This document defines production and costs, and discusses the theory of production and cost. It covers:

1) Definitions of production, inputs, production functions, and the relationship between inputs and output.

2) The characteristics of short-run and long-run production periods and production functions.

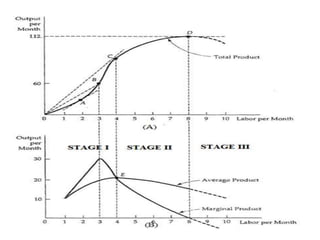

3) The measurement of total product, average product, and marginal product and how they relate at different stages of production.

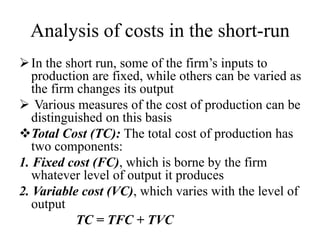

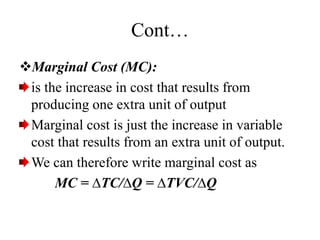

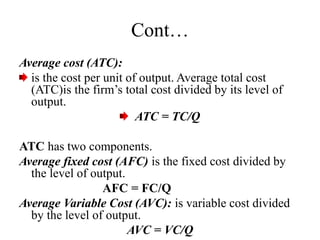

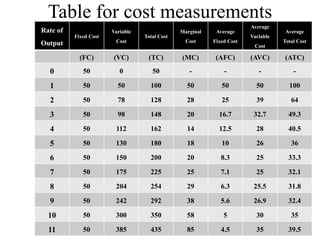

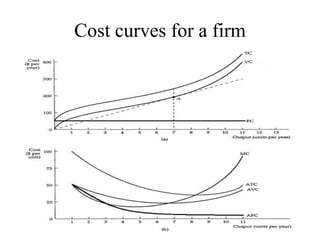

4) Cost concepts including total, fixed, variable, marginal, average, and their relationships as depicted through cost curves.