Downloaded 113 times

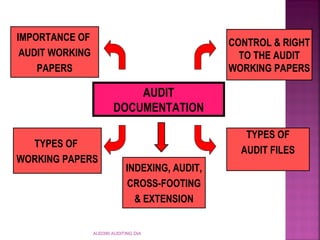

The document discusses audit documentation, also known as audit working papers. It defines audit documentation as the principal record of auditing procedures applied, evidence obtained, and conclusions reached. It should contain information needed to conduct the audit and prepare an audit report. The summary includes three key points about audit documentation: 1. Audit documentation includes a record of evidence accumulated, results of tests performed, documentation of significant findings, and basis for conclusions. 2. Audit documentation provides a basis for audit planning, review by supervisors, and determining the appropriate audit report. 3. Ownership of the audit files belongs to the auditor, and the files are considered confidential.

![AUDIT PLANNING AND PROCEDURES [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/4777auditplanningandproceduresautosaved-240818090542-6370a7b2-thumbnail.jpg?width=640&height=640&fit=bounds)