Downloaded 2,183 times

![PRESENTATION ON GENERAL LEDGER & TRAIL BALANCE Prepared by HASHIBUL HASAN [email_address]](https://image.slidesharecdn.com/accountingpresentationslidefinalforslideshare-100420043853-phpapp01/75/presentation-slide-on-Accounting-General-ledger-trial-balance-1-2048.jpg)

This presentation discusses the general ledger, trial balance, and their purpose and process. The general ledger contains all balance sheet accounts and records transactions through debits and credits. A trial balance is created by summing the balances of each ledger account and comparing total debits to total credits to check for errors. An example transaction is provided to demonstrate preparing ledger accounts and a trial balance.

Presentation on General Ledger by Hashibul Hasan from Daffodil International University.

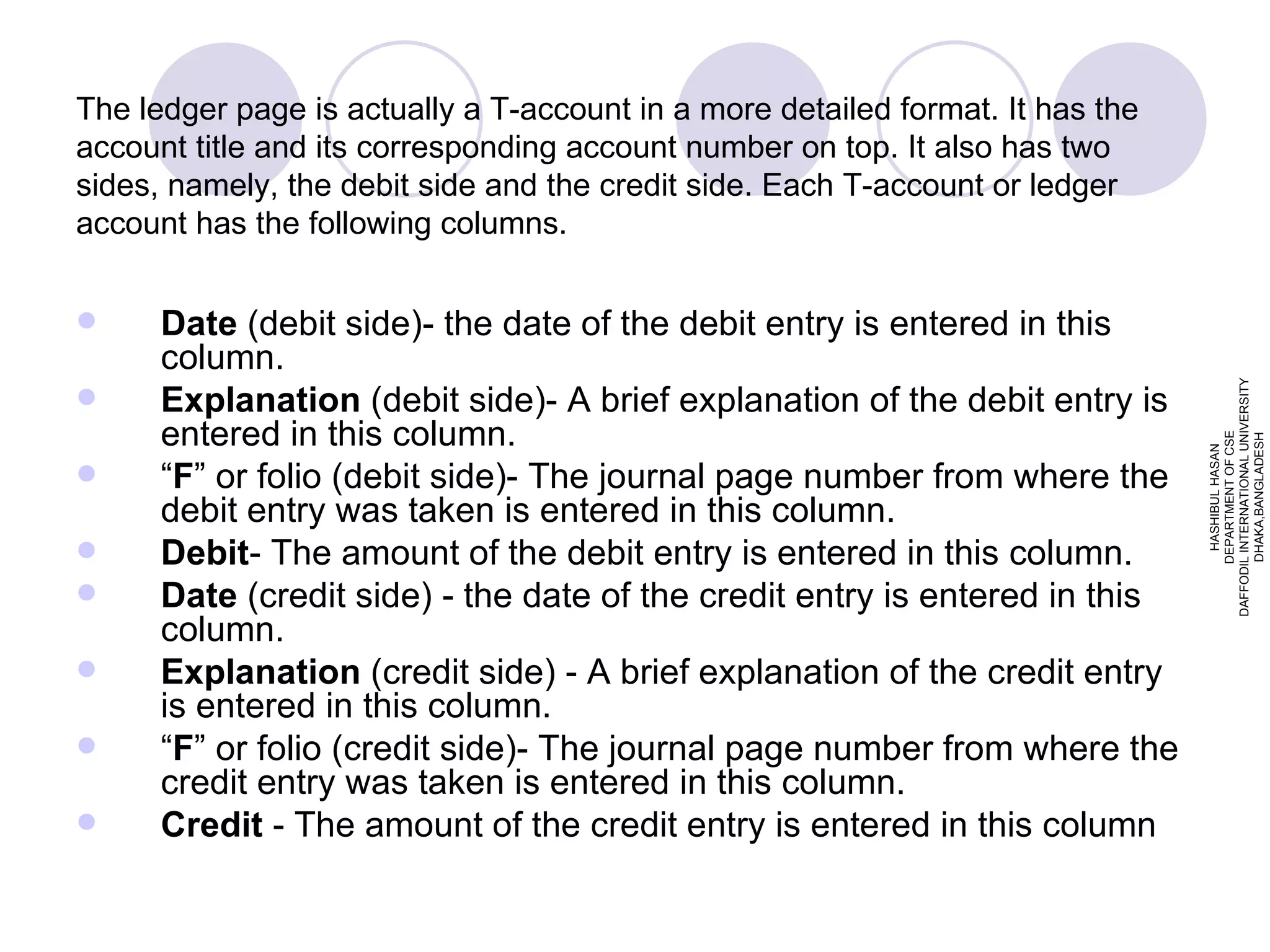

Definition and structure of General Ledger in accounting. Covers T-account format with debits and credits.

Example of ledger entries illustrating balance and transaction details for accounts receivable.

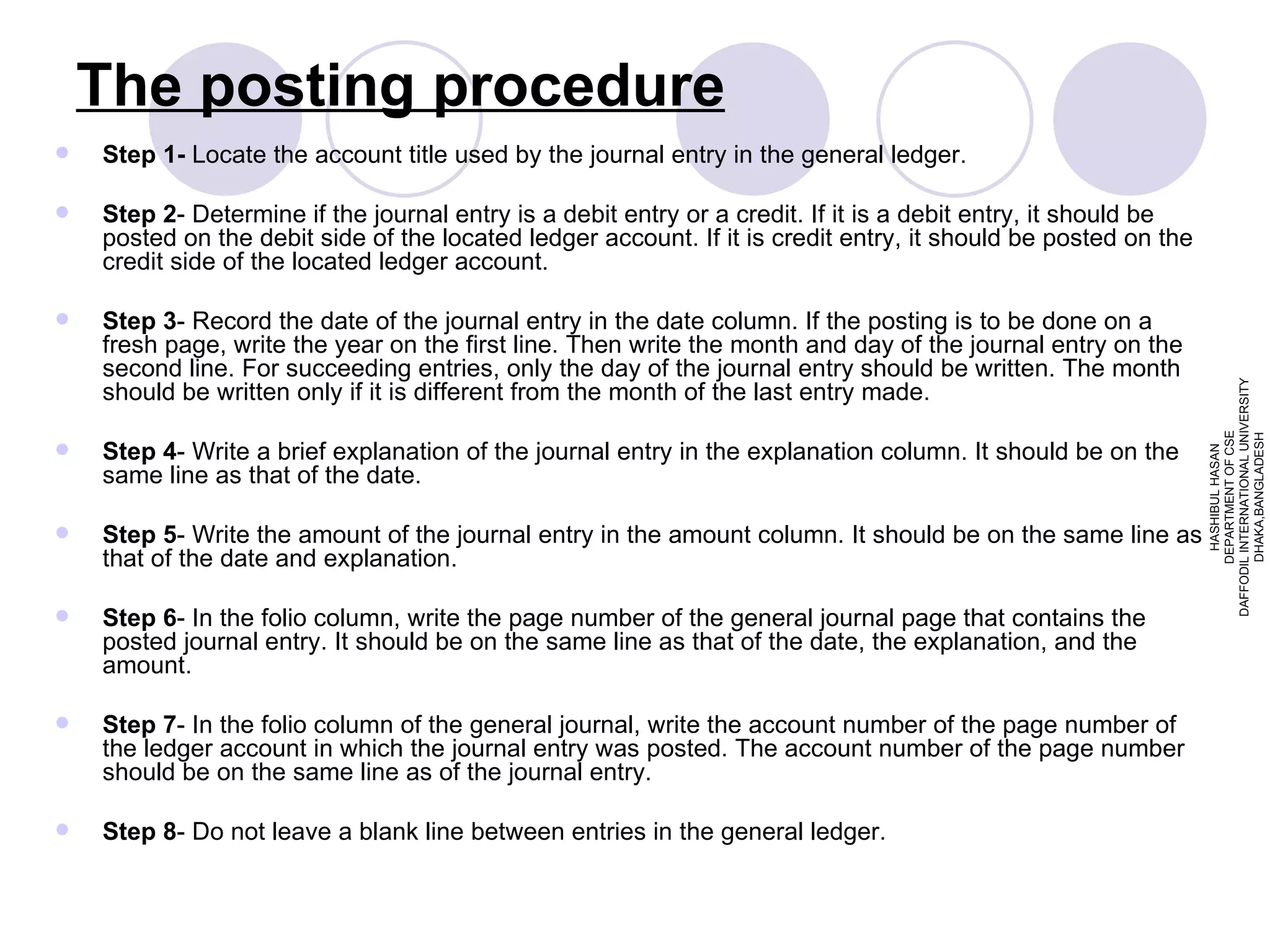

Step-by-step process for posting journal entries to the General Ledger accurately.

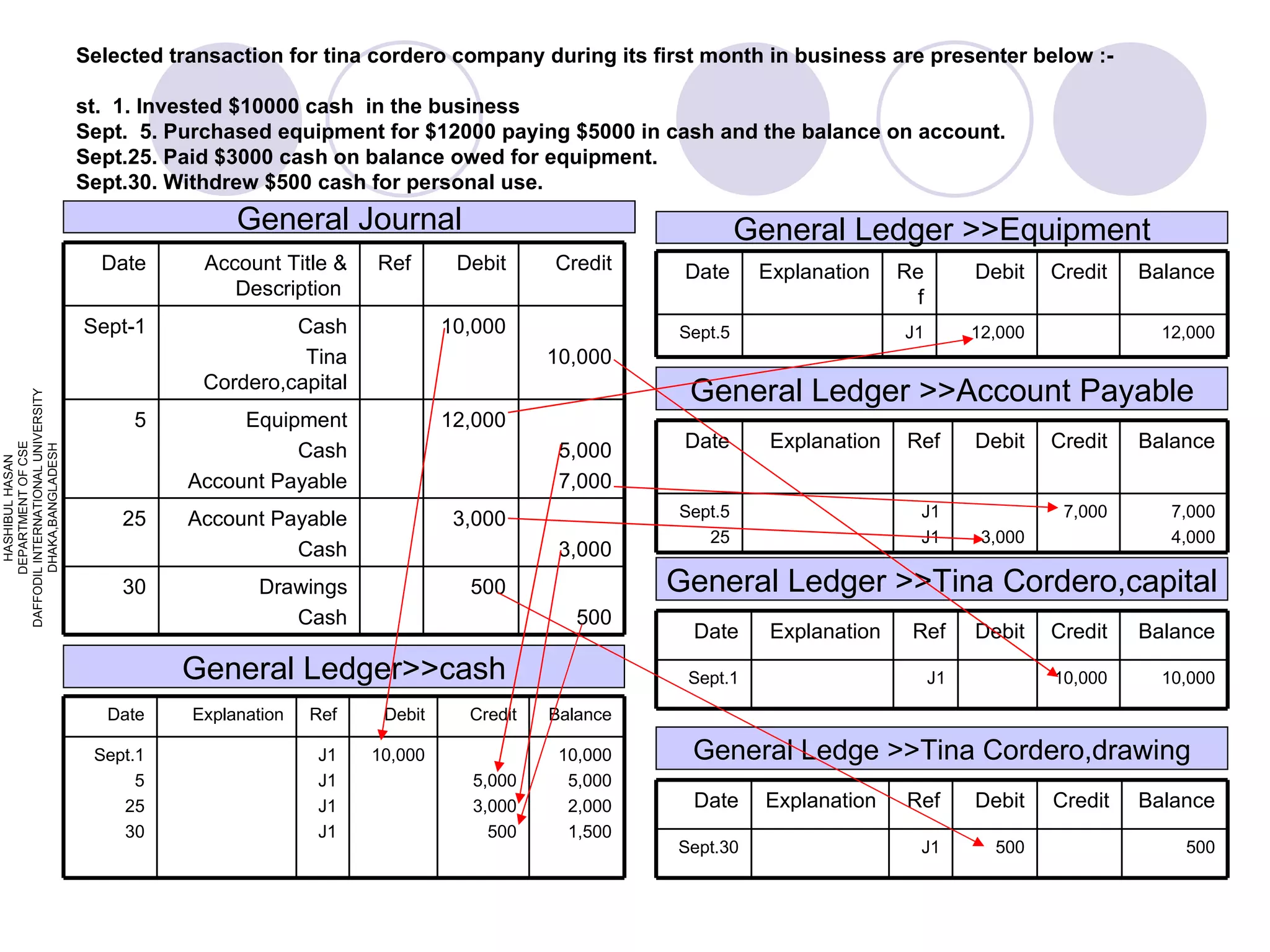

Selected transactions for Tina Cordero Company, detailing investments and cash movements.

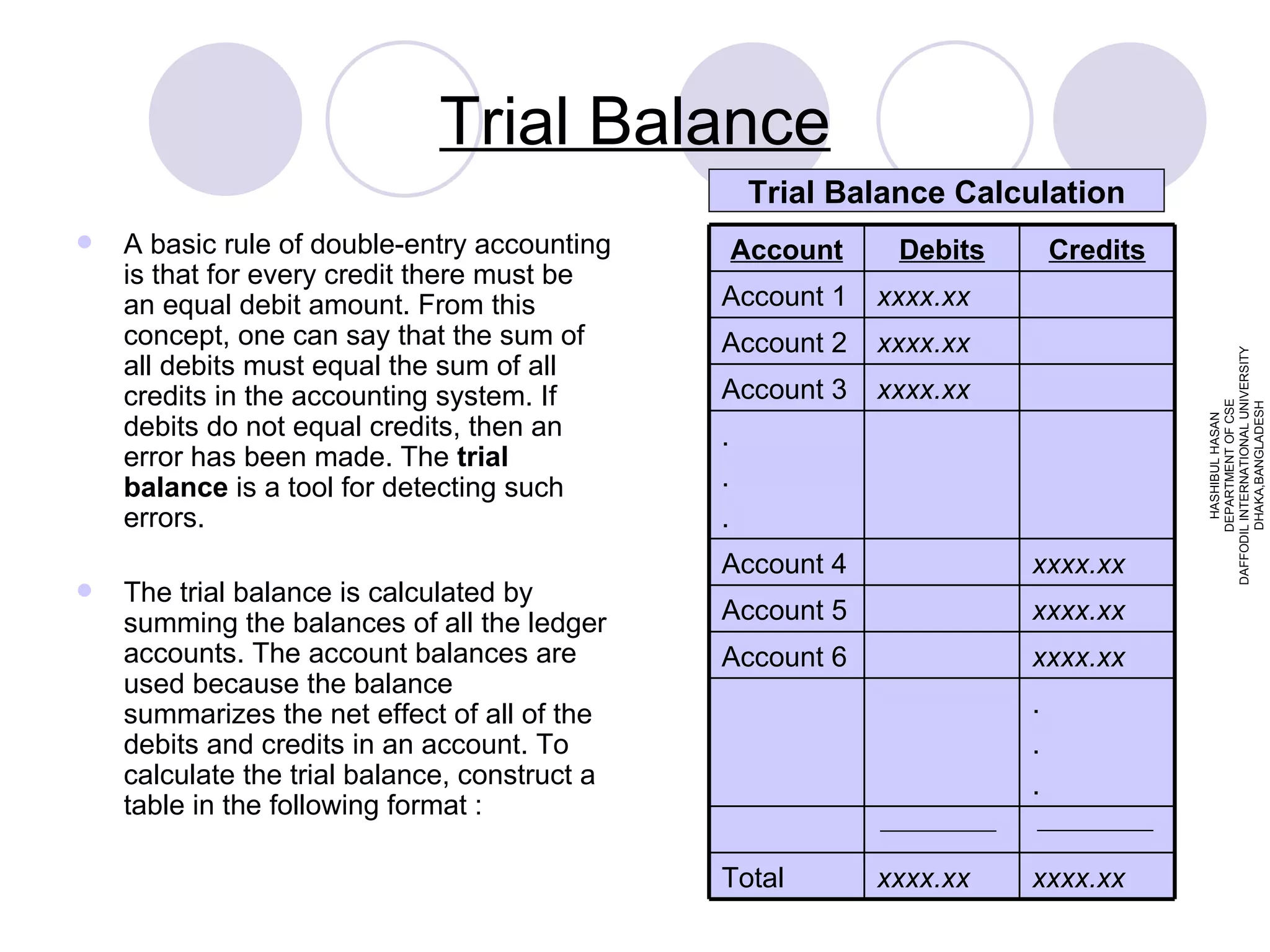

Definition and importance of Trial Balance in accounting to ensure debits equal credits.

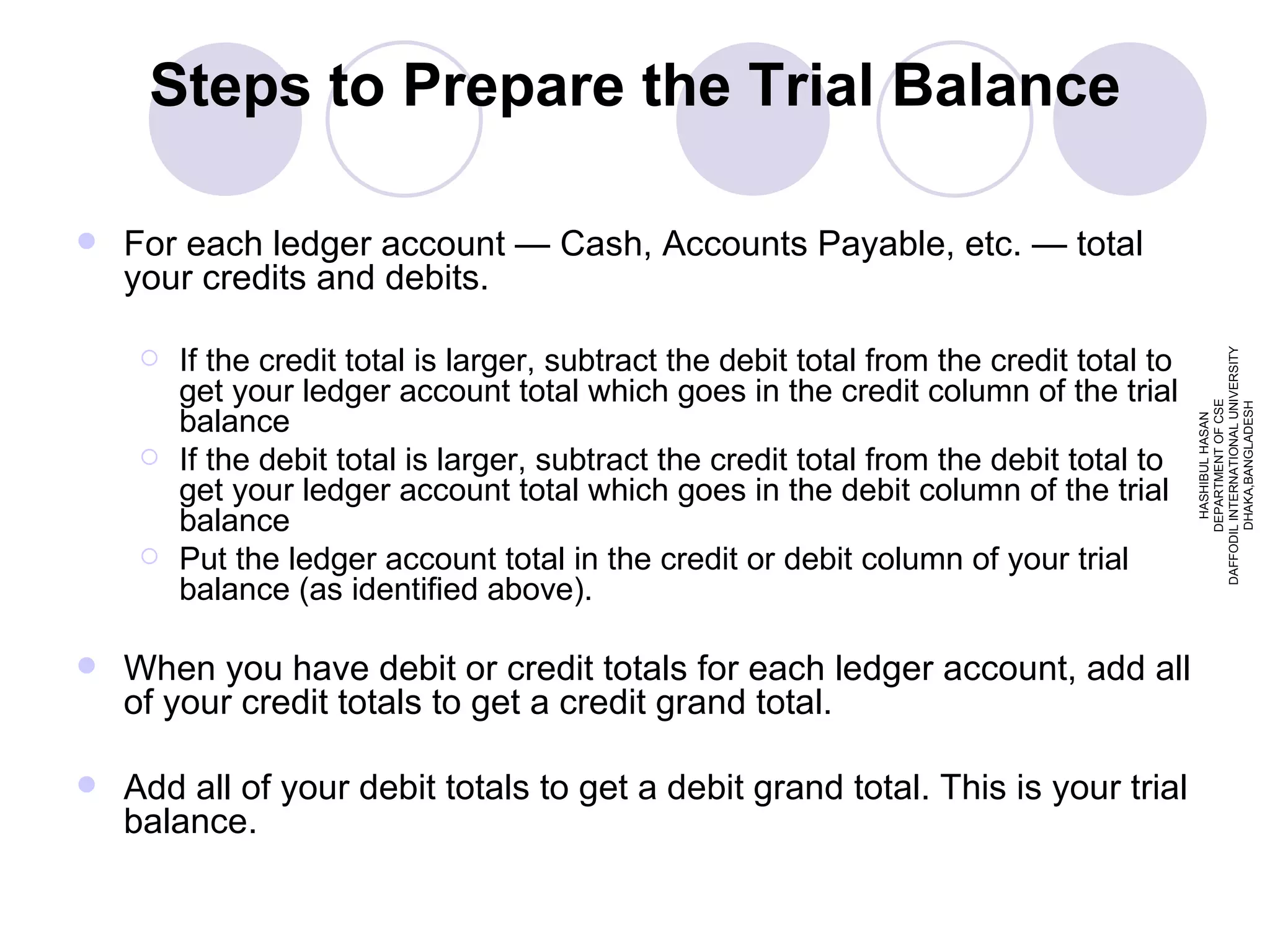

Steps to prepare a Trial Balance, including totaling debits and credits for ledger accounts.

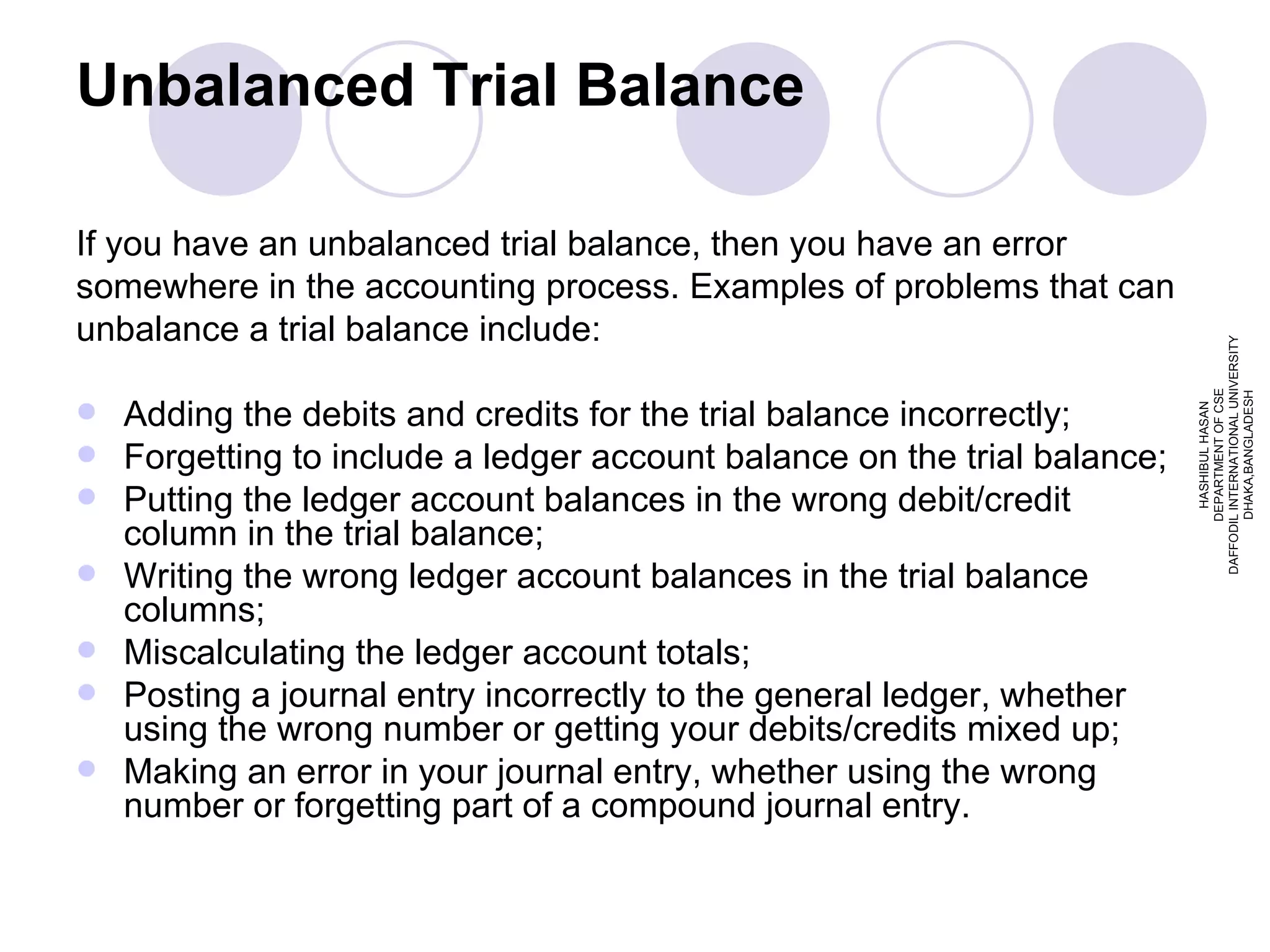

Common issues leading to an unbalanced Trial Balance and examples of errors.

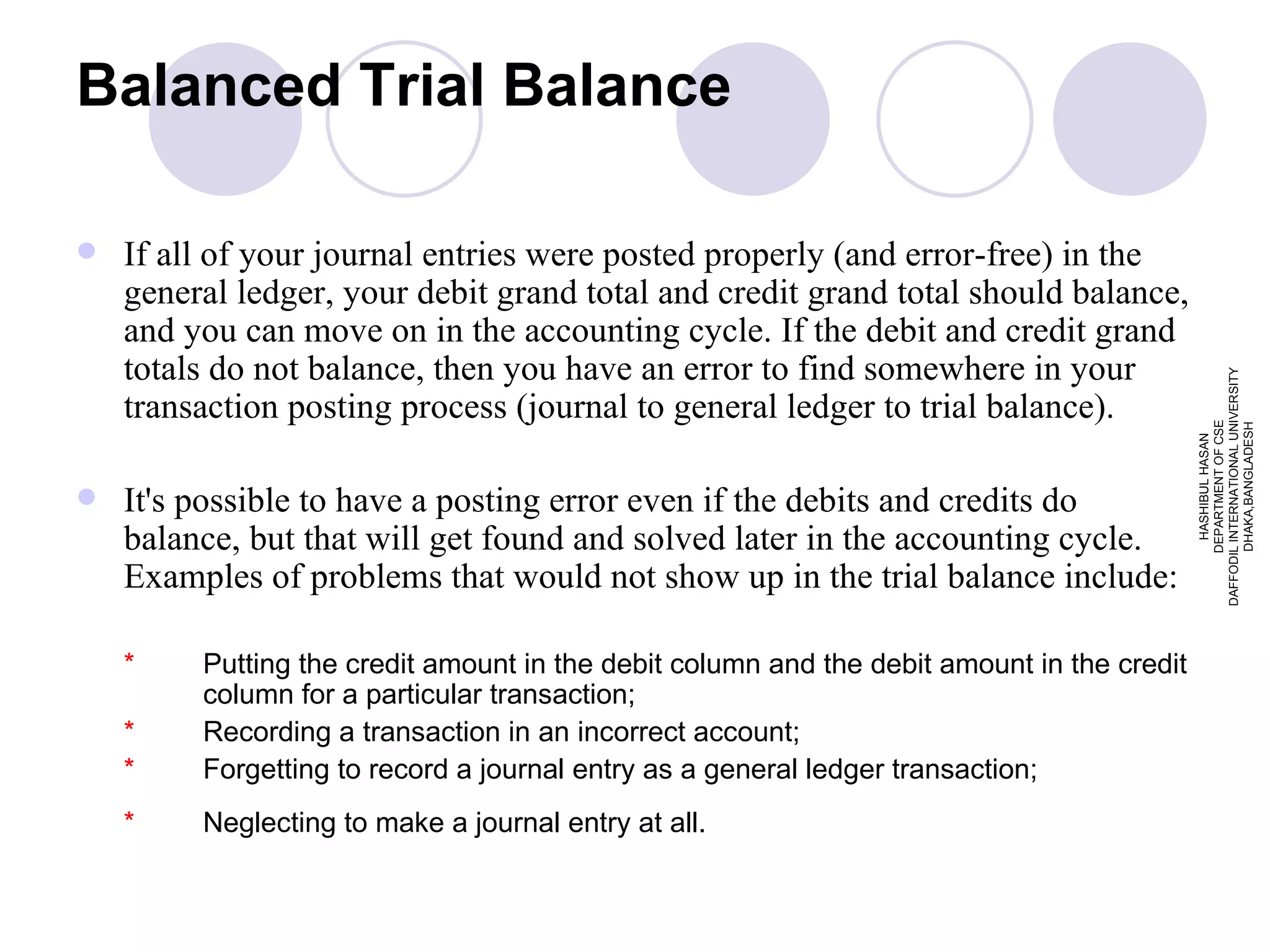

Criteria and significance of a balanced Trial Balance, highlighting potential posting errors.

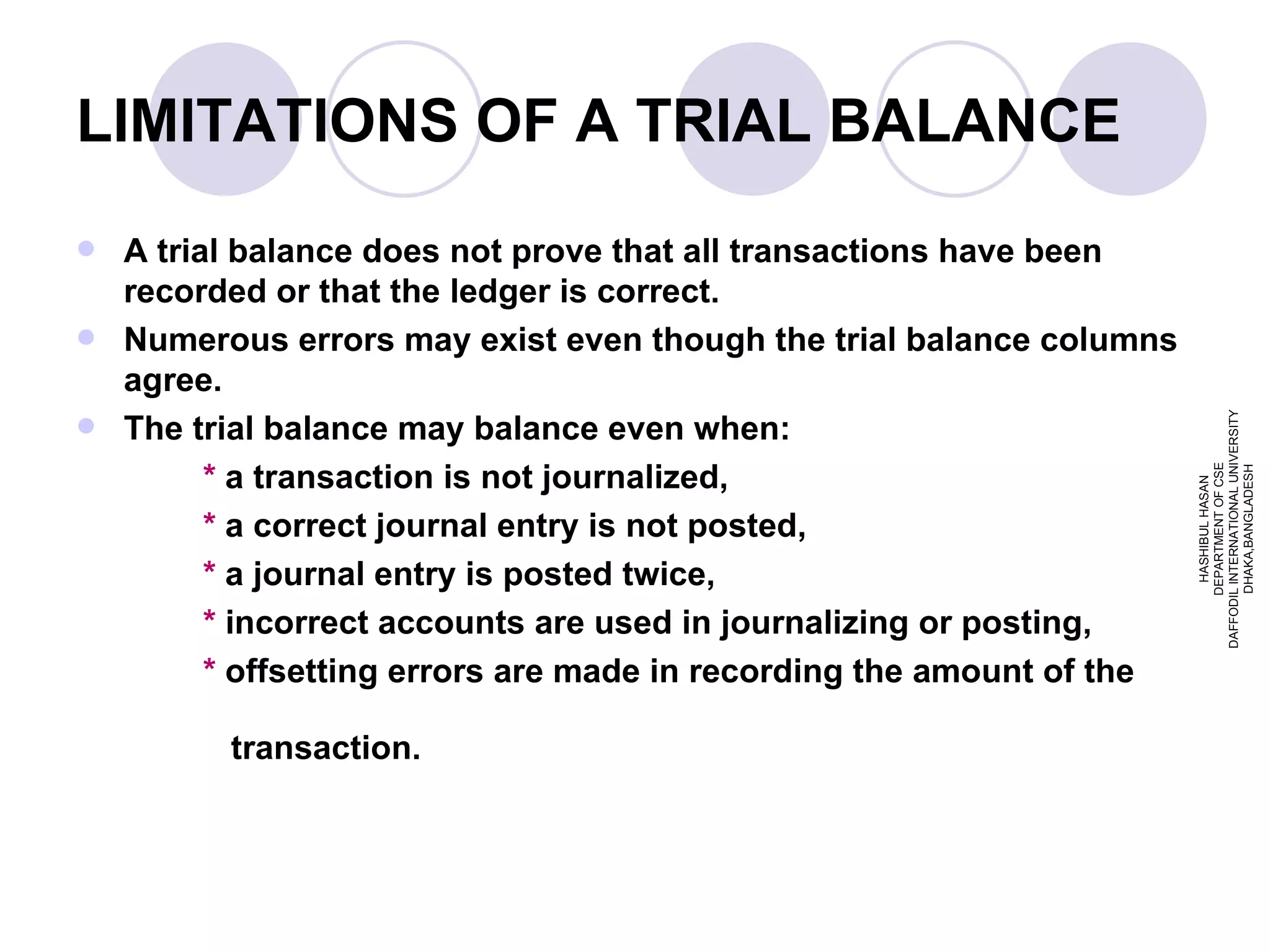

Discusses limitations of Trial Balance, indicating that it does not confirm complete accuracy.

Invitation for questions and concluding remarks by Hashibul Hasan.