Downloaded 1,103 times

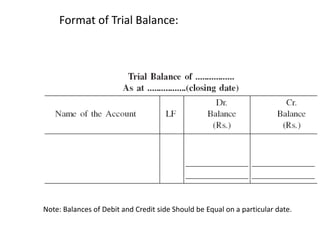

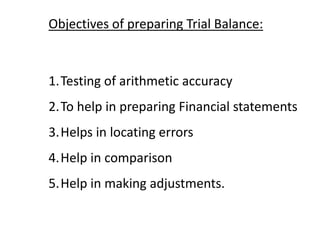

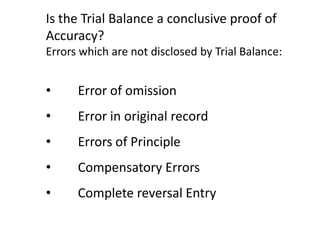

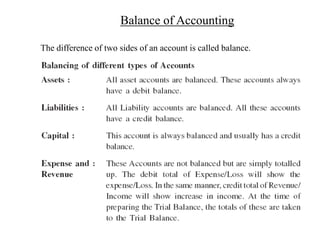

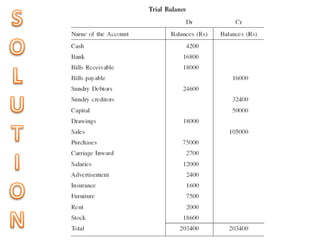

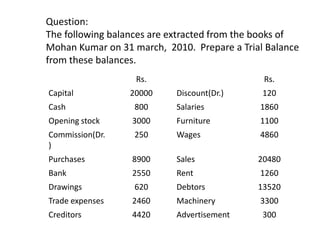

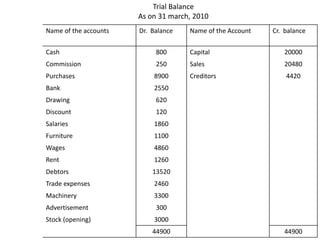

A trial balance is a list of all ledger account balances on a given date arranged in separate debit and credit columns. It is prepared to test arithmetic accuracy, help prepare financial statements, locate errors, allow comparison, and make adjustments. However, a trial balance does not conclusively prove accuracy as some errors like omissions, original errors, errors of principle, or compensating errors may not be disclosed. The example shows a trial balance prepared from account balances extracted from Mohan Kumar's books on March 31, 2010 with equal totals for debit and credit columns.