Downloaded 22 times

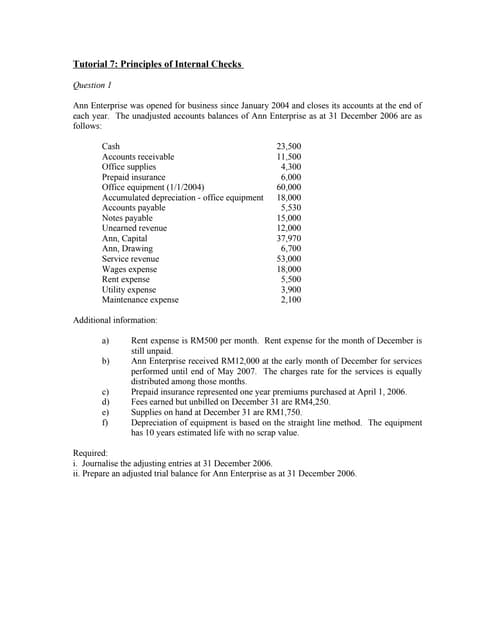

This document contains information about various accounting concepts and records: 1. It discusses the components of the profit and loss account including manufacturing account, trading account, profit and loss account, and profit and loss appropriation account. 2. It describes the key components and order of a balance sheet including real accounts, personal accounts, unamortized nominal accounts, and the uniform format for company balance sheets. 3. It provides examples of trial balance entries for various accounts like salaries, purchases, drawings, debtors, creditors, and capital for a sample trial balance.

![Csac06[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac061-p-110520054419-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac05[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac051-p-110520054504-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Working and functions_of_rbi[1]](https://cdn.slidesharecdn.com/ss_thumbnails/workingandfunctionsofrbi1-110522002449-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac08[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac081-p-110520054521-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac10[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac101-p-110520054545-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac14[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac141-p-110520054443-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)