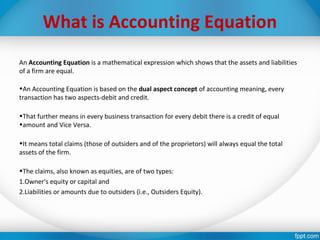

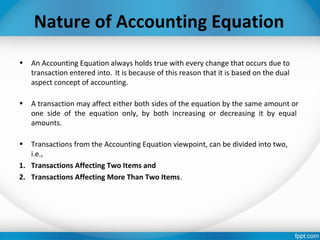

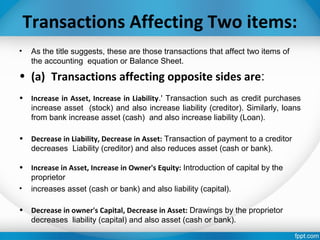

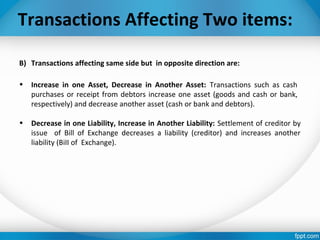

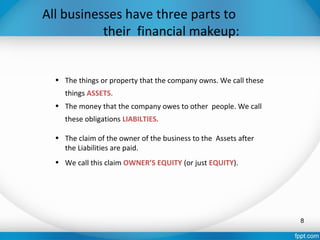

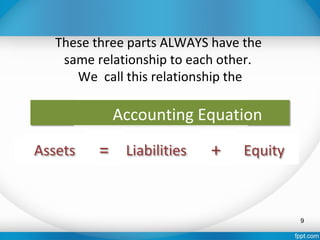

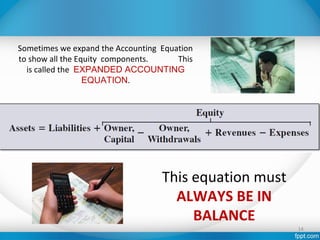

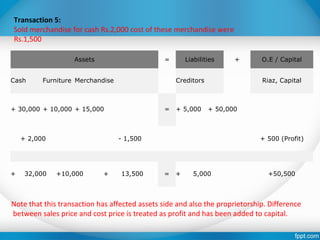

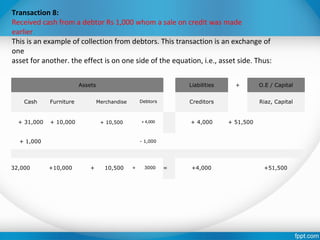

The accounting equation shows that a firm's assets are always equal to its liabilities plus owner's equity. It is based on the dual aspect concept where every transaction has equal debit and credit effects. The accounting equation always holds true as it is affected by transactions that may increase or decrease either one or two sides of the equation by equal amounts. Examples are provided to illustrate how common business transactions impact the accounting equation components of assets, liabilities, and owner's equity.