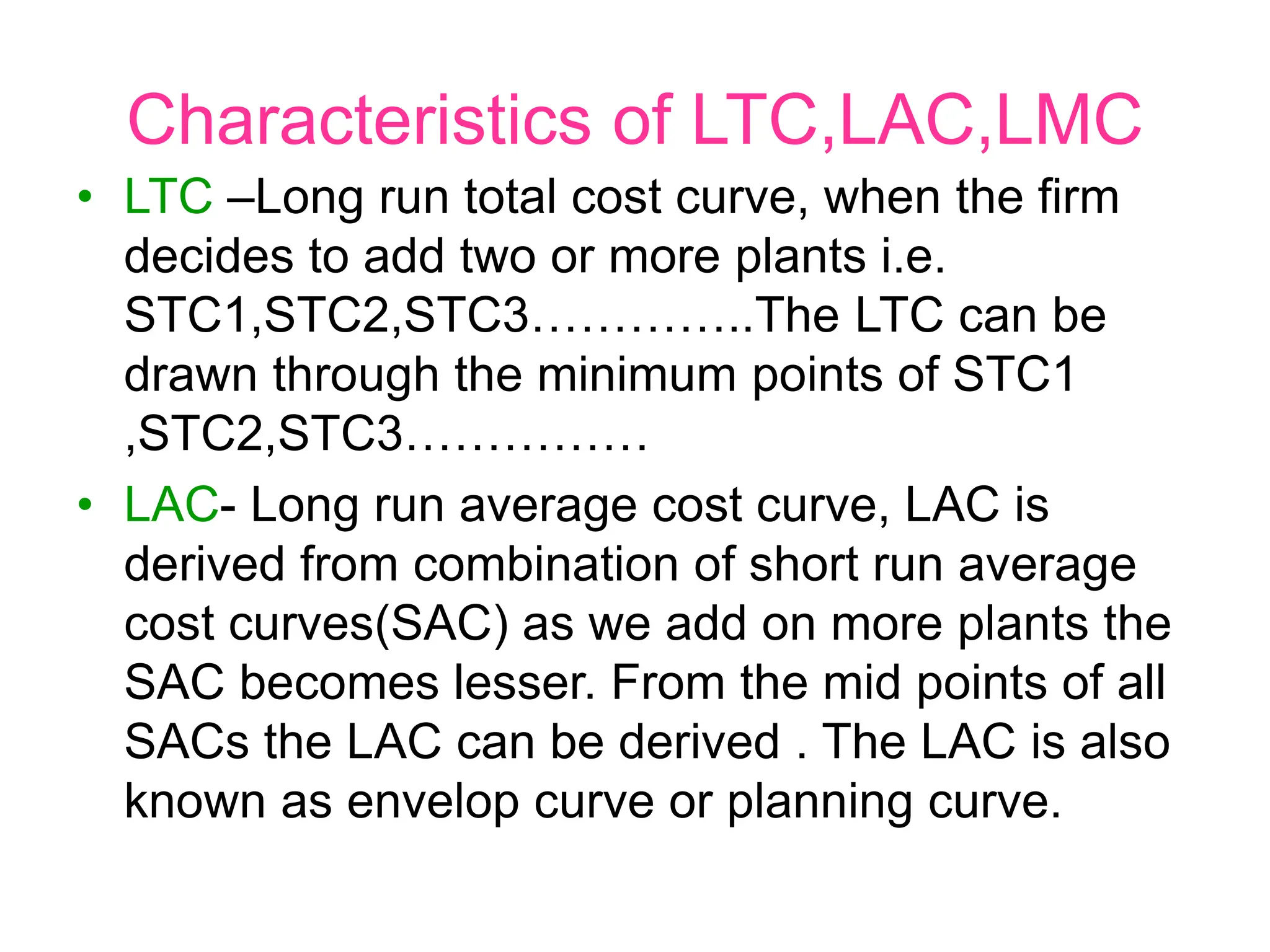

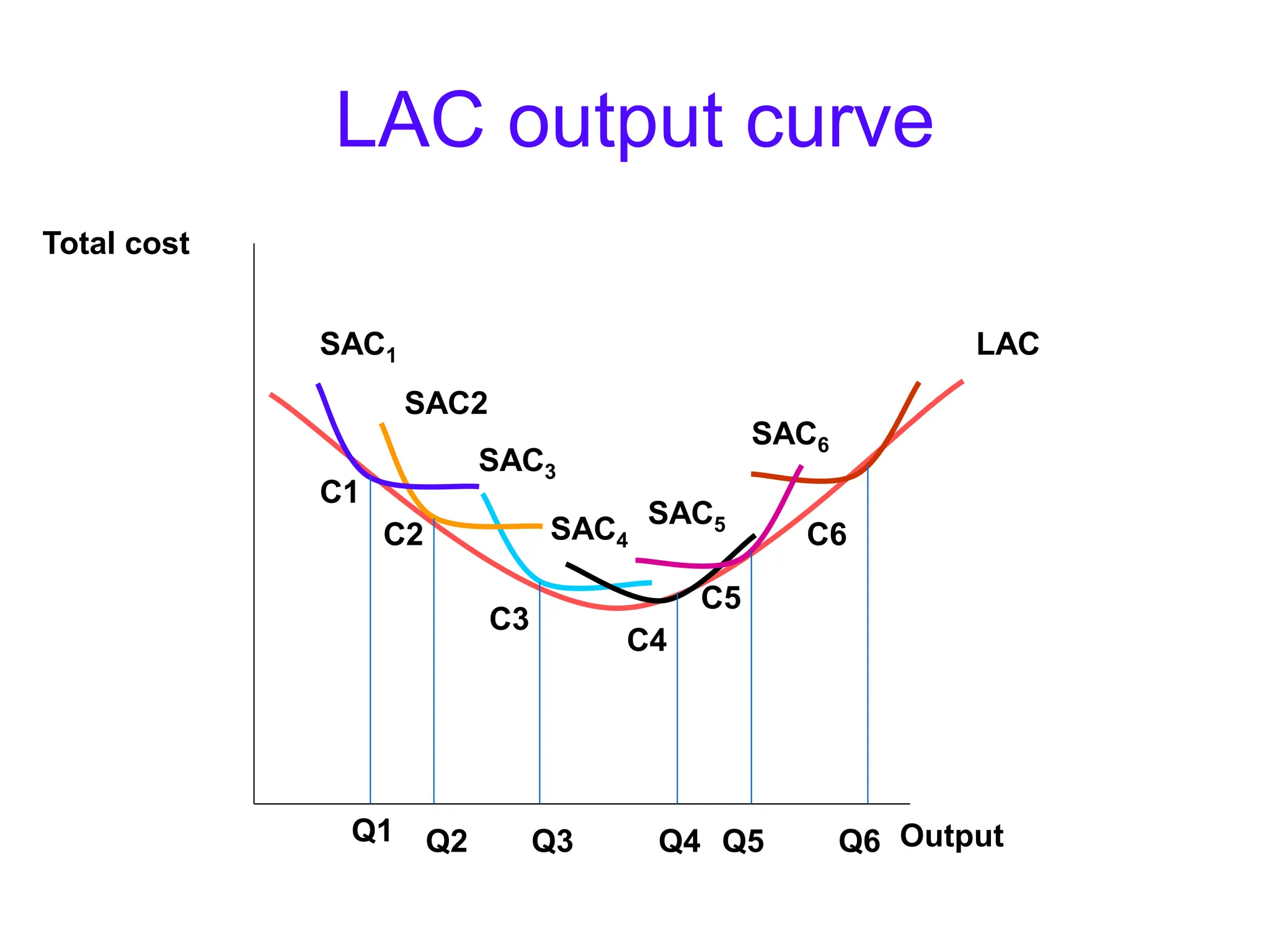

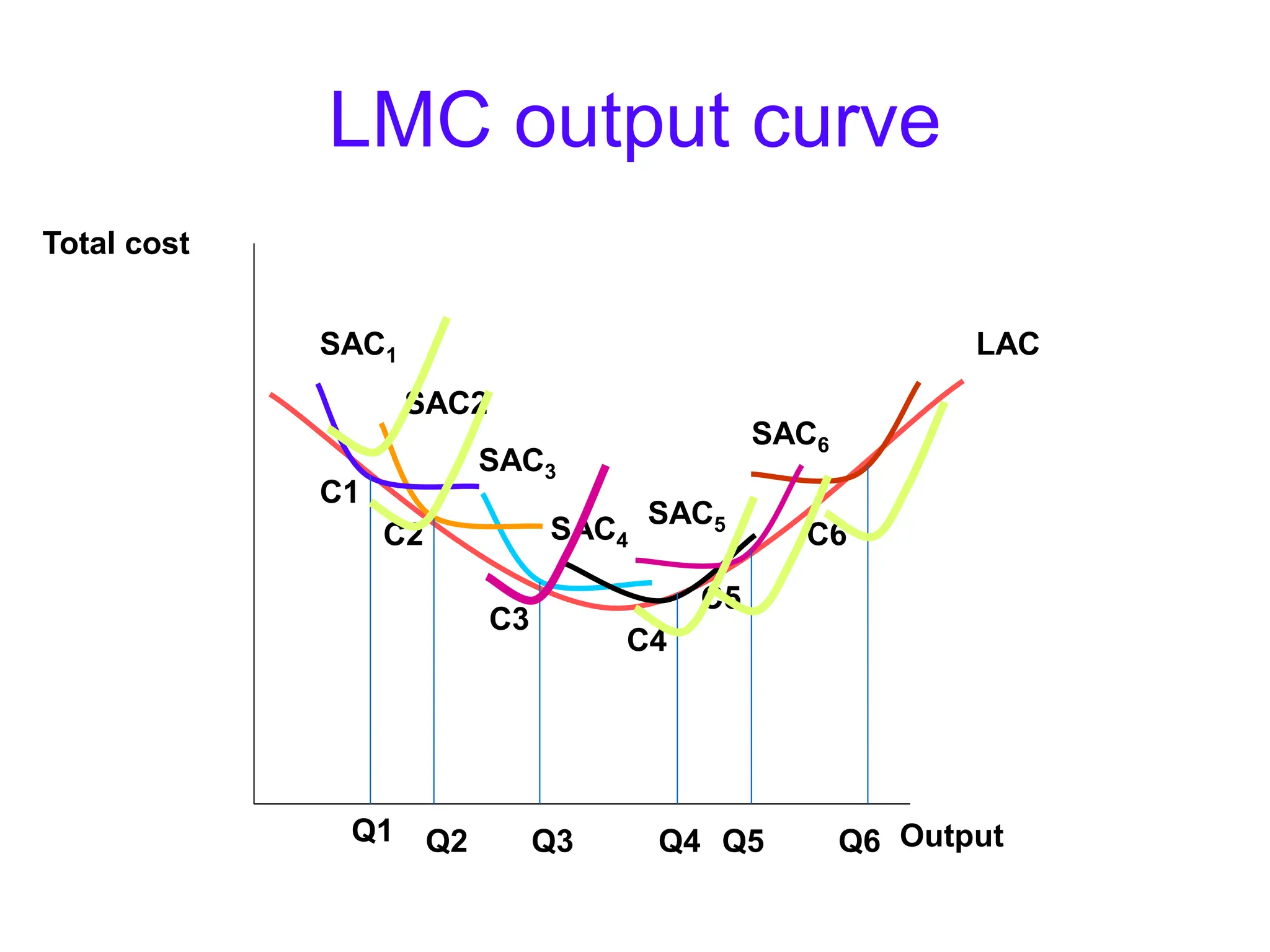

This document discusses key concepts related to production and cost analysis. It defines inputs, fixed and variable inputs, production functions, total product, average product, marginal product, and the law of diminishing marginal returns. It also covers production in the short run and long run, including isoquants, marginal rate of technical substitution, and returns to scale. The document analyzes costs including fixed, variable, and total costs. It discusses average and marginal costs, breakeven analysis, and economies of scale. Finally, it covers long run cost relationships including long run total cost, average cost, and marginal cost curves.