Download as PDF, PPTX

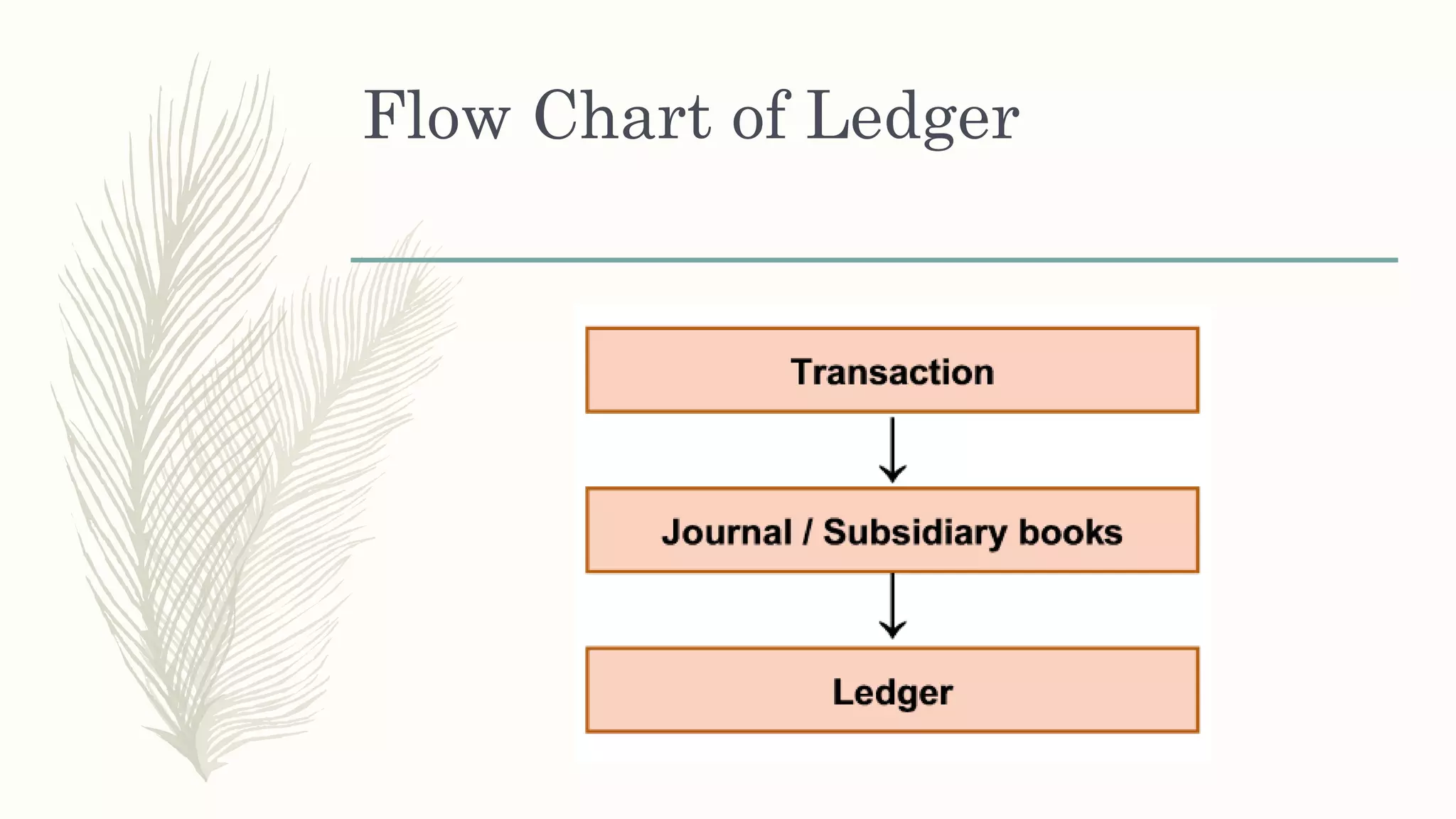

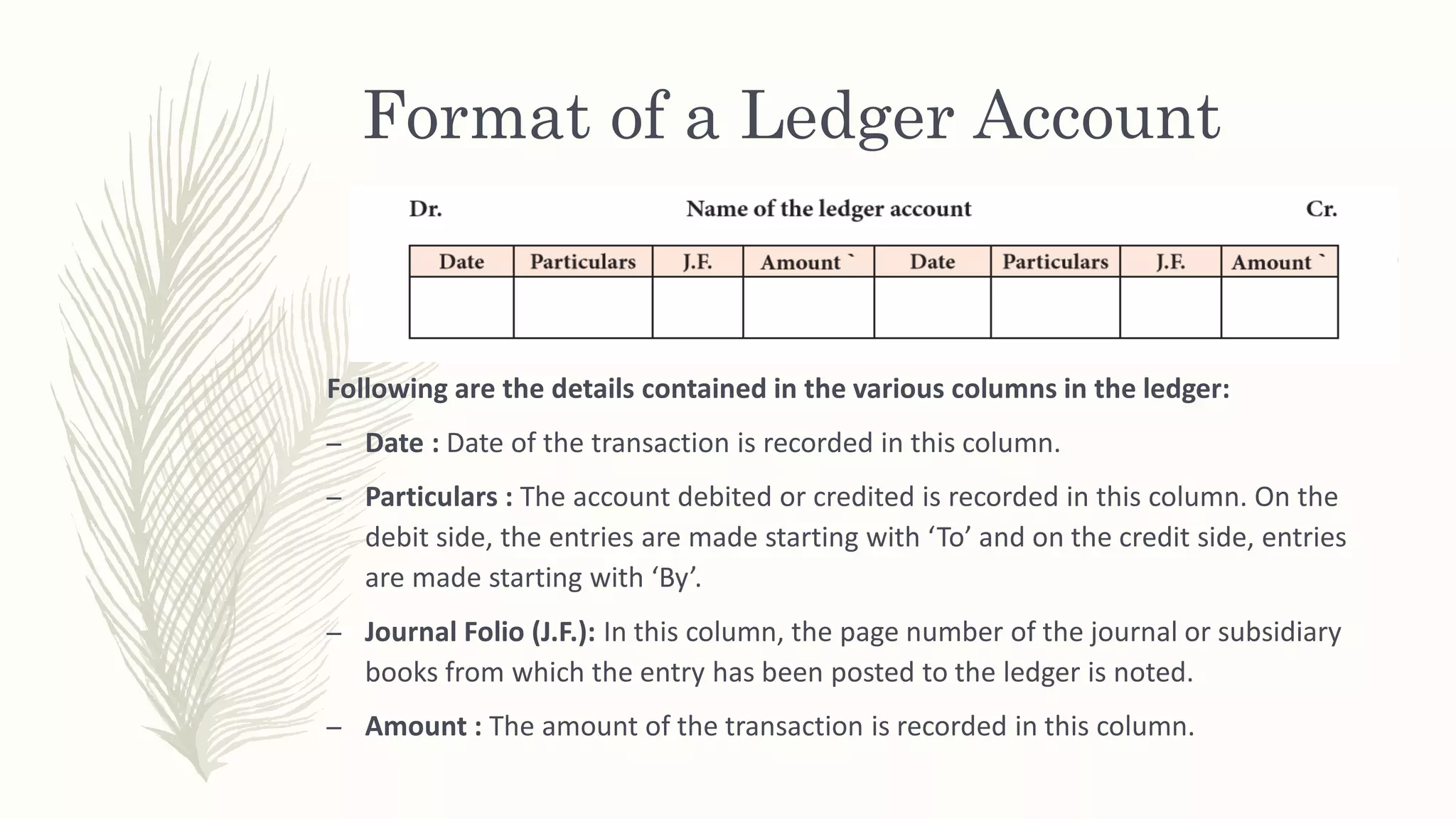

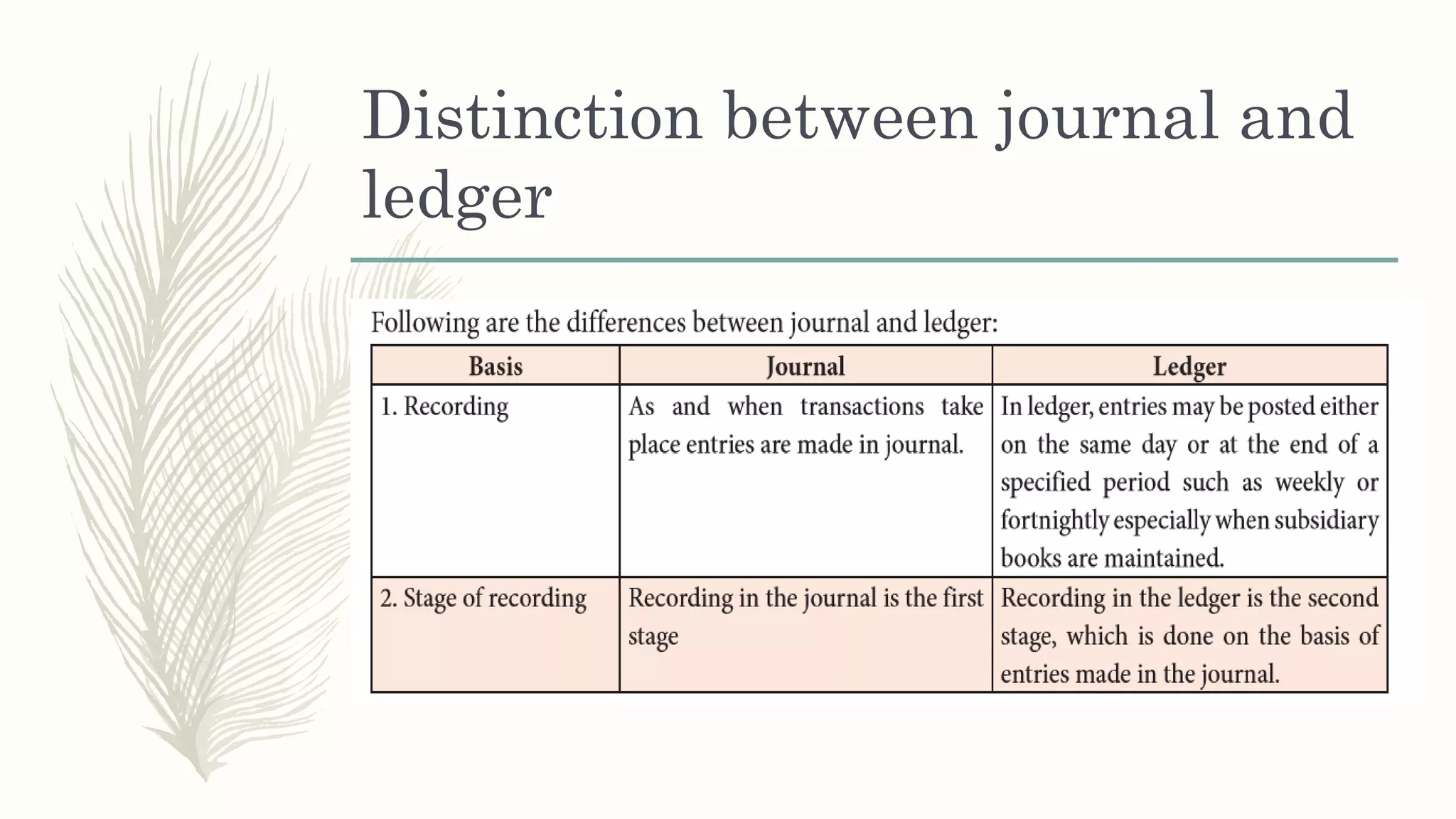

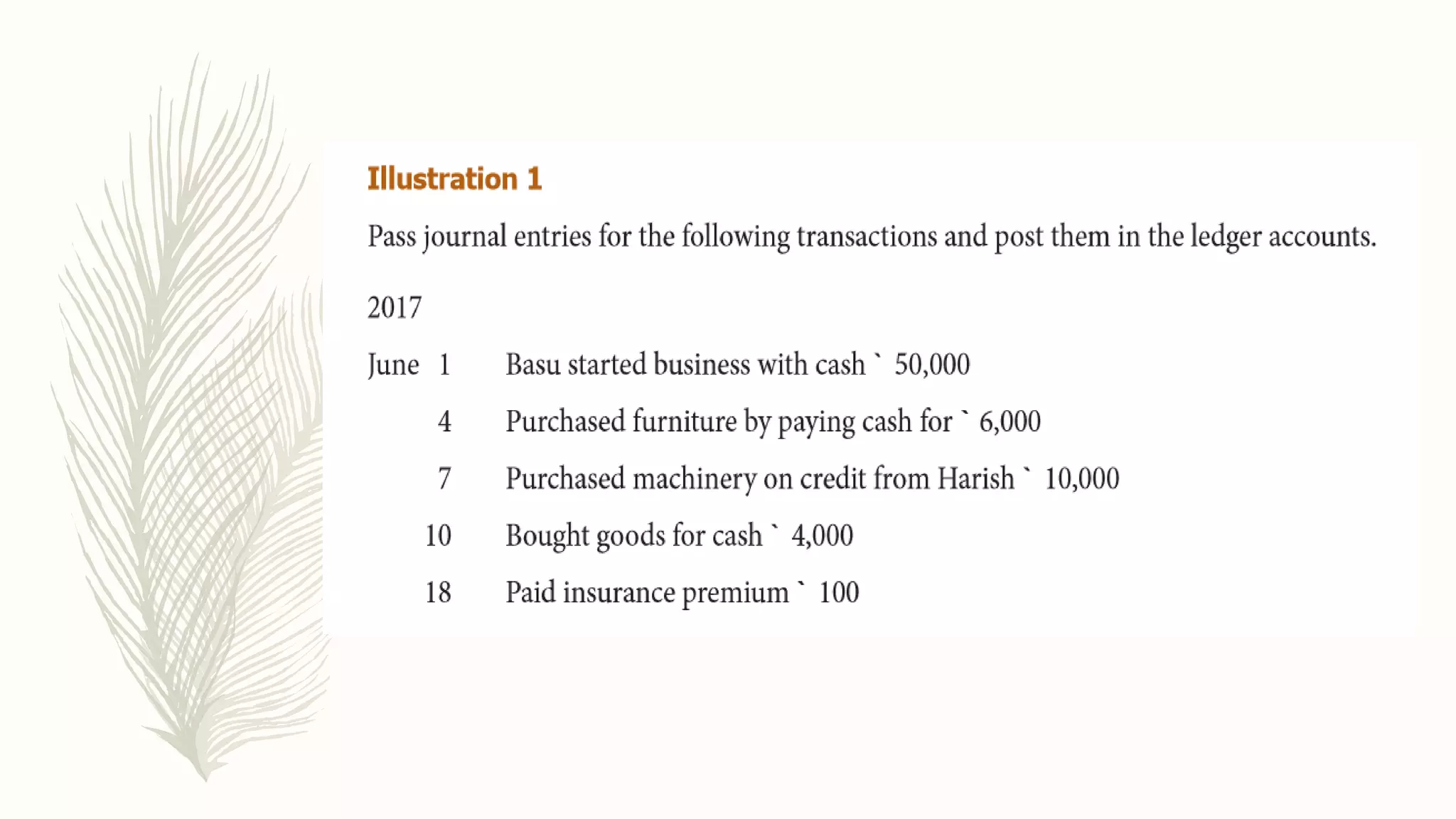

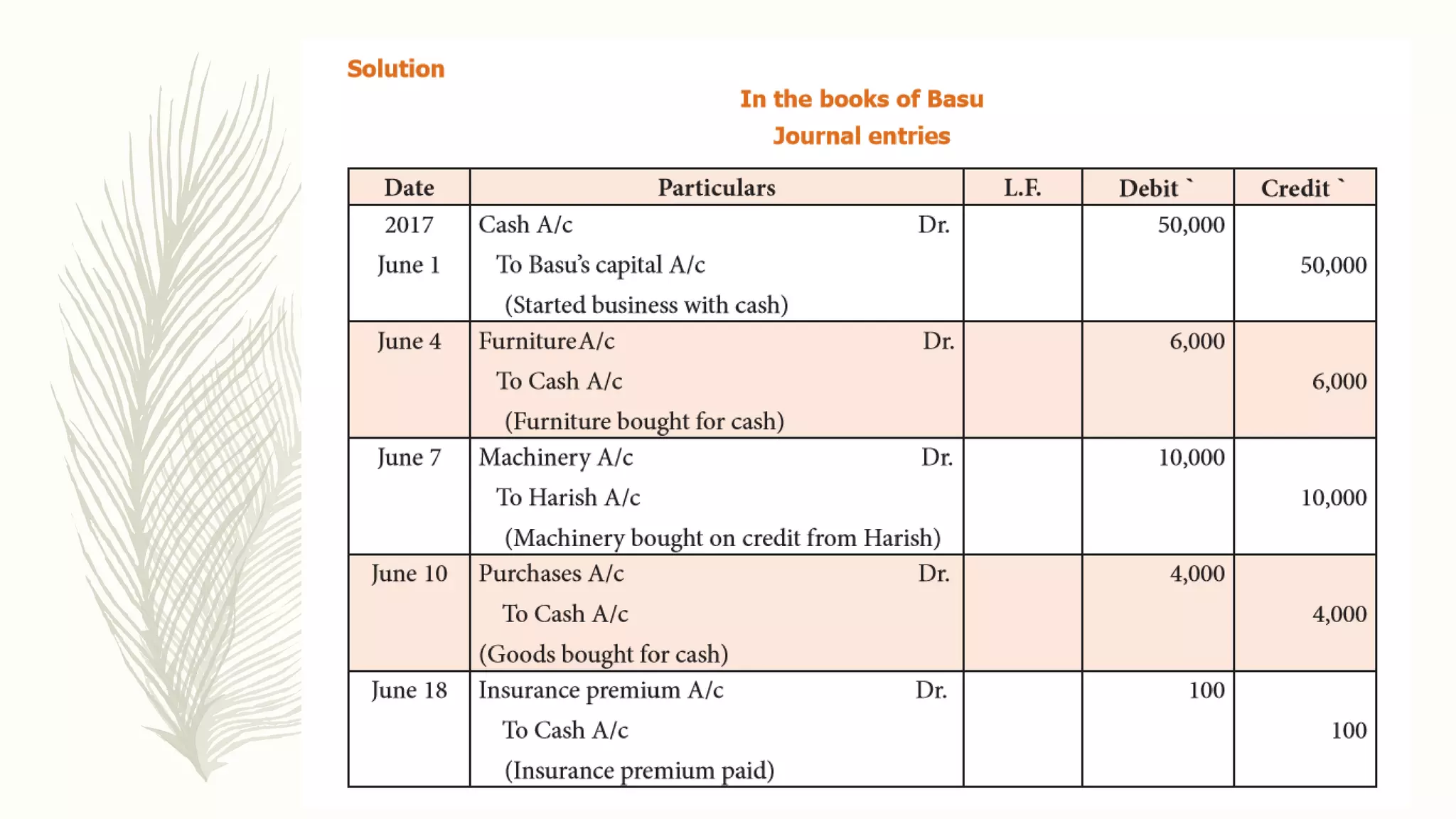

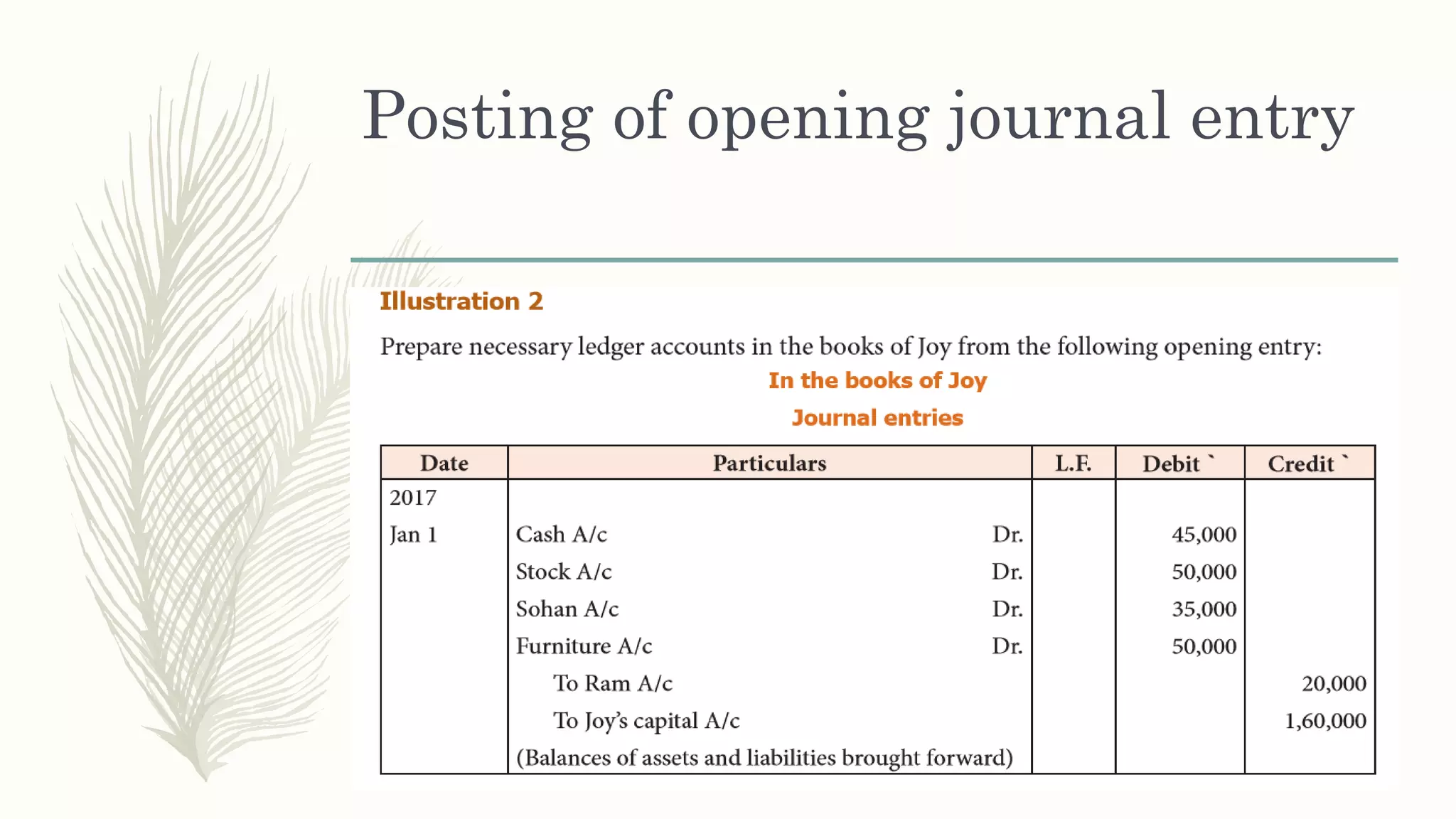

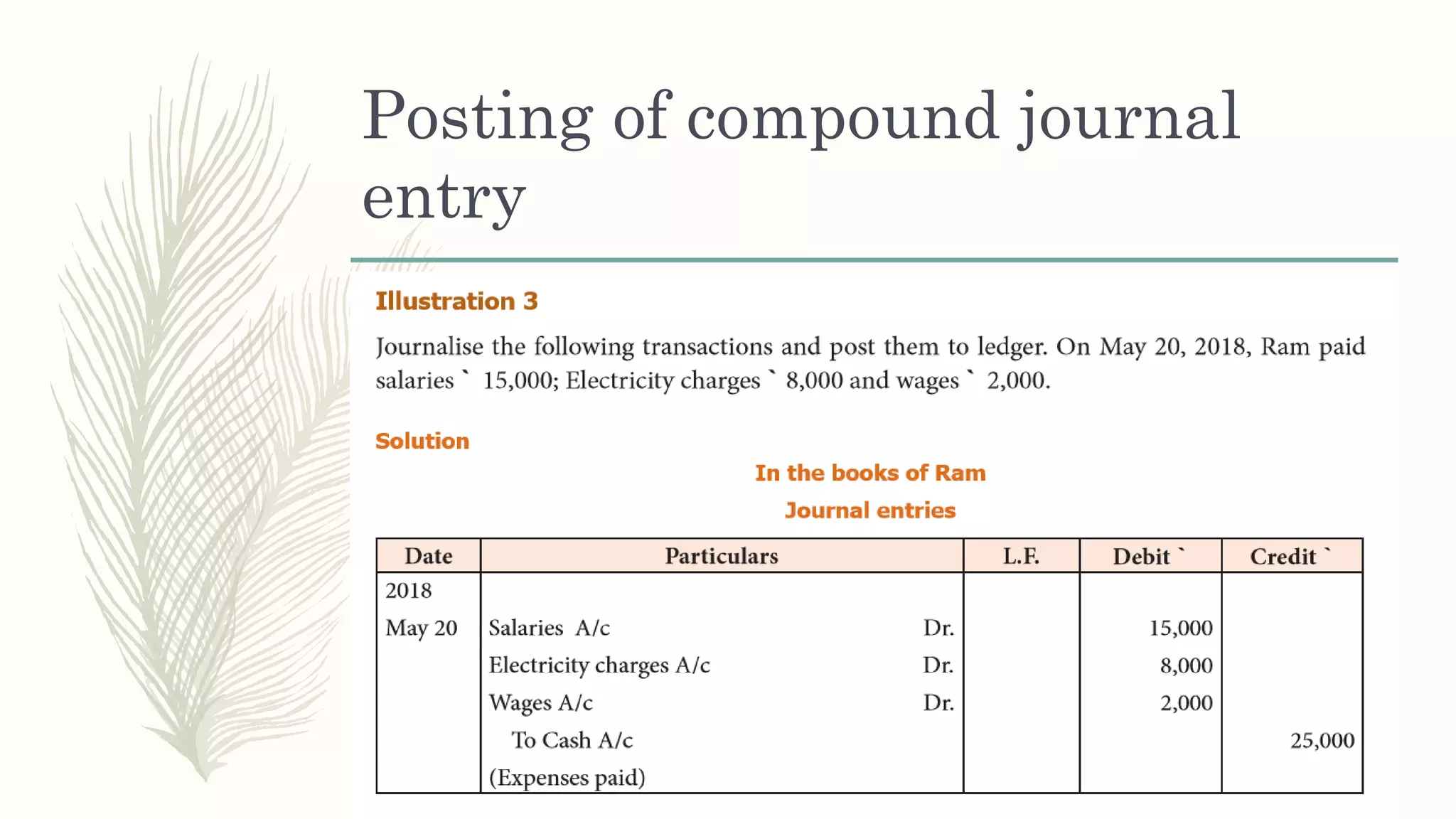

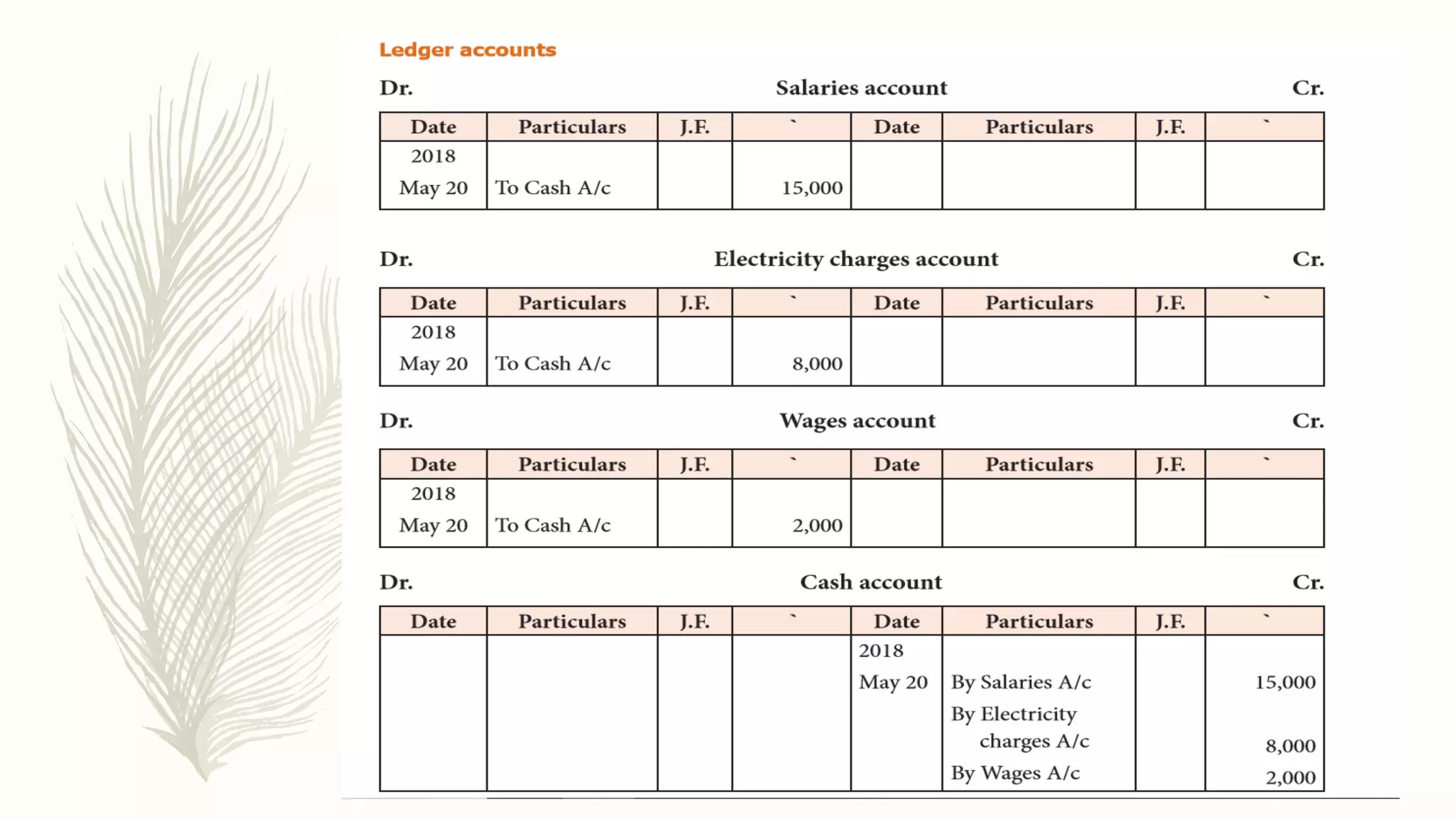

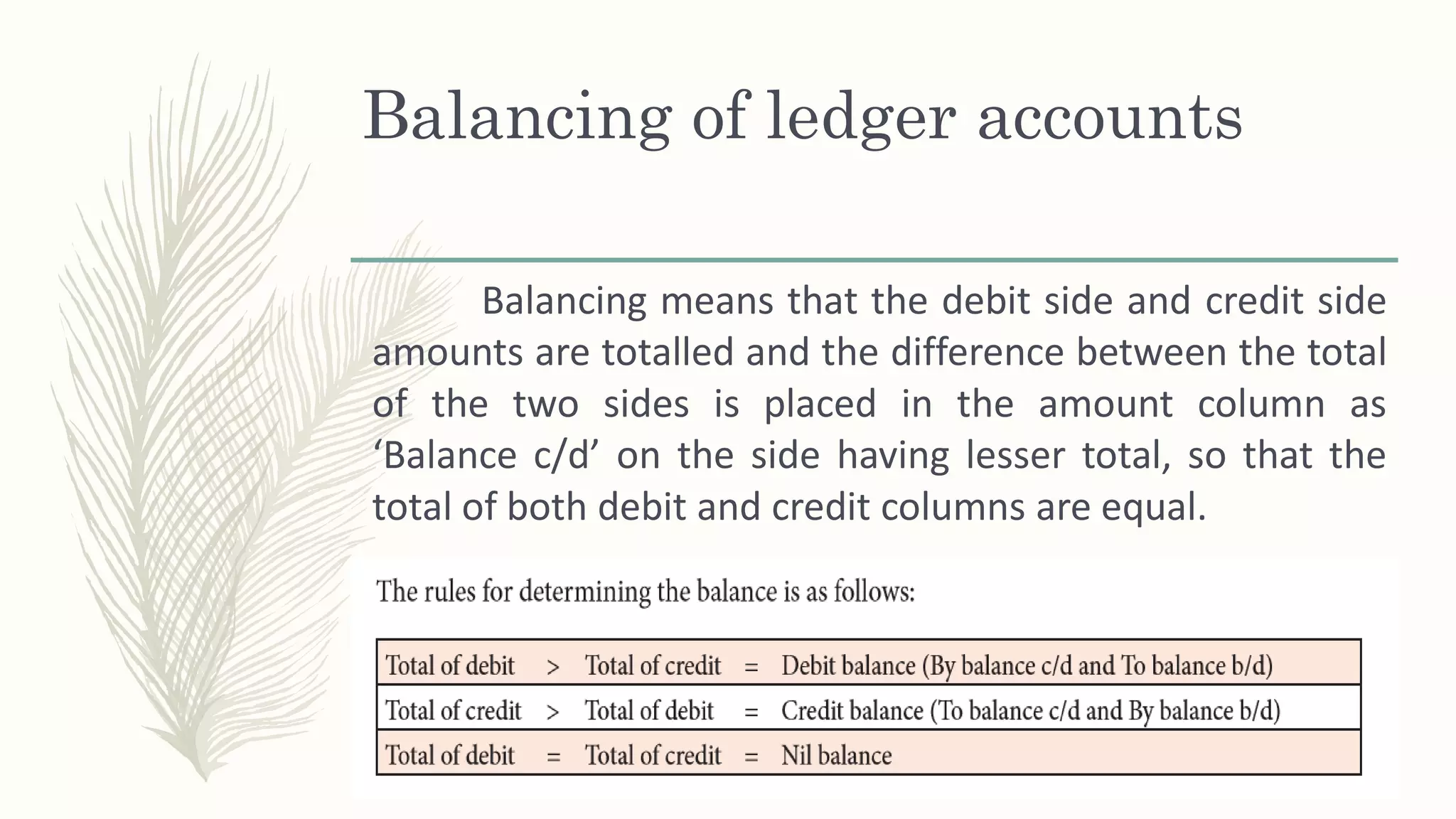

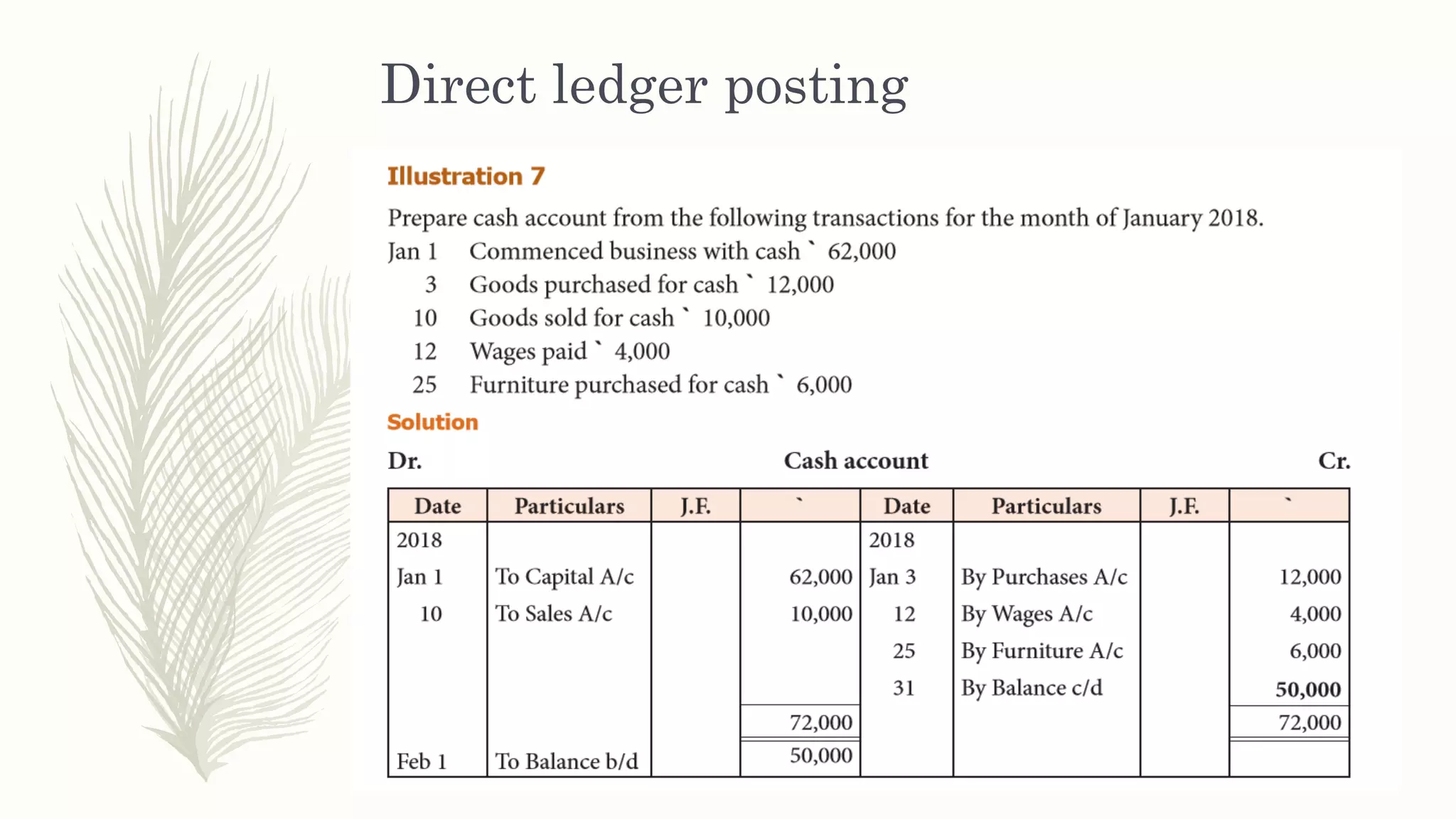

This document defines key concepts related to ledgers. It begins with defining a ledger as a summary of all transactions relating to an account over a period of time, showing the net effect. It then provides a flow chart and discusses the utilities of ledgers, including providing quick information on accounts, controlling transactions, preparing trial balances and financial statements. The document also covers the format of ledger accounts, the distinction between journals and ledgers, and the procedures for posting transactions to ledgers, including opening entries, compound entries, and balancing accounts.