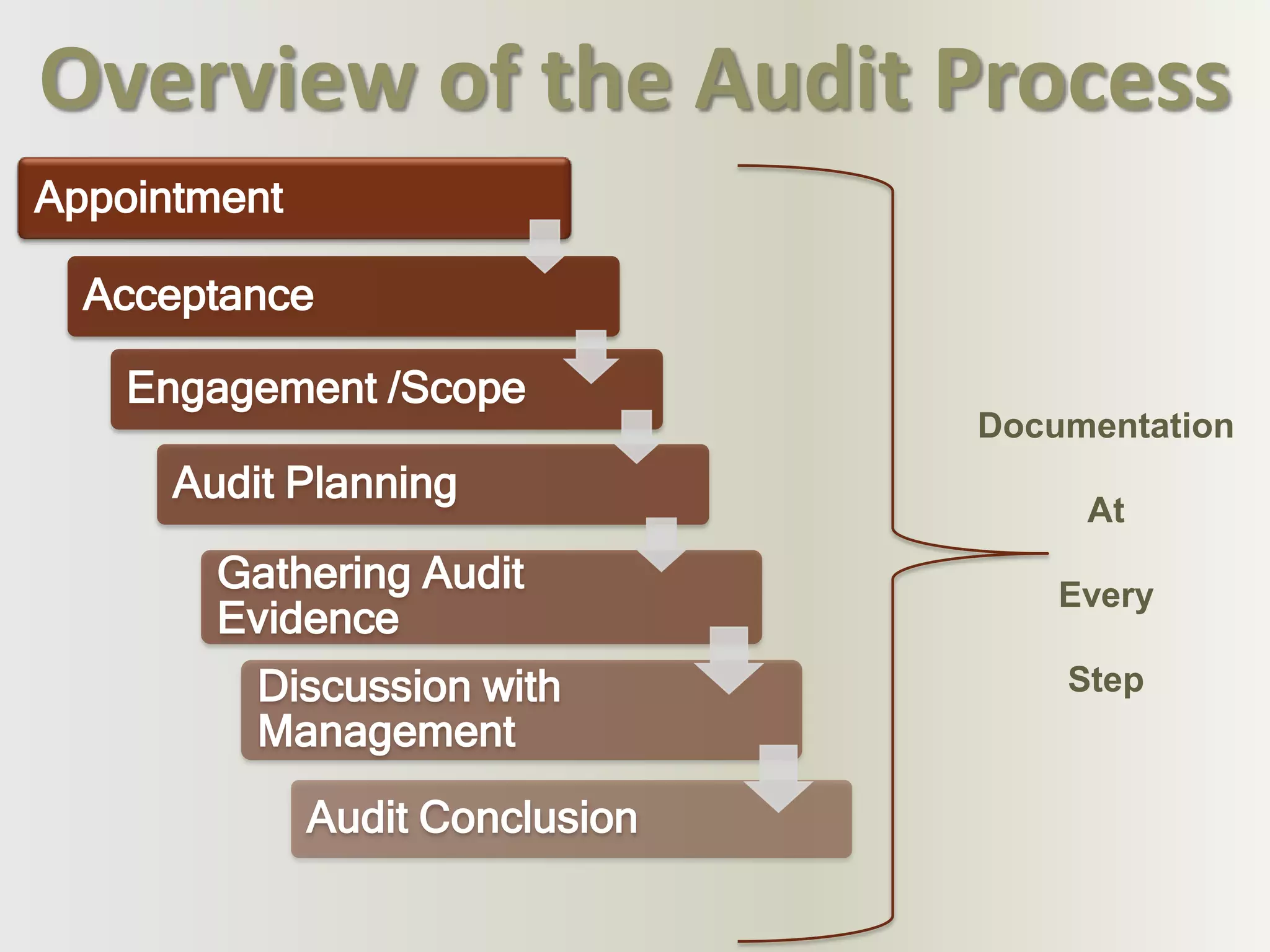

Maintaining audit documentation is important to demonstrate the work performed was sufficient and in accordance with auditing standards. The audit documentation should provide a clear understanding of the work done, evidence obtained, and conclusions reached.

![Audit evidence a framework (ppt ch7[1].pdf)](https://cdn.slidesharecdn.com/ss_thumbnails/auditevidence-aframeworkpptch71-pdf-121211154609-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)