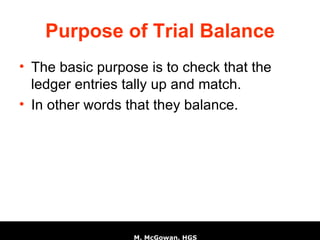

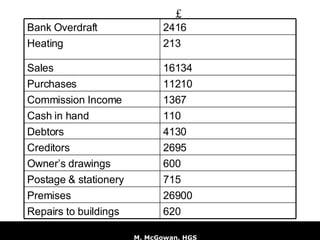

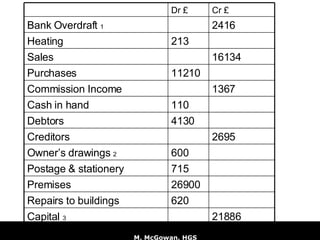

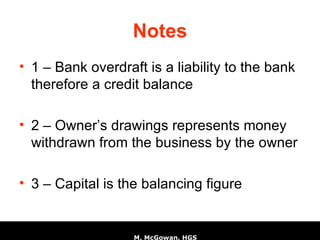

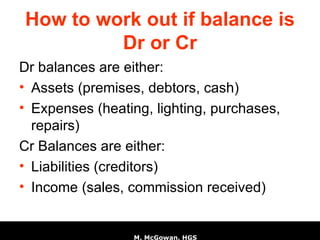

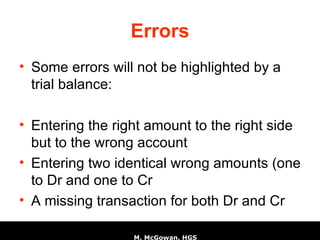

The document is a trial balance for an accounting firm that checks ledger entries balance. It lists account names and balances, with notes explaining that bank overdraft and owner's drawings have credit balances, while capital is the balancing figure. Errors like entering amounts to the wrong account or missing matching transactions will not be caught by a trial balance.