Downloaded 706 times

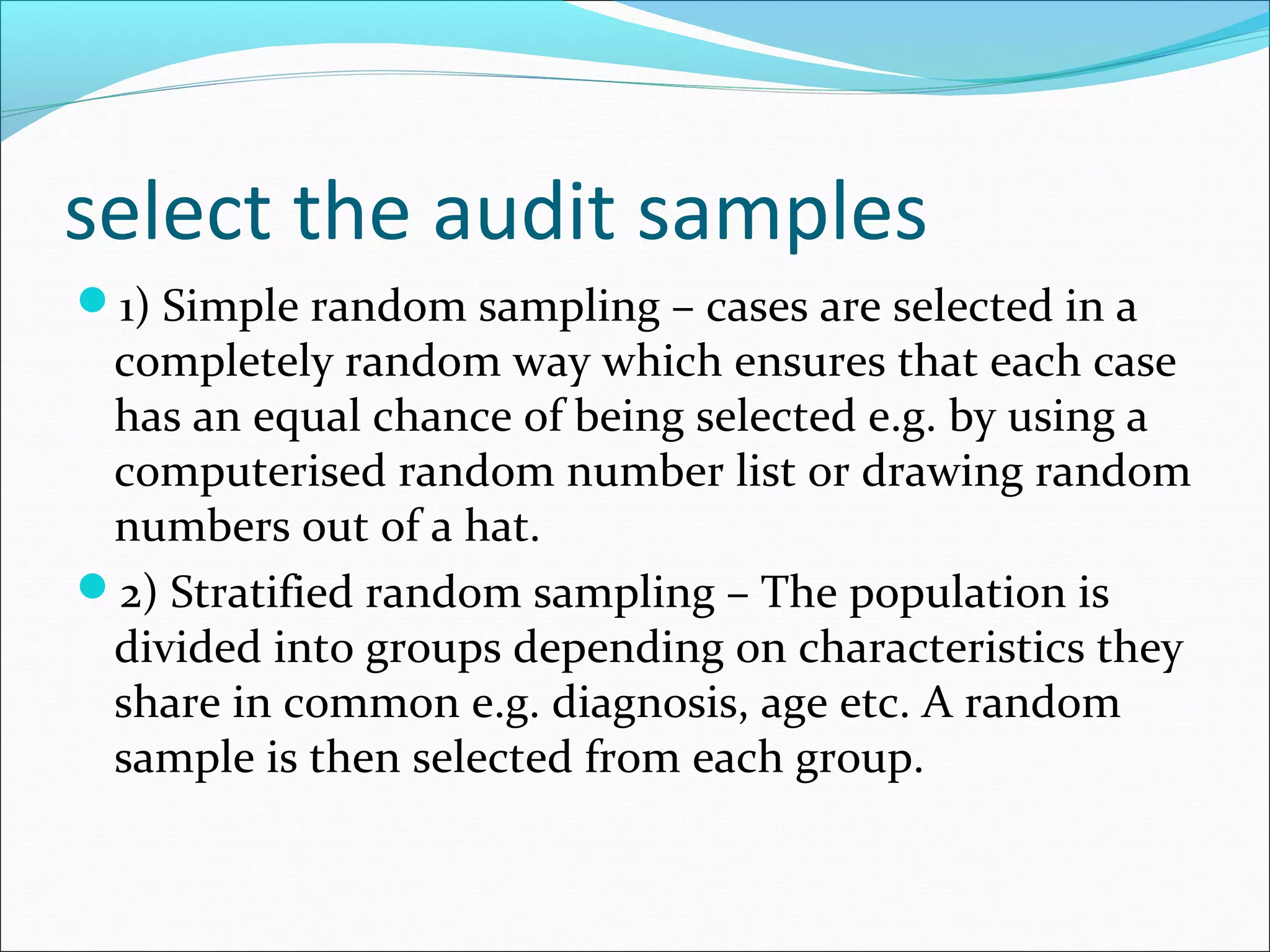

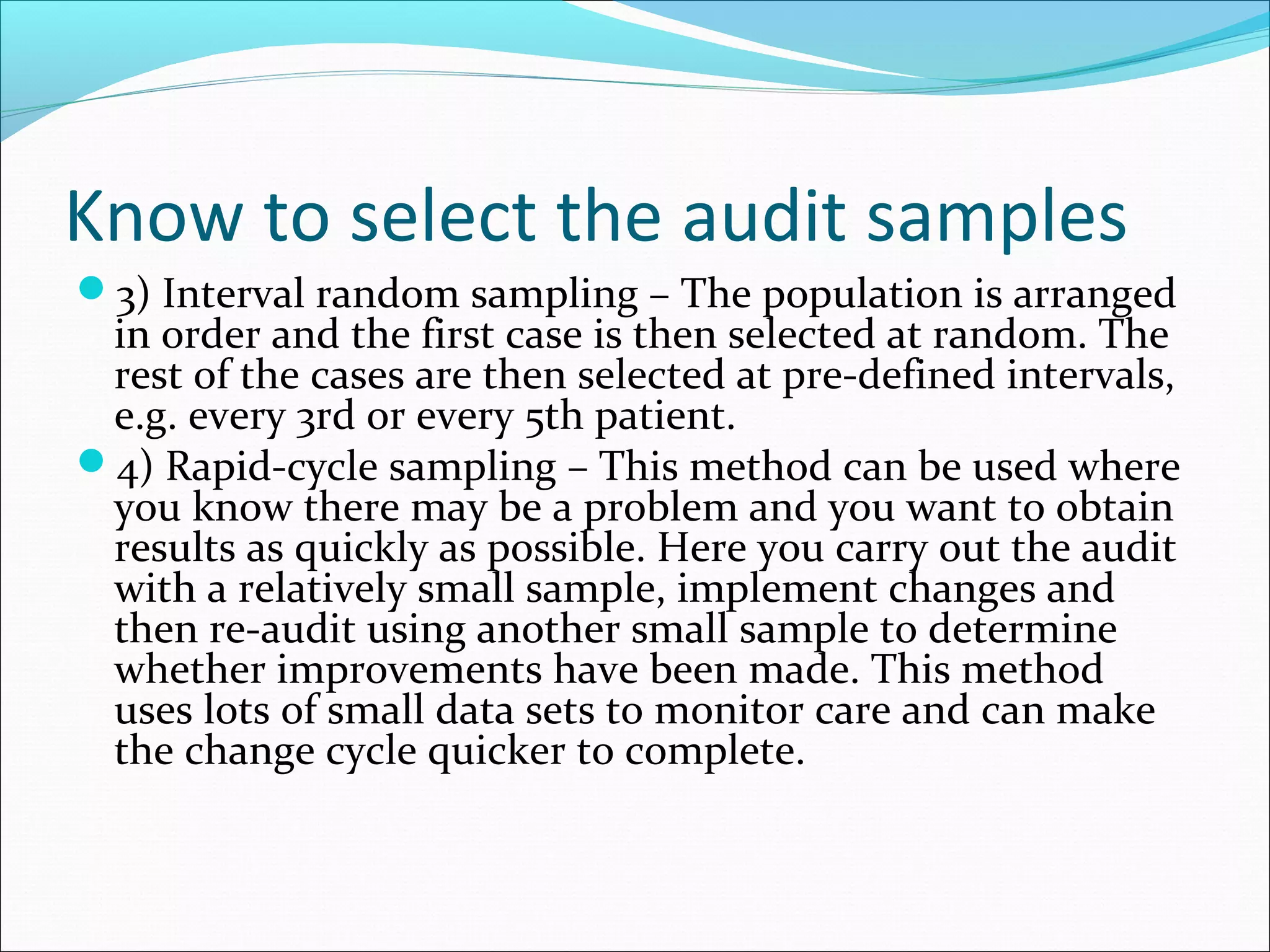

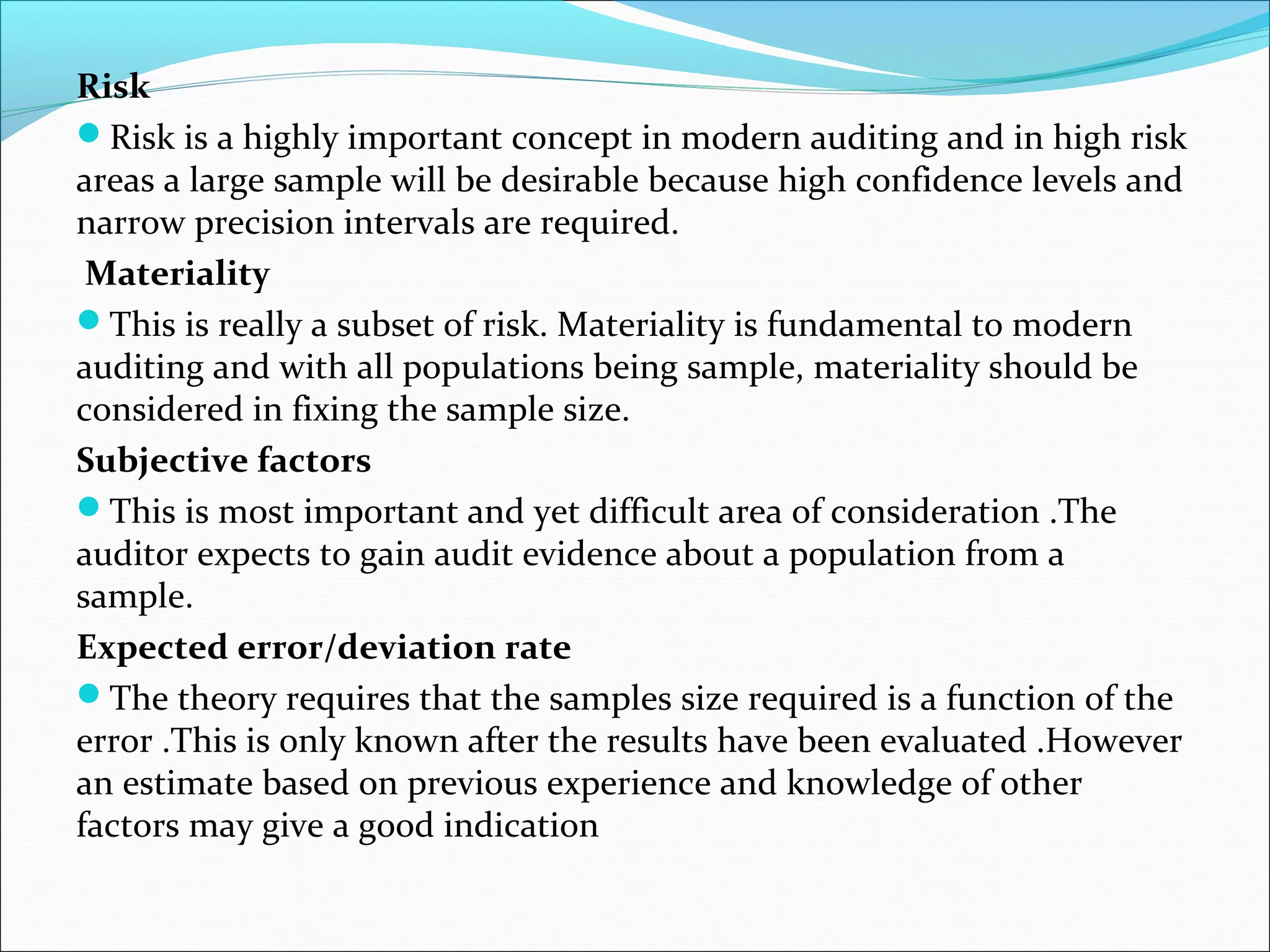

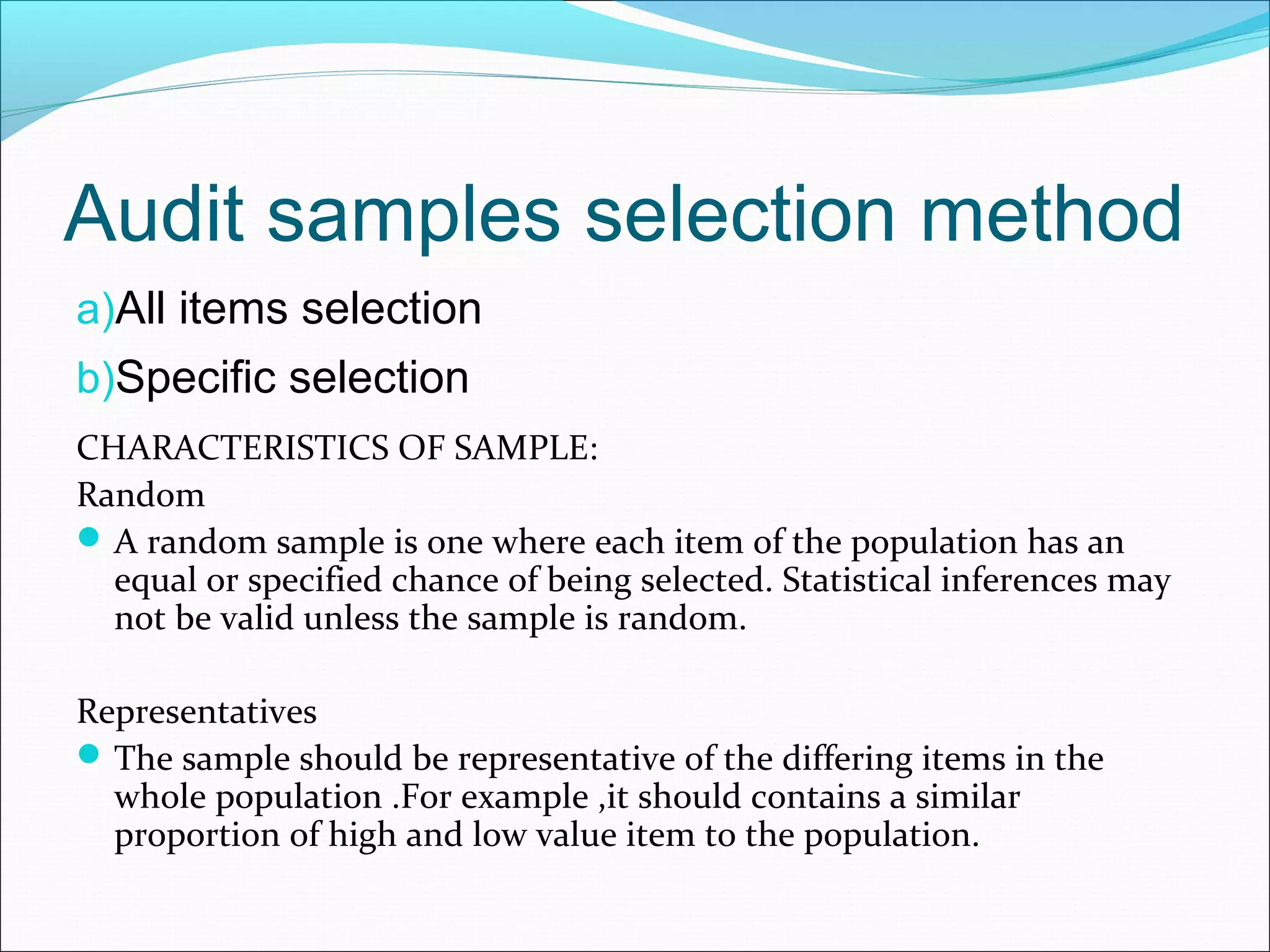

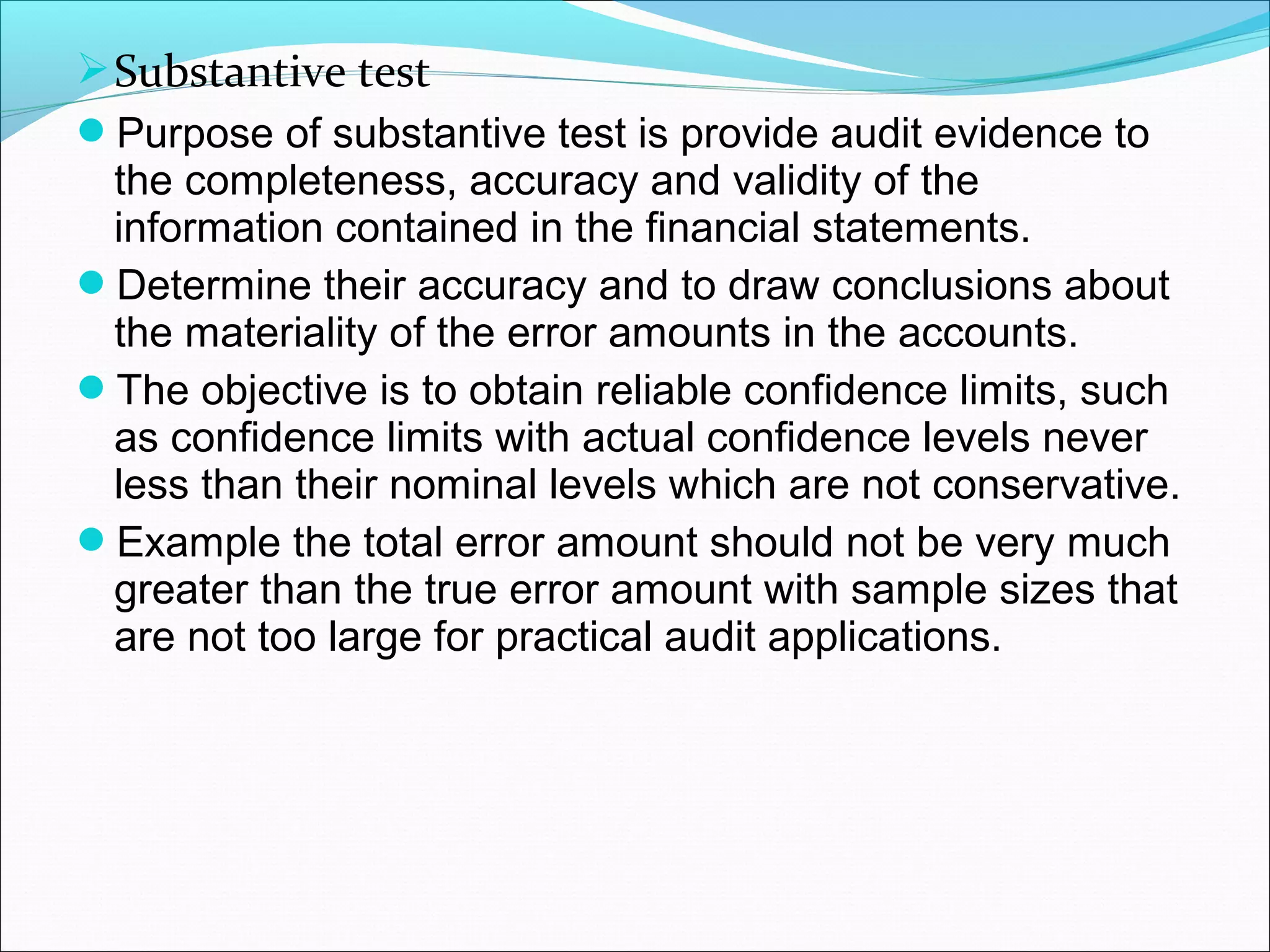

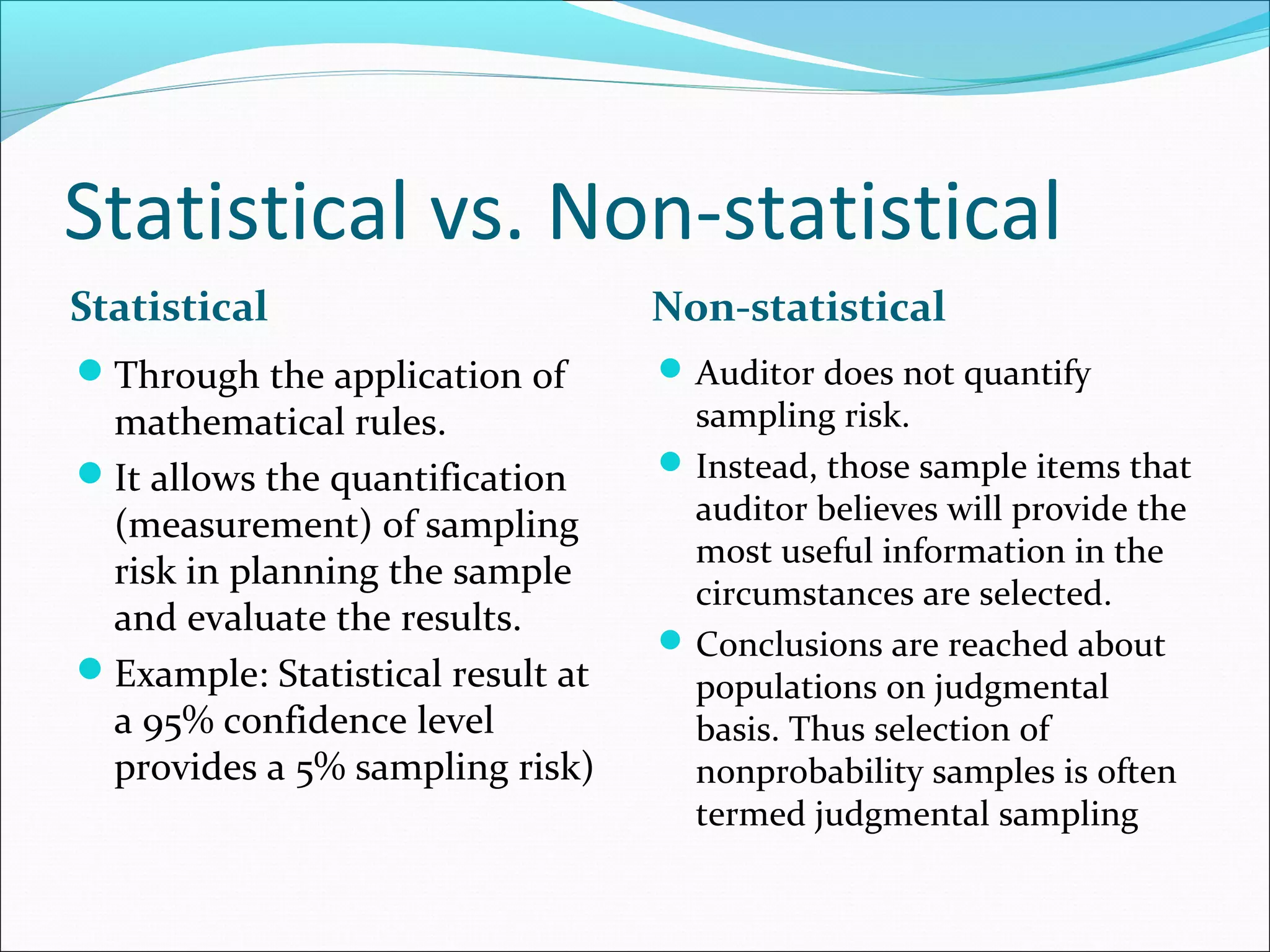

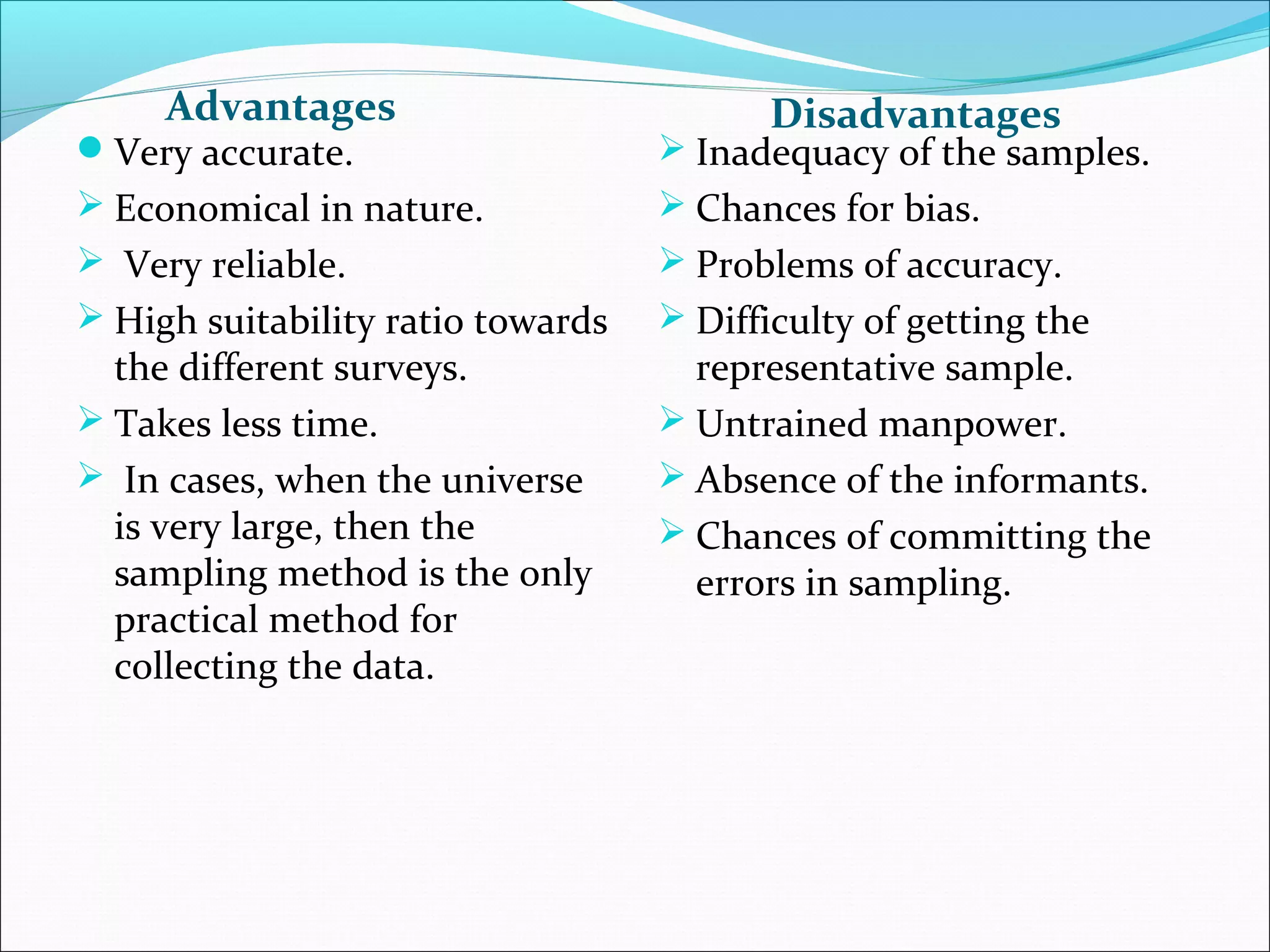

This document discusses audit sampling methods. It defines audit sampling as selecting a subset of a population for the purpose of making inferences about the whole population. Audit sampling helps auditors efficiently gather evidence and detect errors or misstatements. The document discusses factors that affect sample size, different sampling methods like simple random sampling and stratified random sampling, and the purposes of test of controls and substantive testing. It also compares statistical and non-statistical sampling methods.