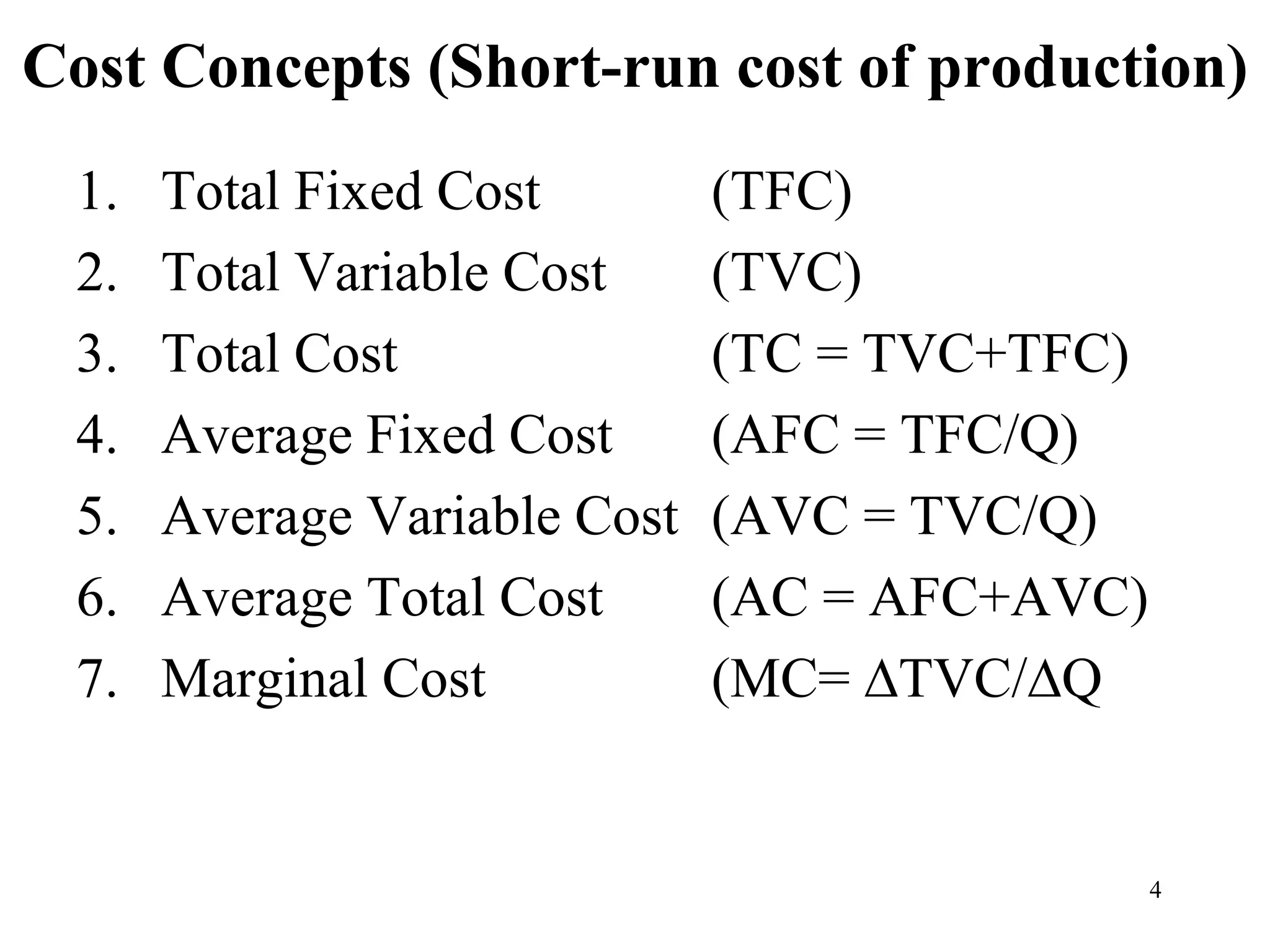

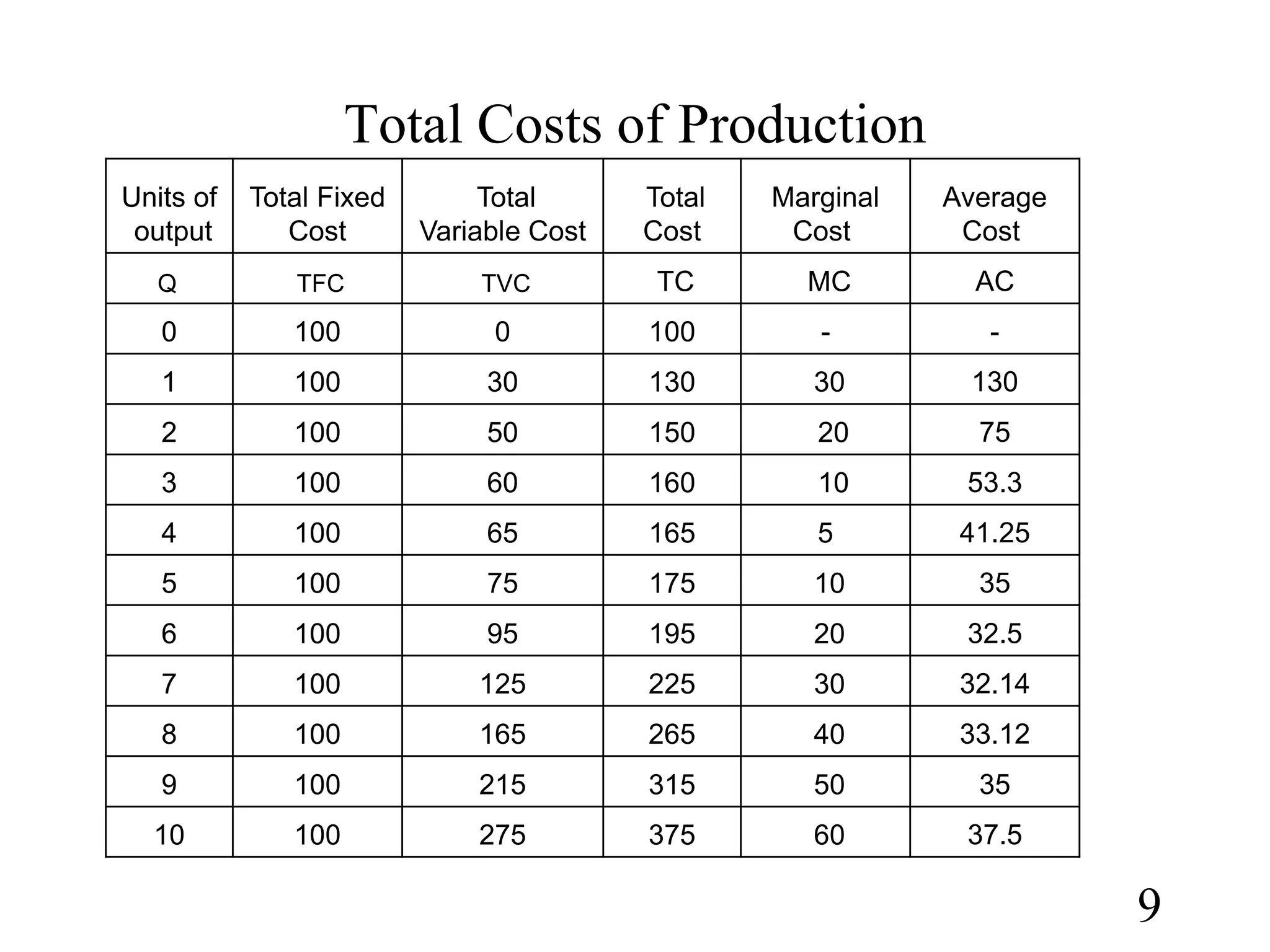

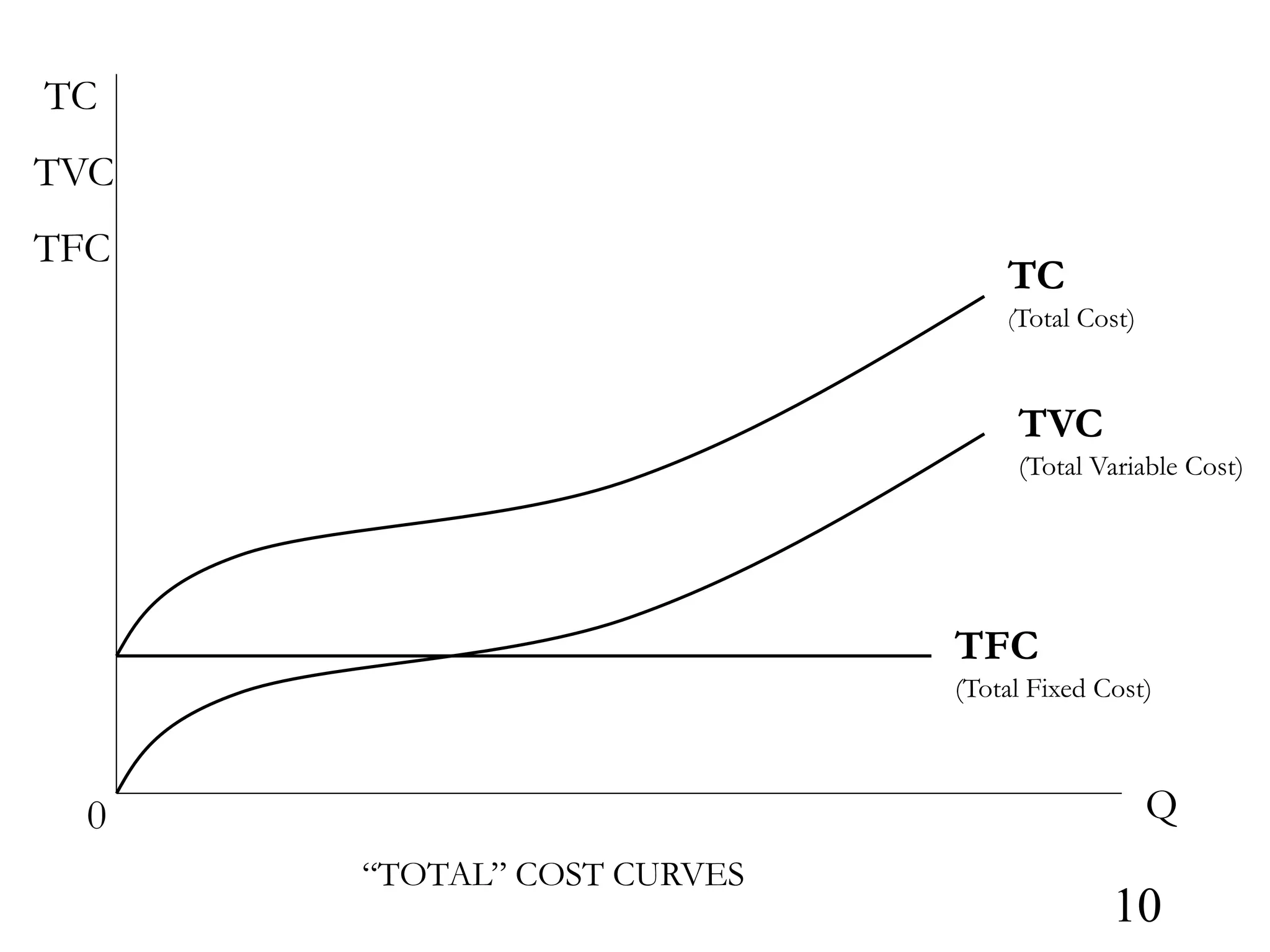

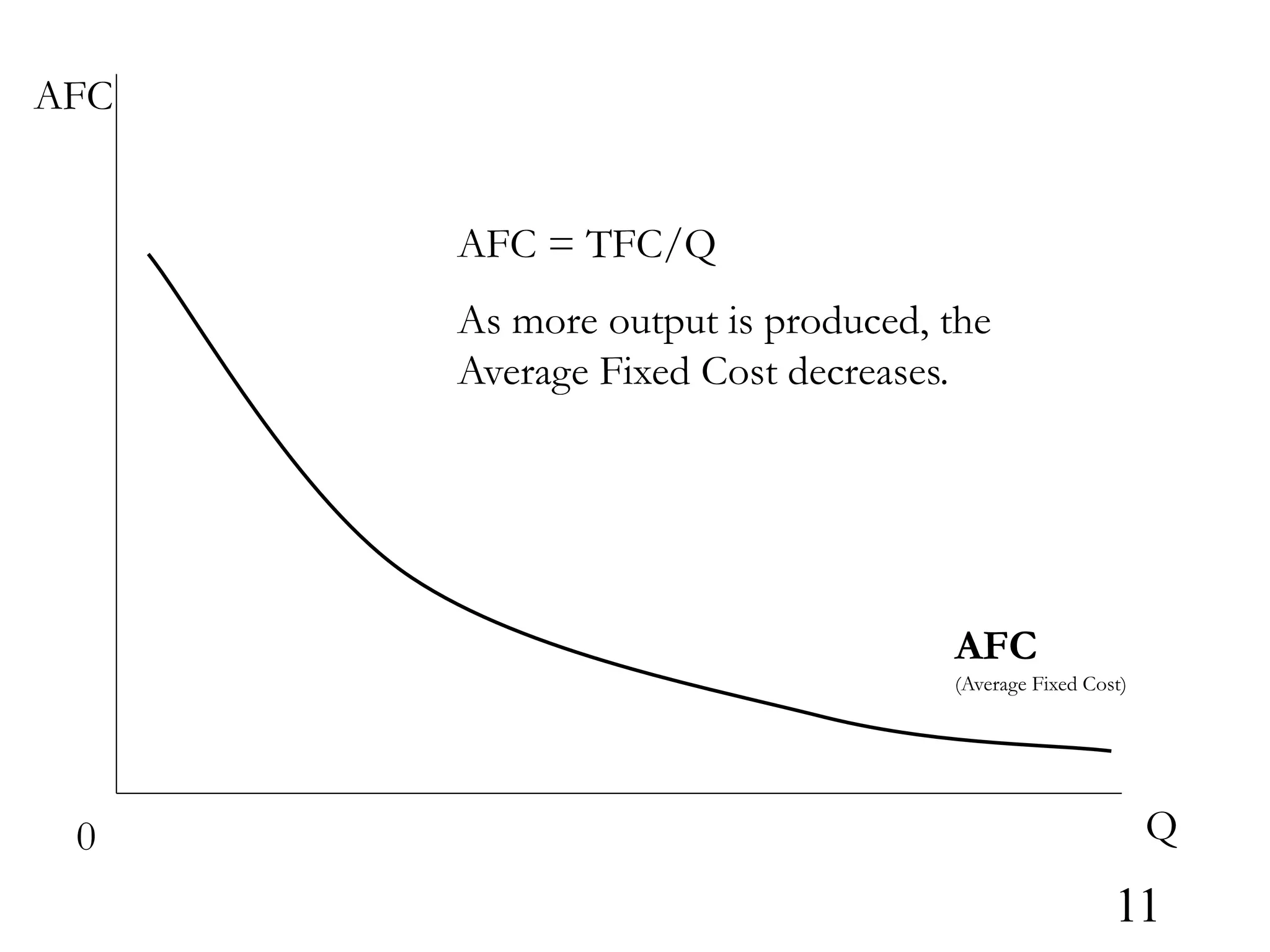

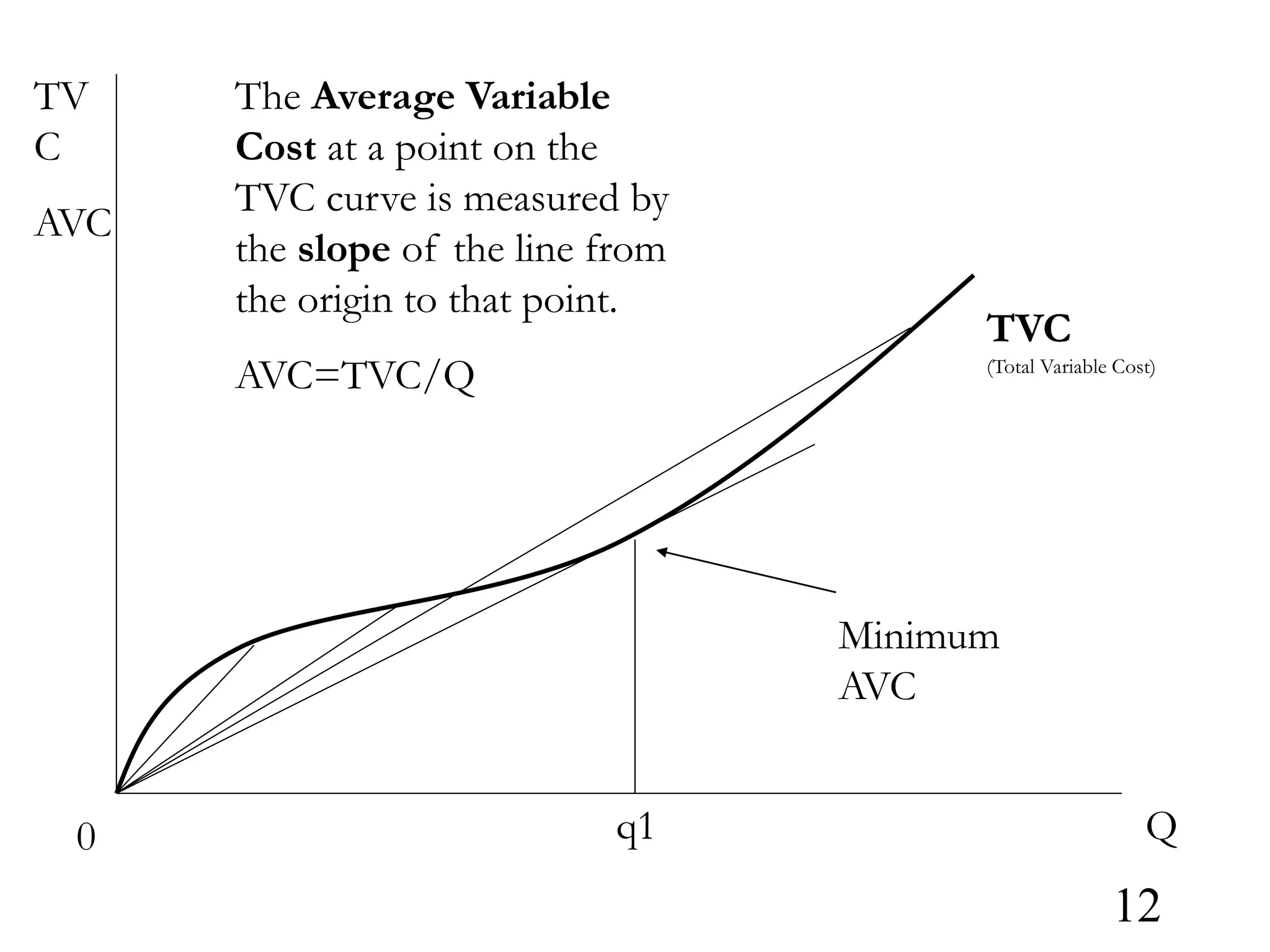

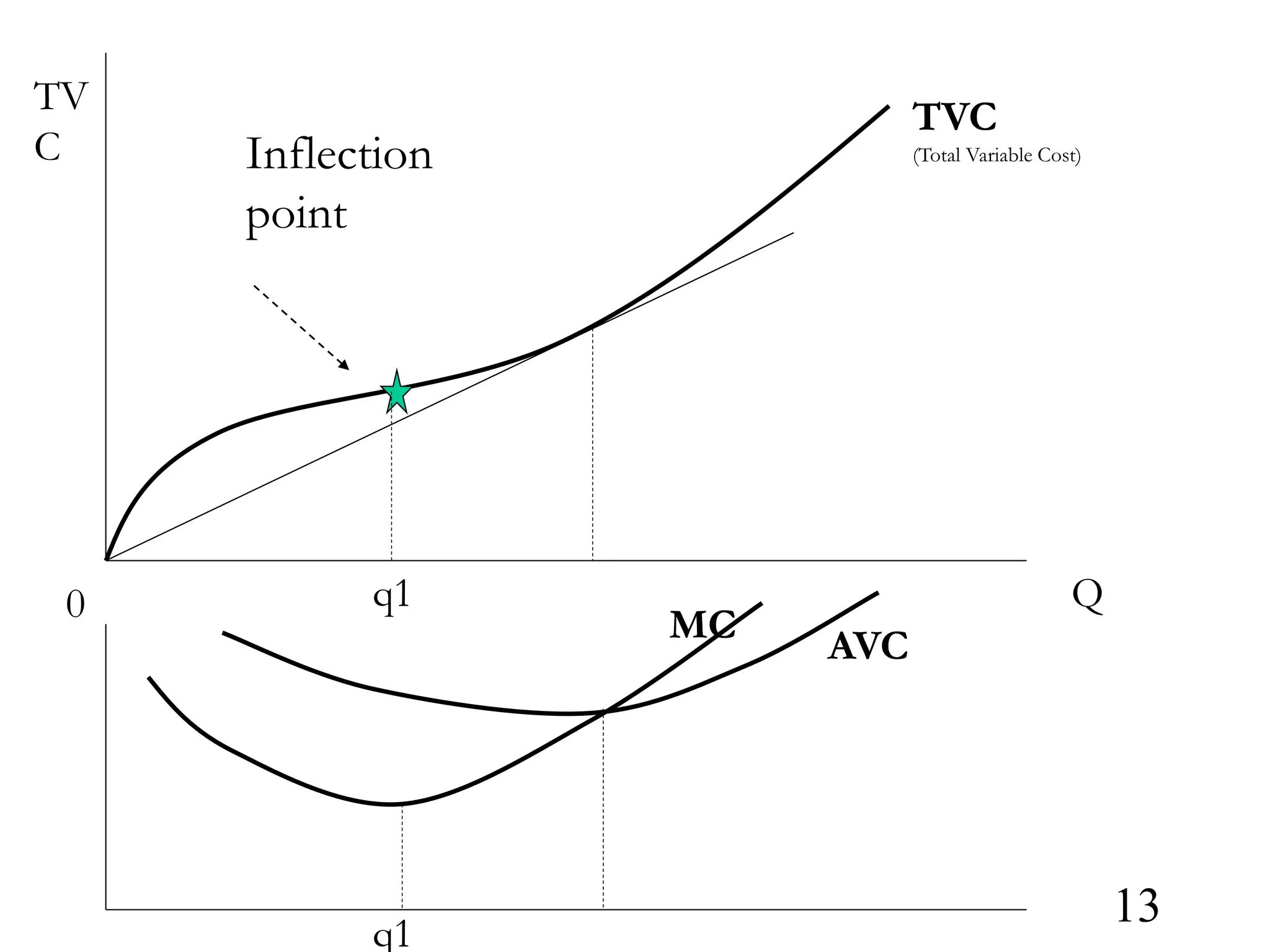

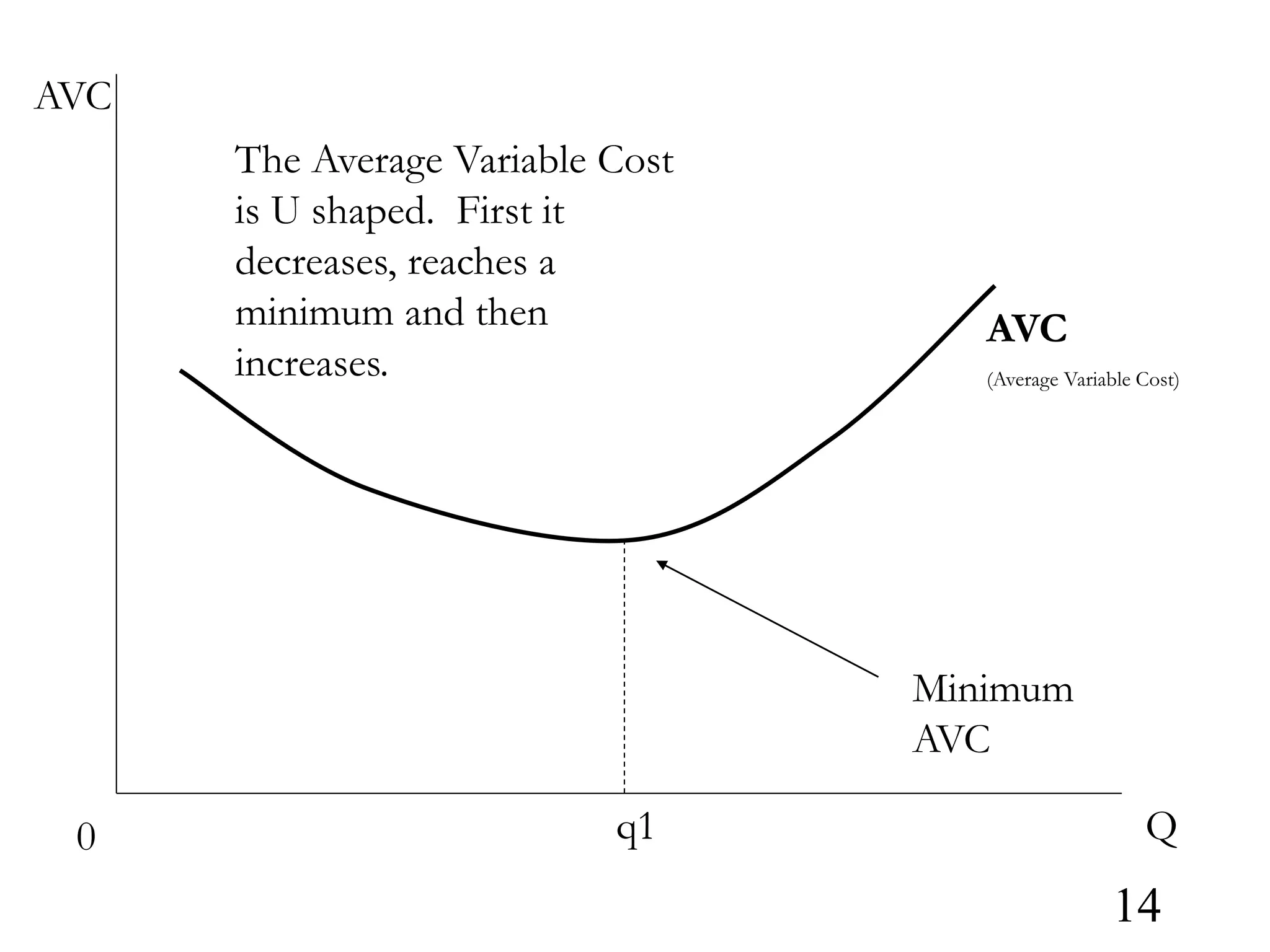

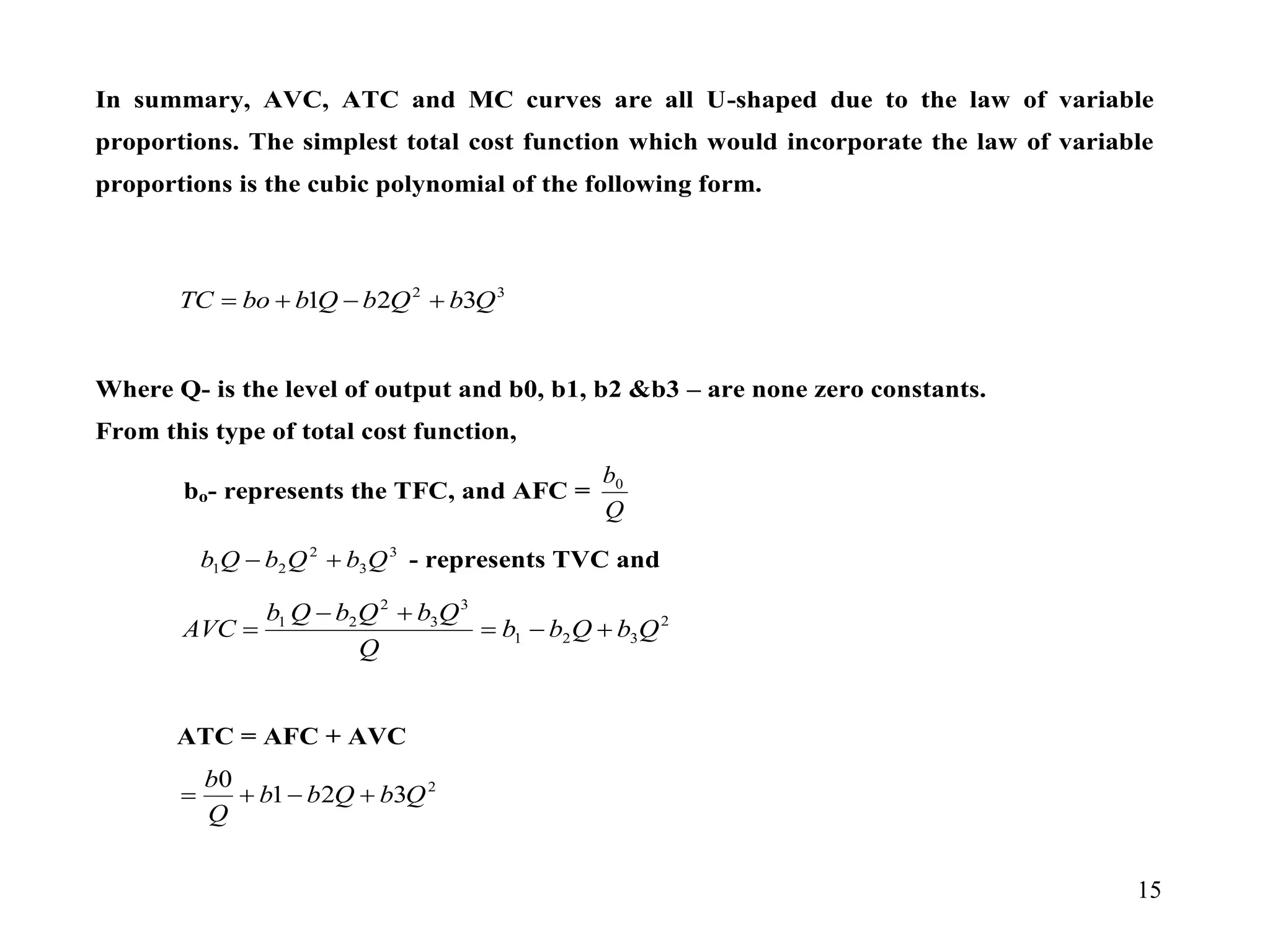

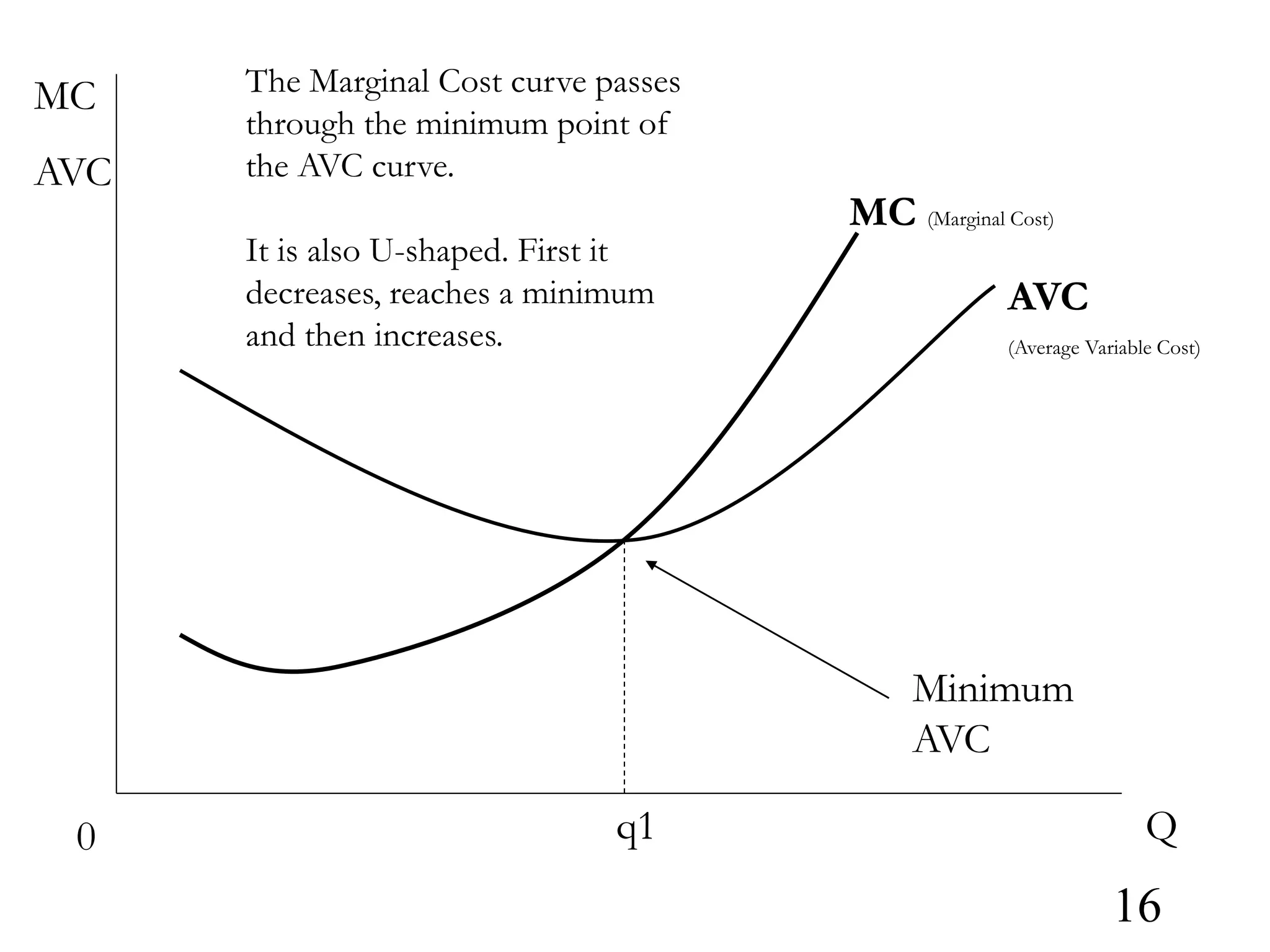

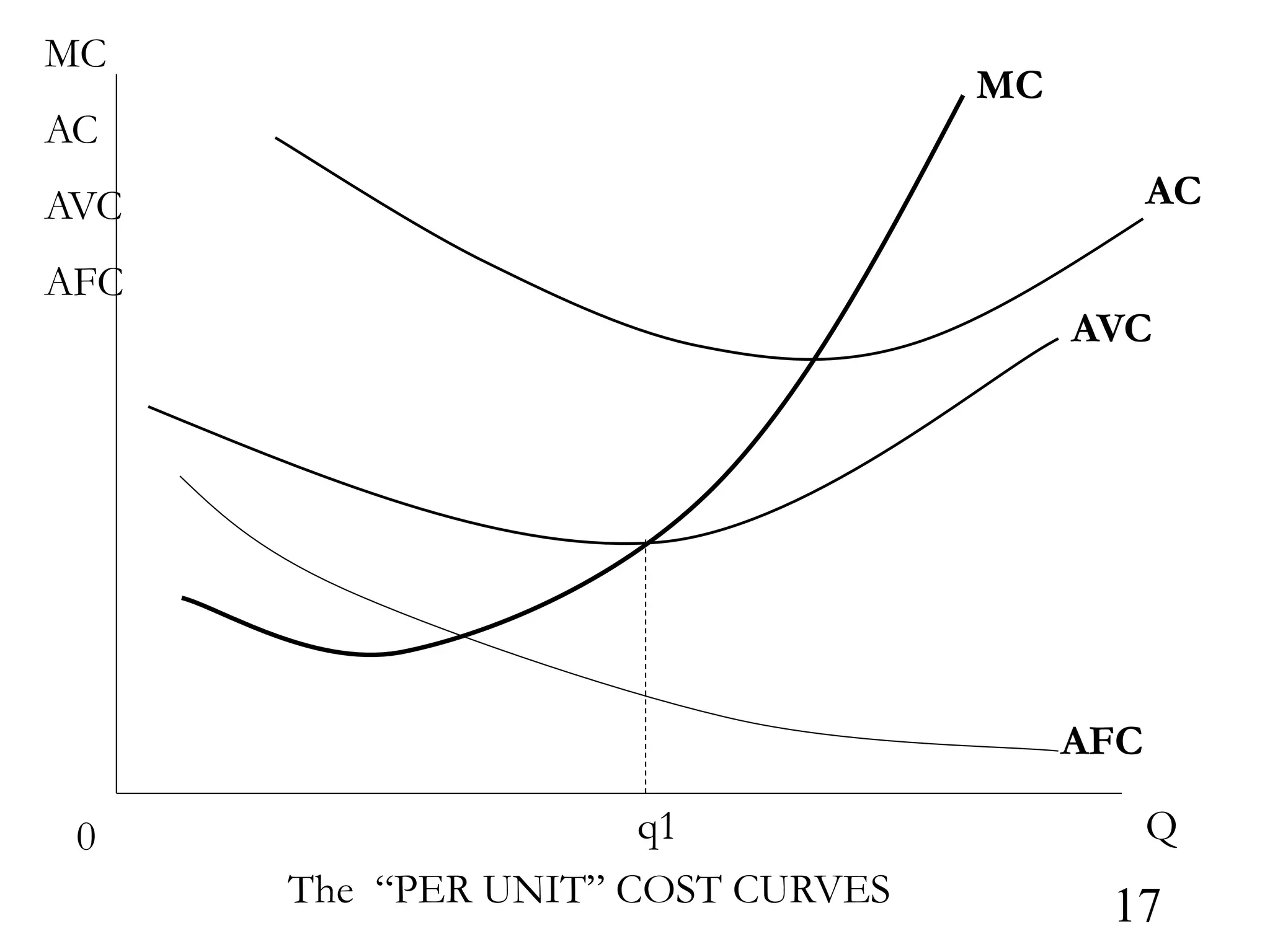

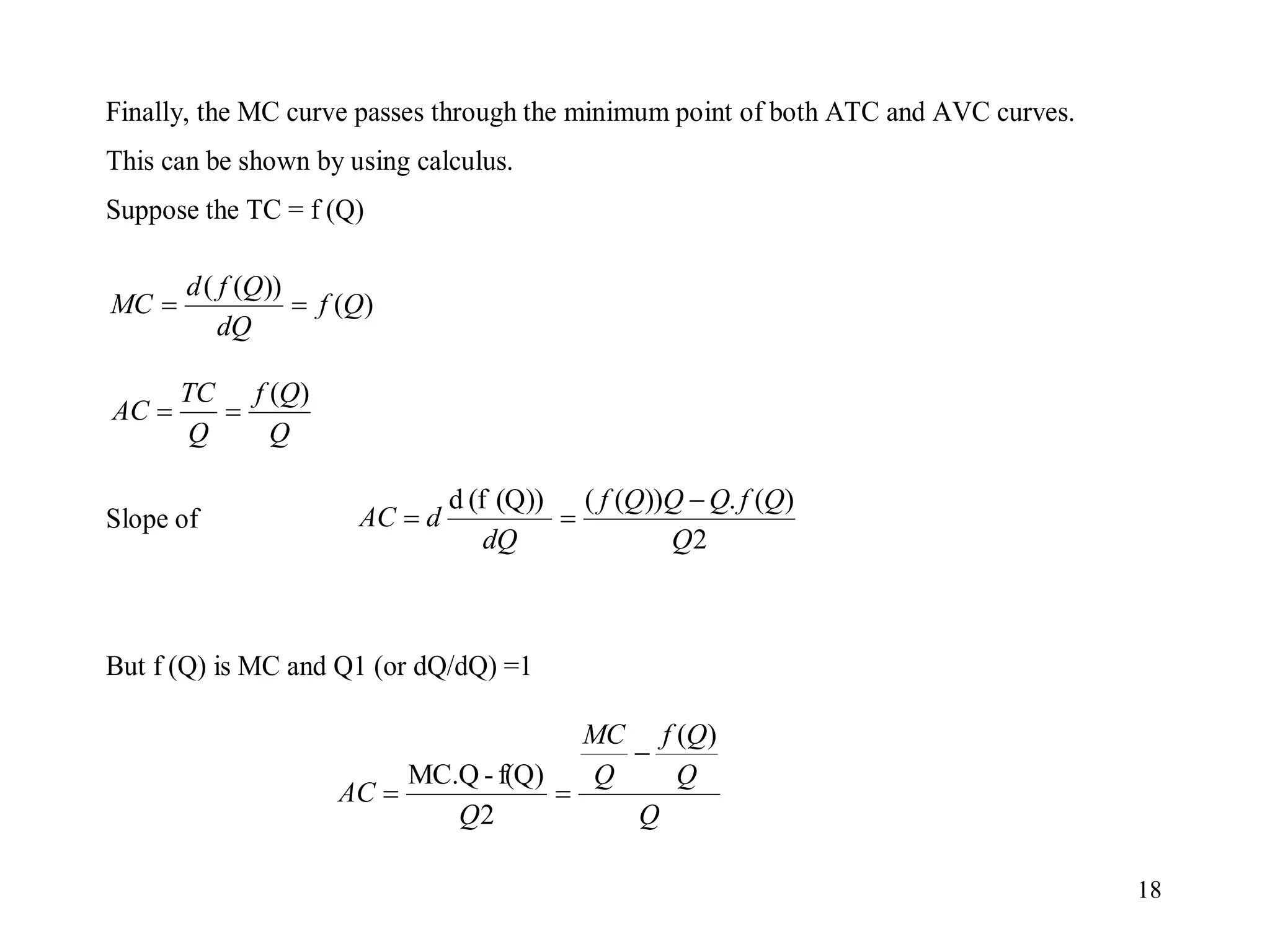

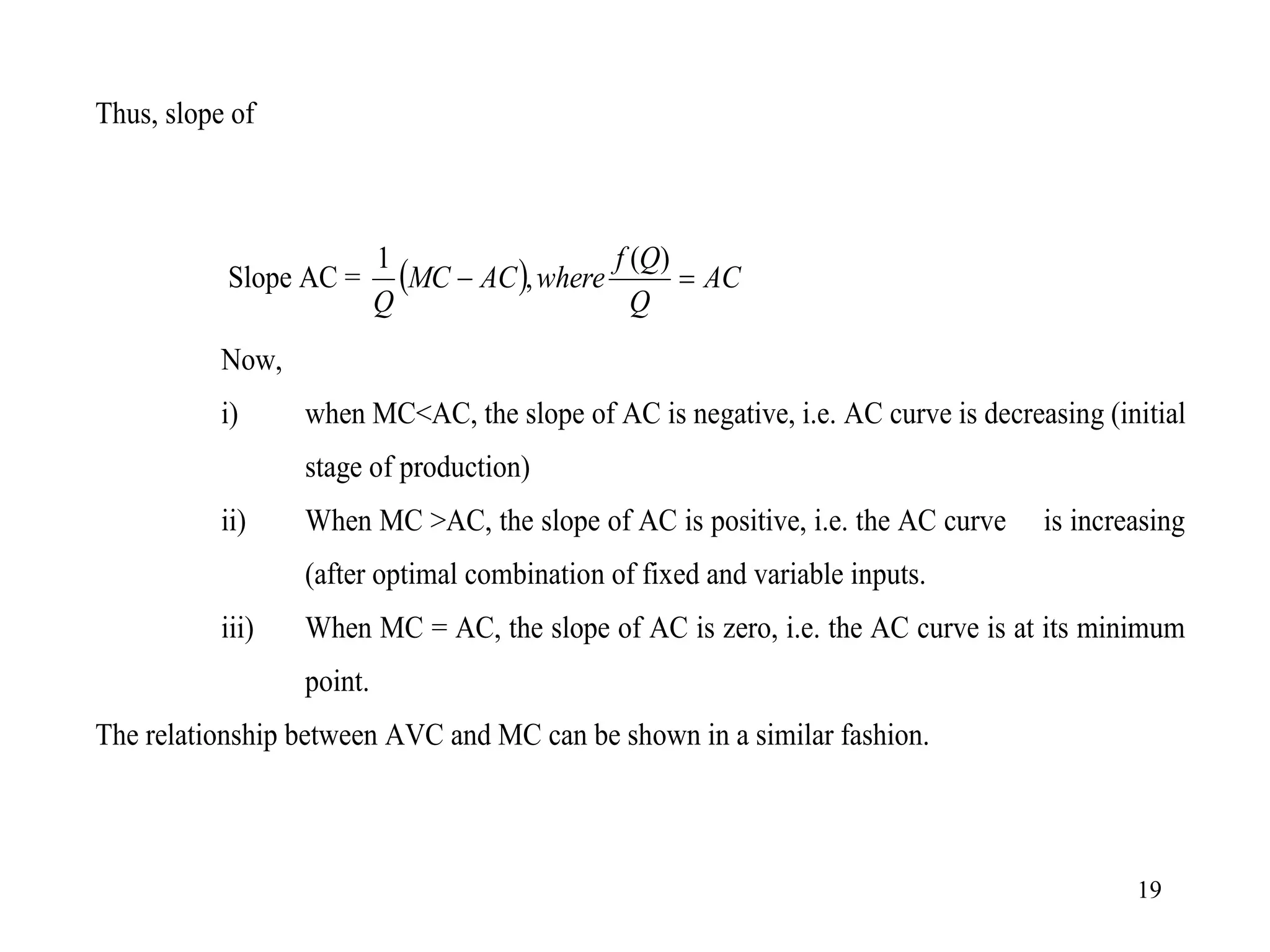

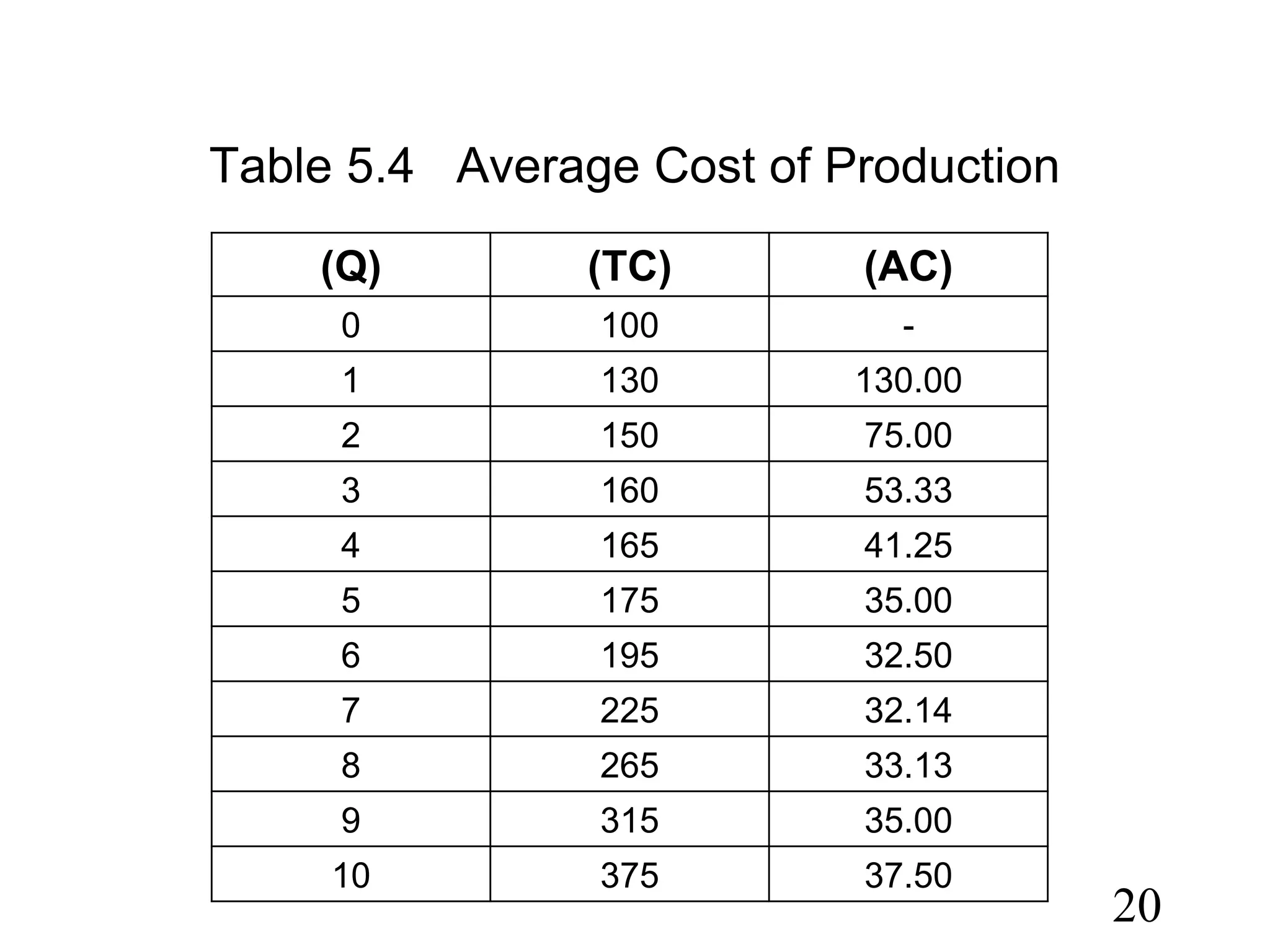

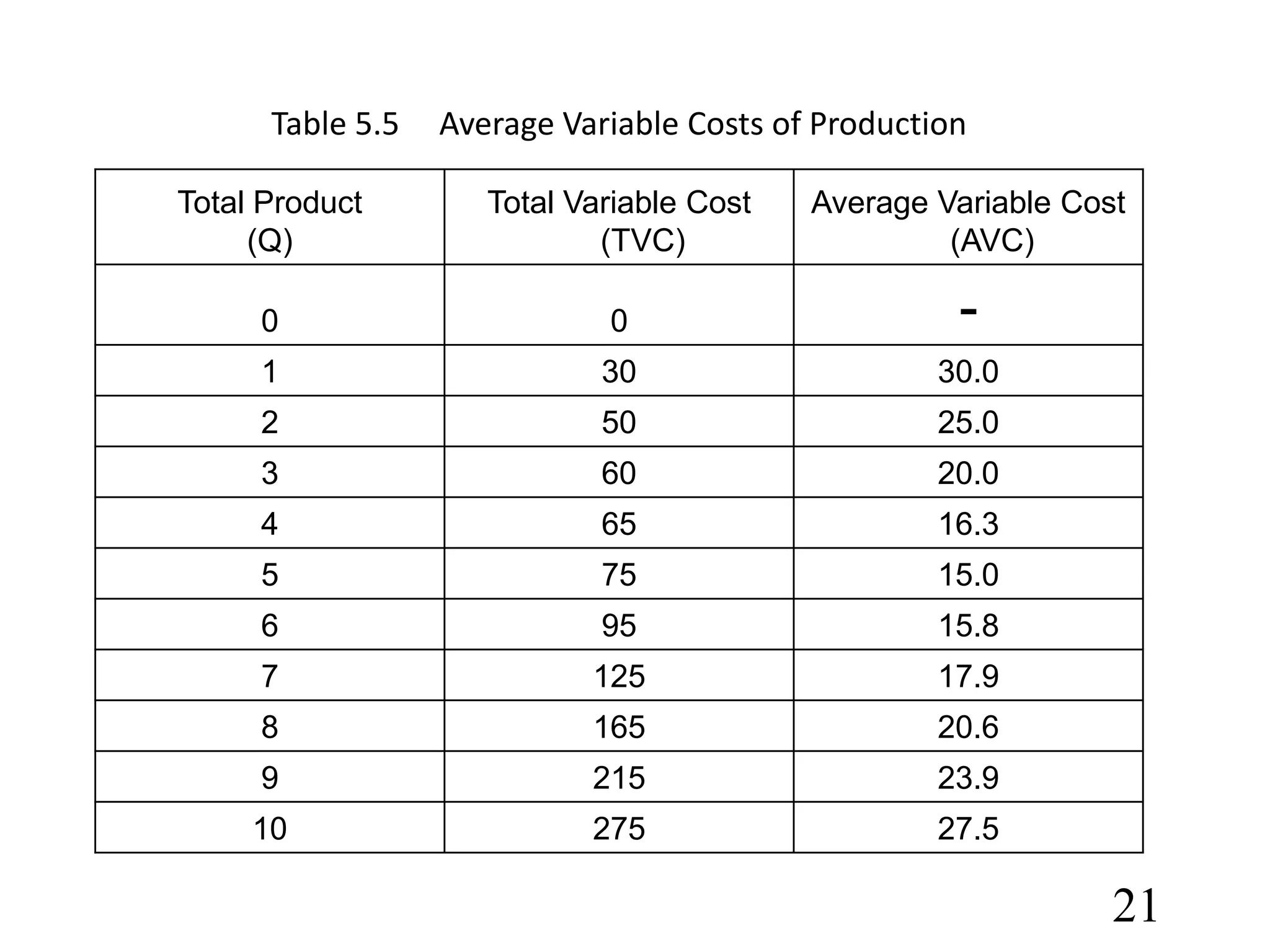

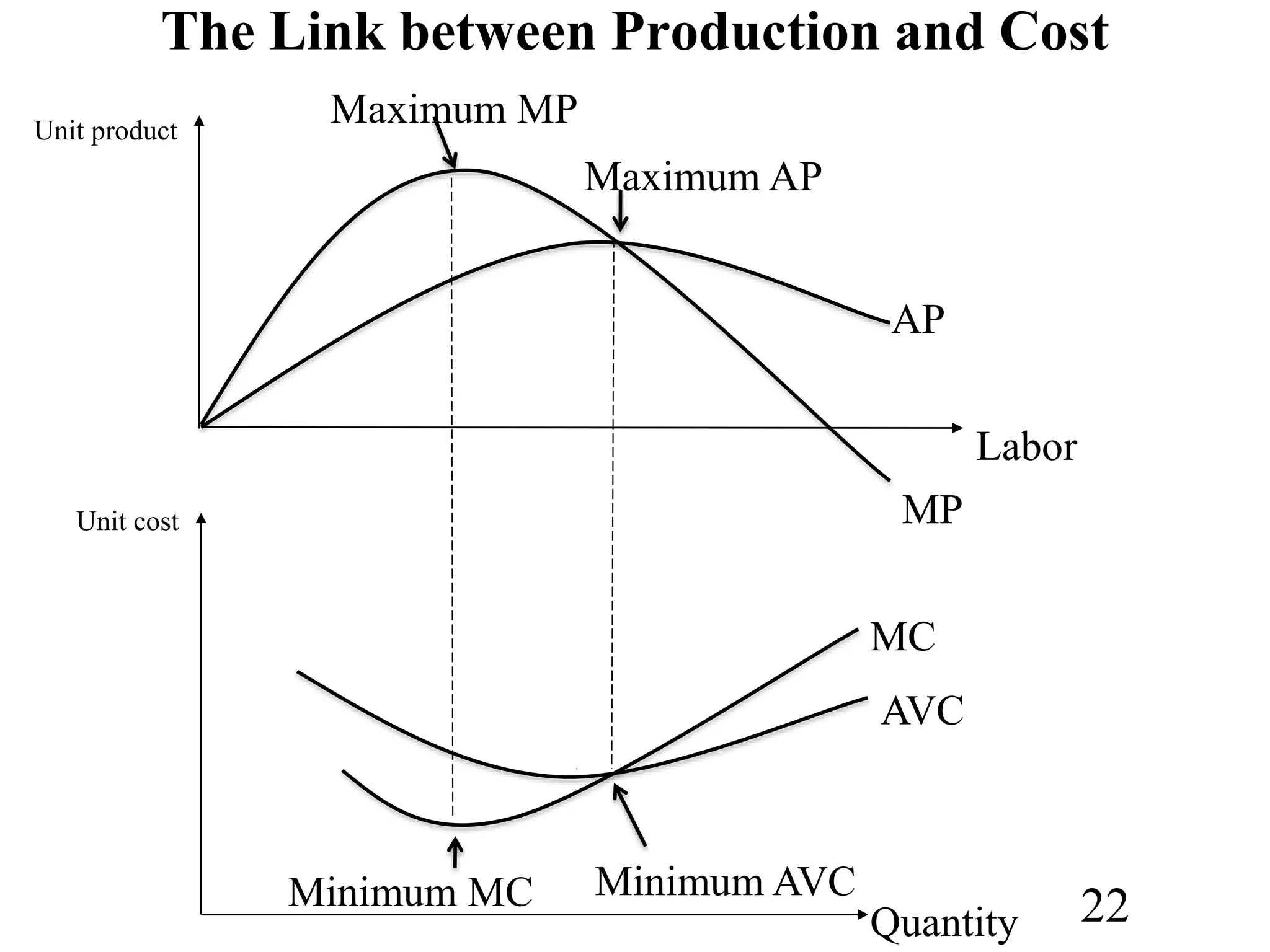

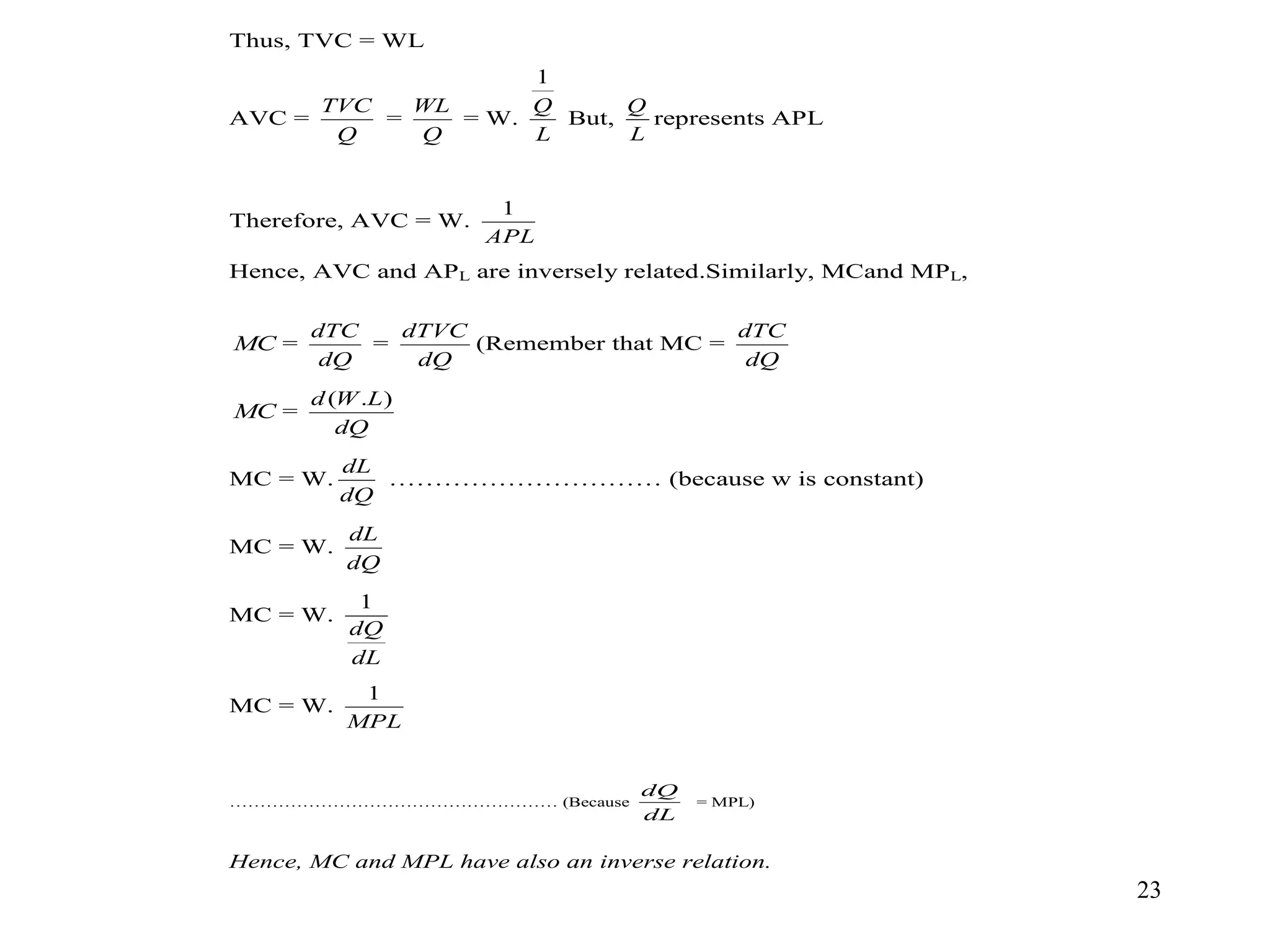

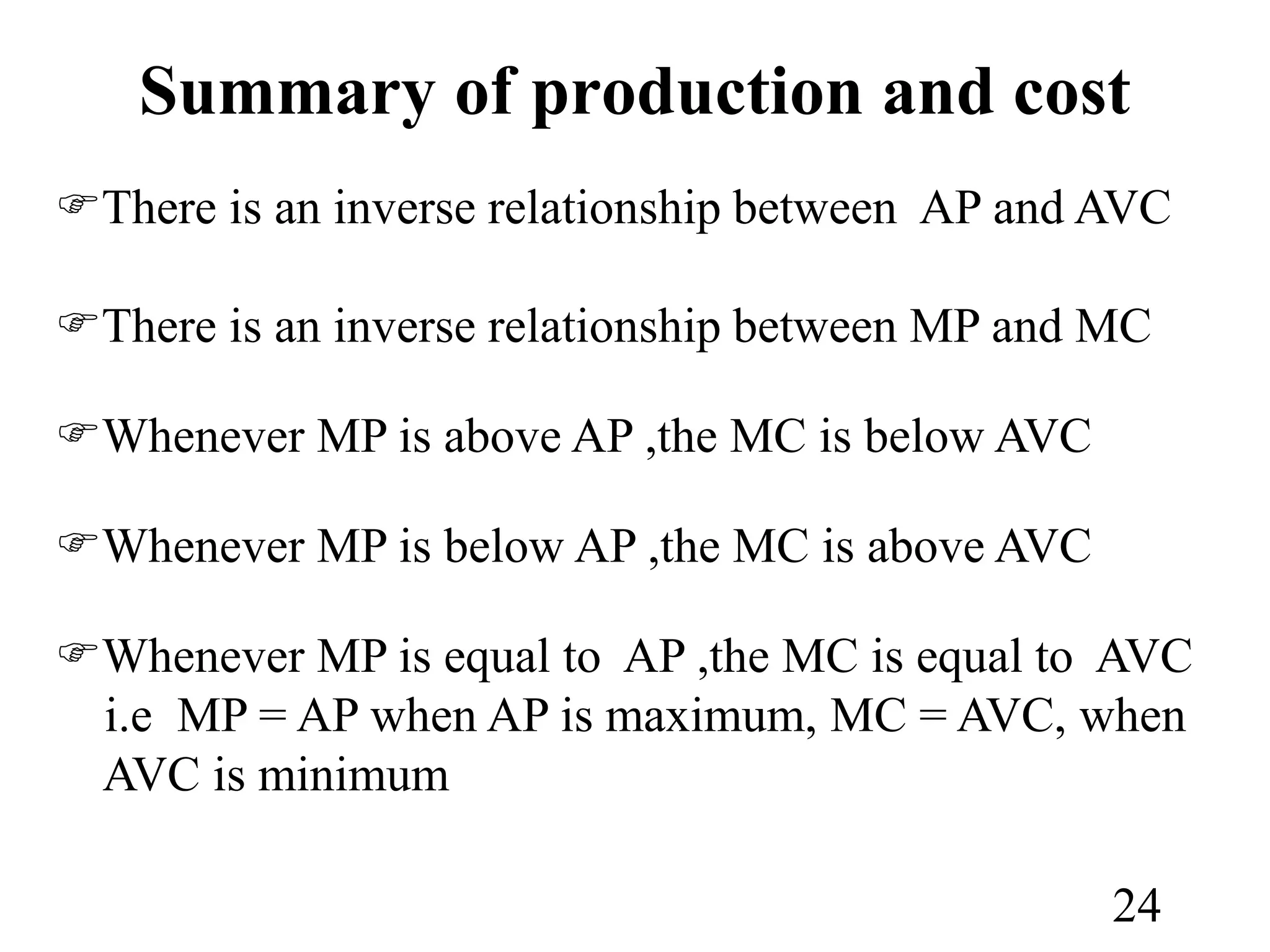

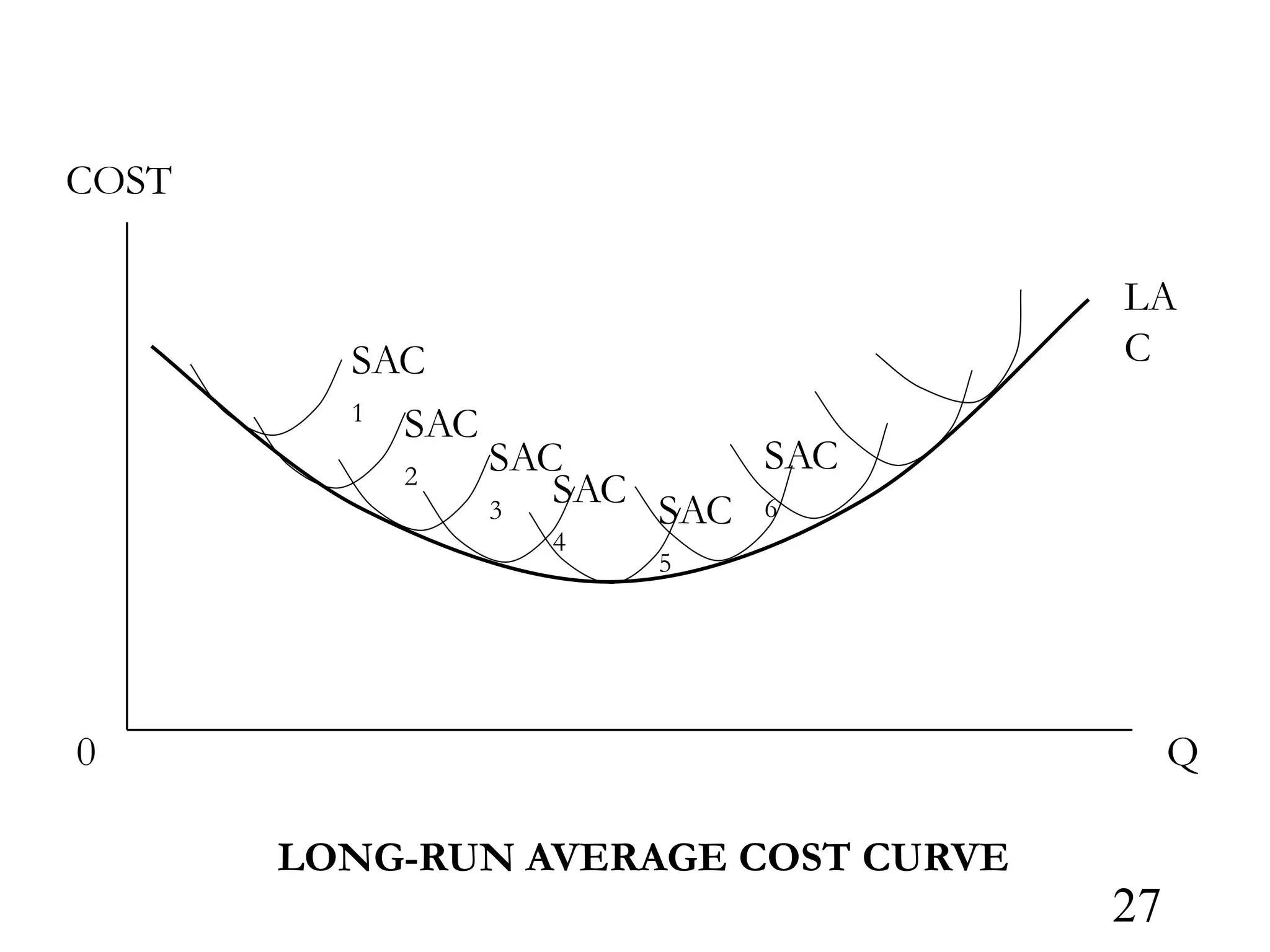

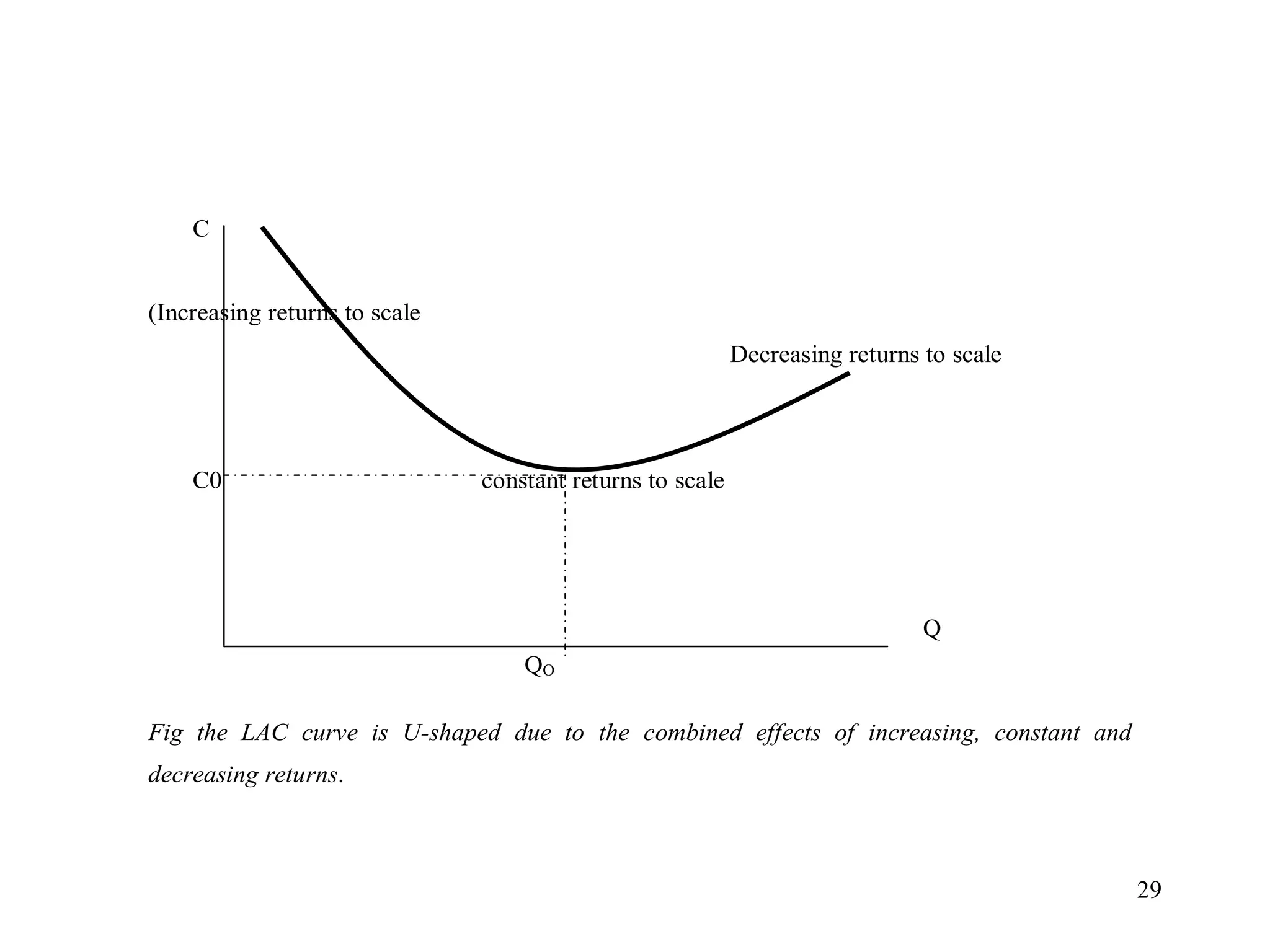

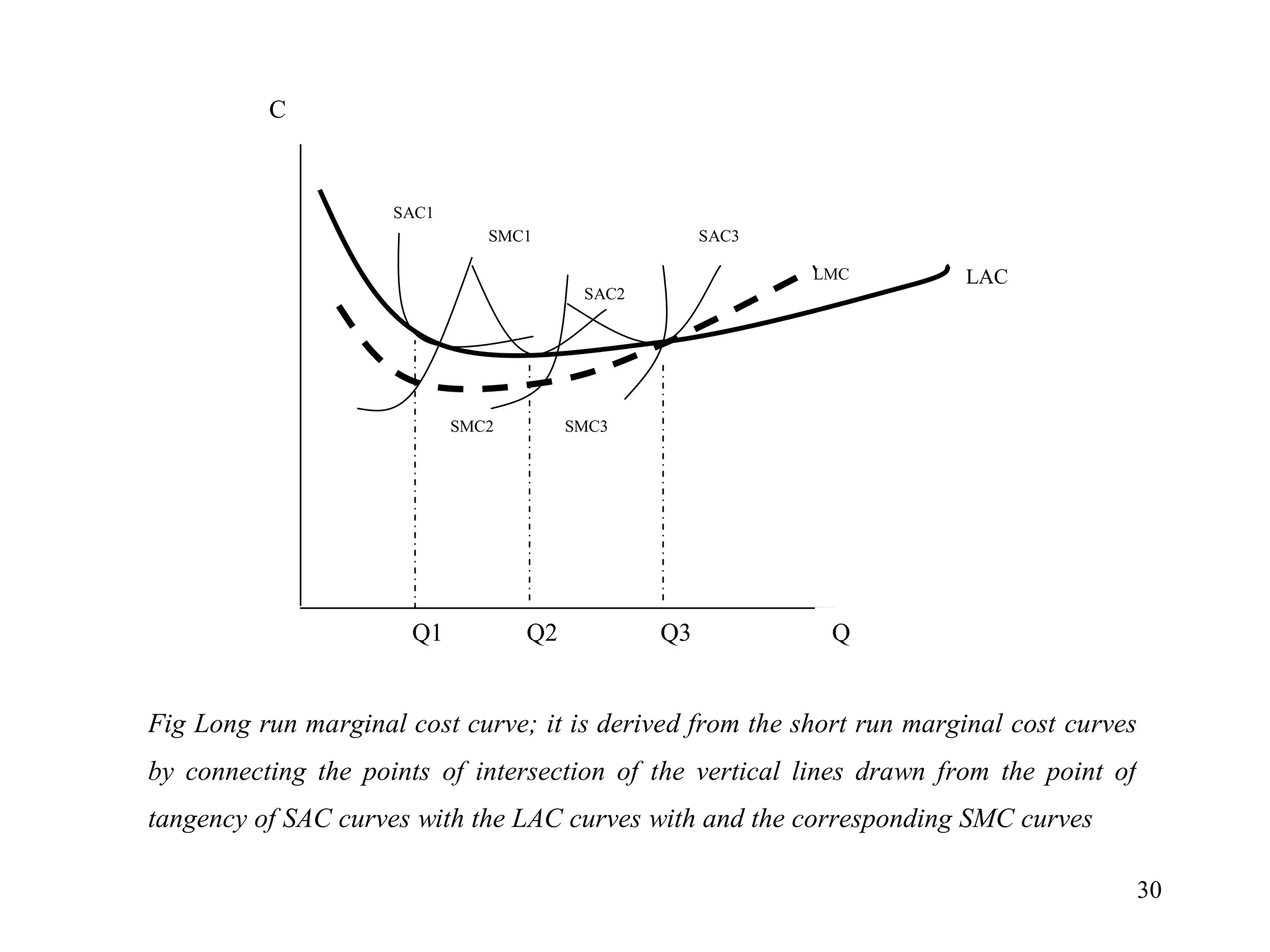

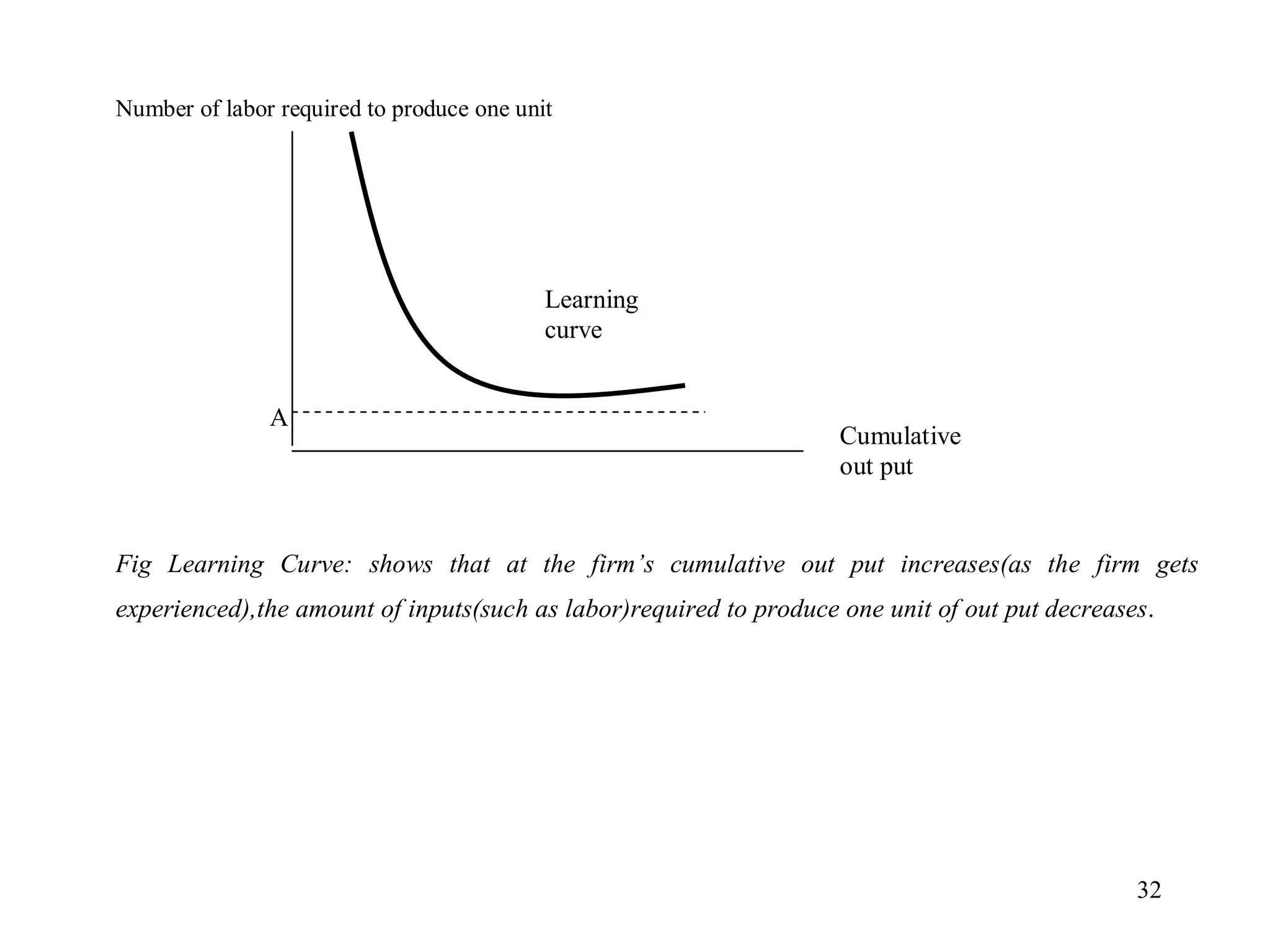

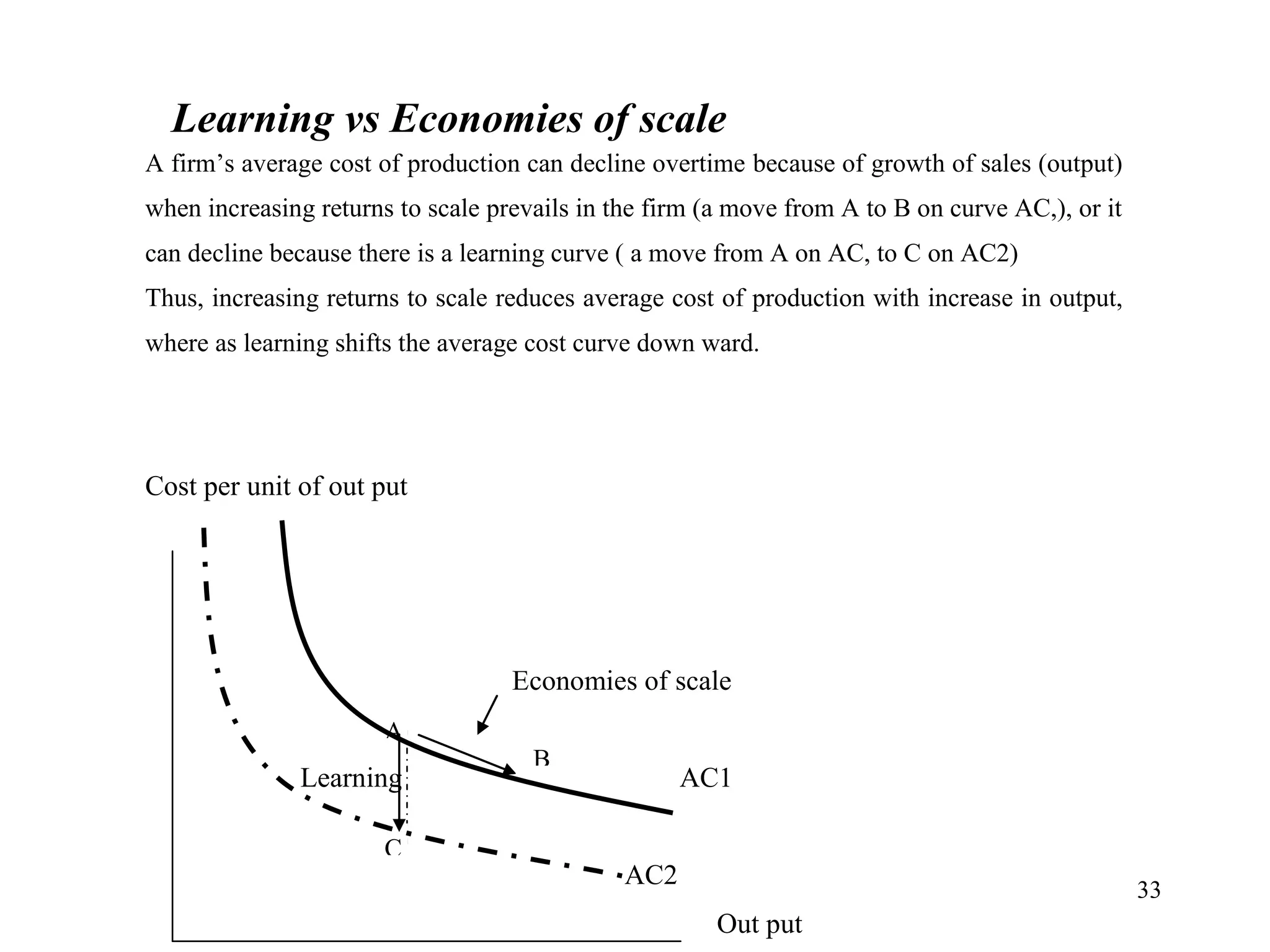

This document discusses various cost concepts in economics. It defines private and social costs, and explains how private costs can be measured using economic and accounting costs. Economic cost includes explicit costs like wages as well as implicit opportunity costs. The document then discusses different types of costs in the short run including total, variable, fixed, average, and marginal costs. It provides examples and graphs to illustrate cost curves and their relationships. Specifically, it explains that AVC, ATC and MC curves are U-shaped due to the law of variable proportions. The document also discusses costs in the long run and how the long run average cost curve is determined by the envelope of short run average cost curves. Finally, it discusses the learning curve concept and how