Download as PDF, PPTX

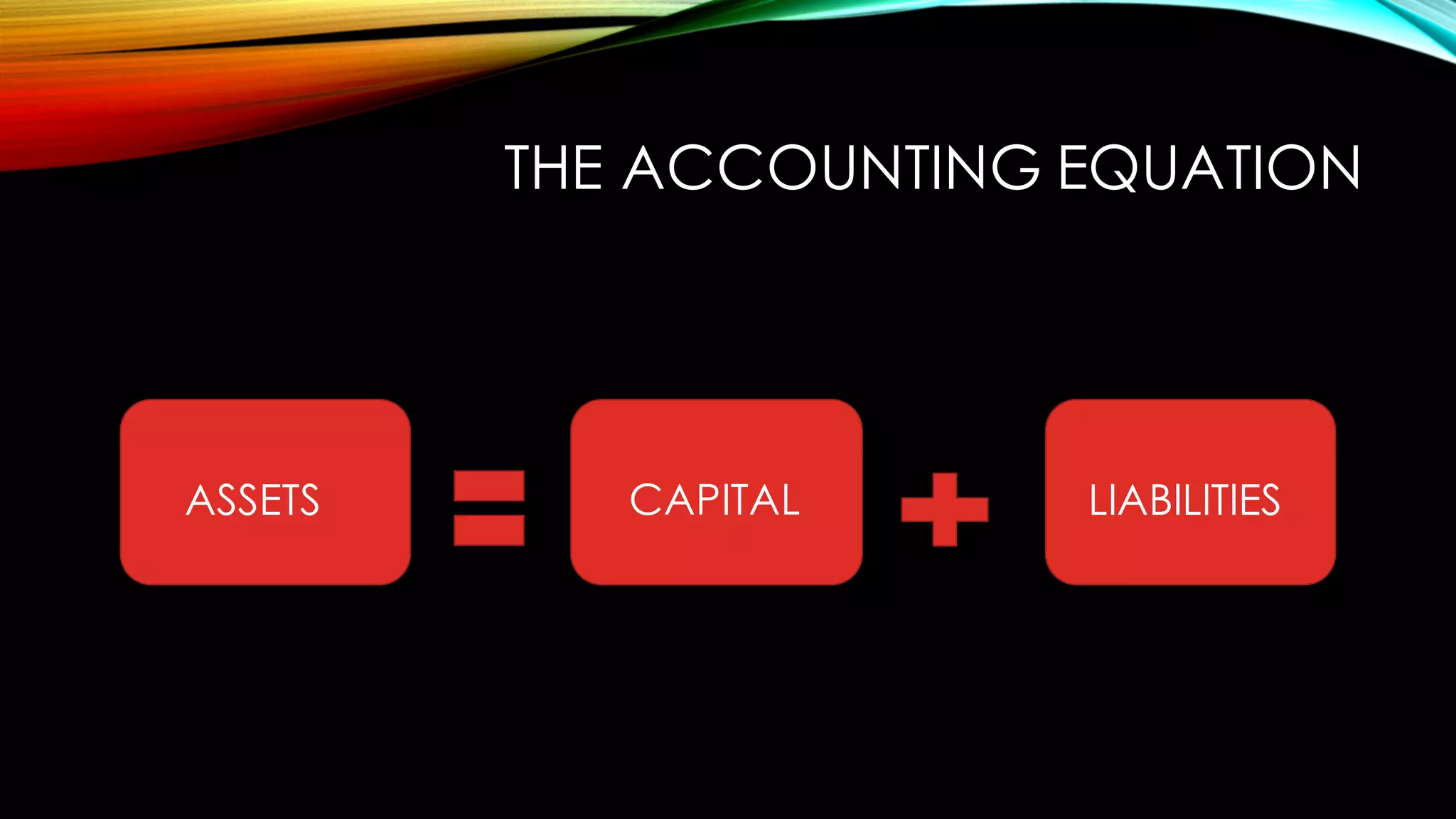

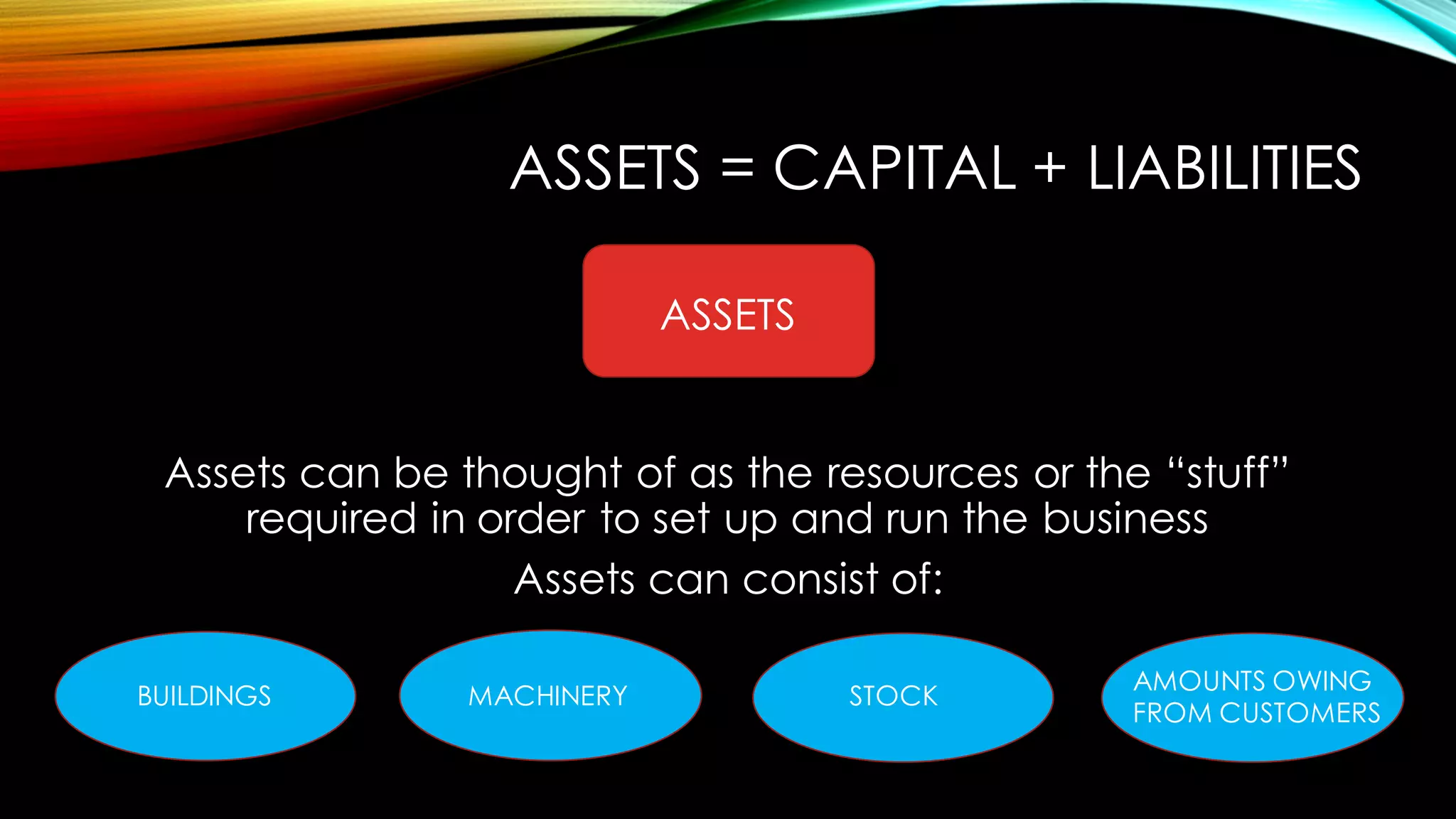

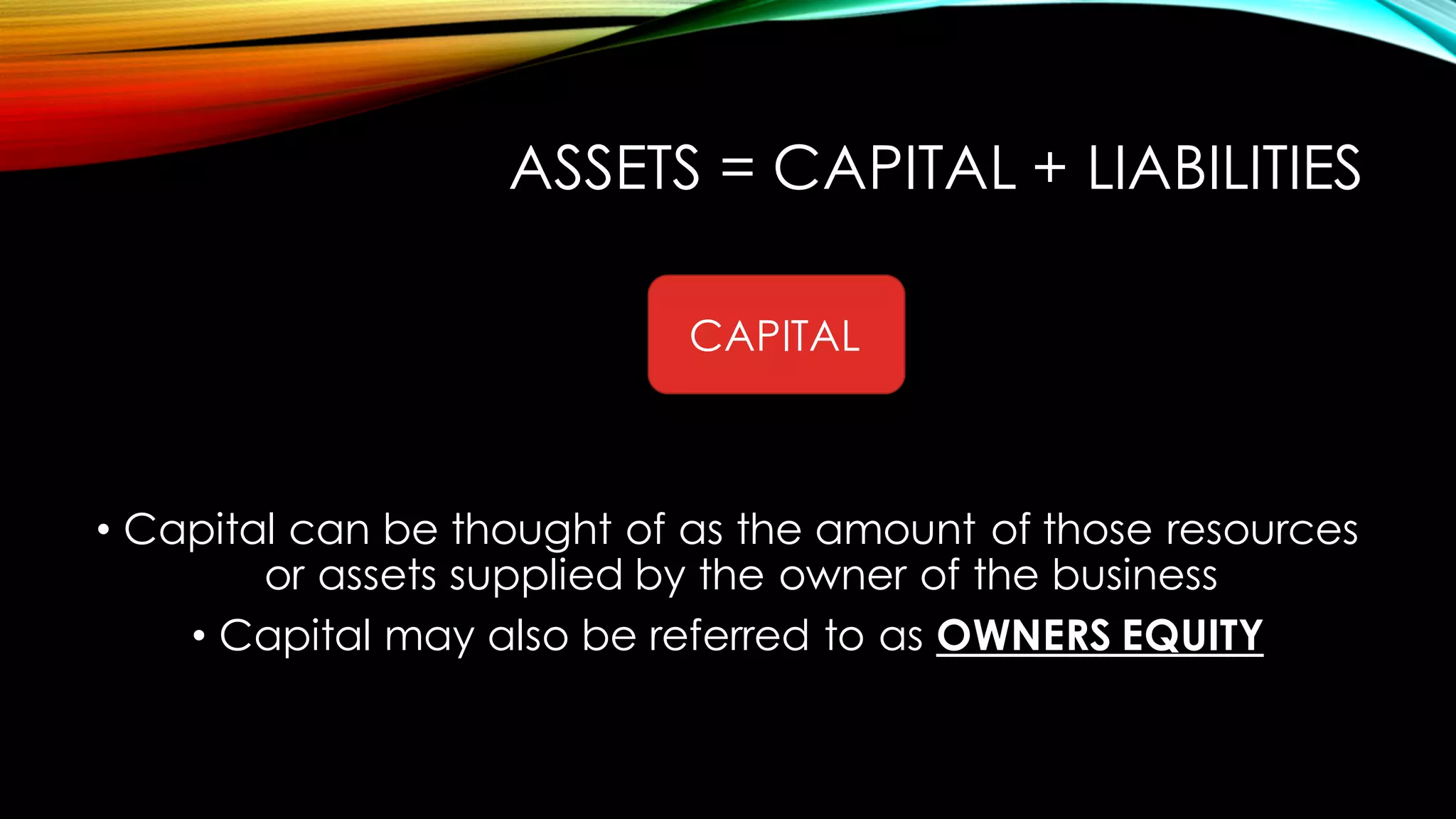

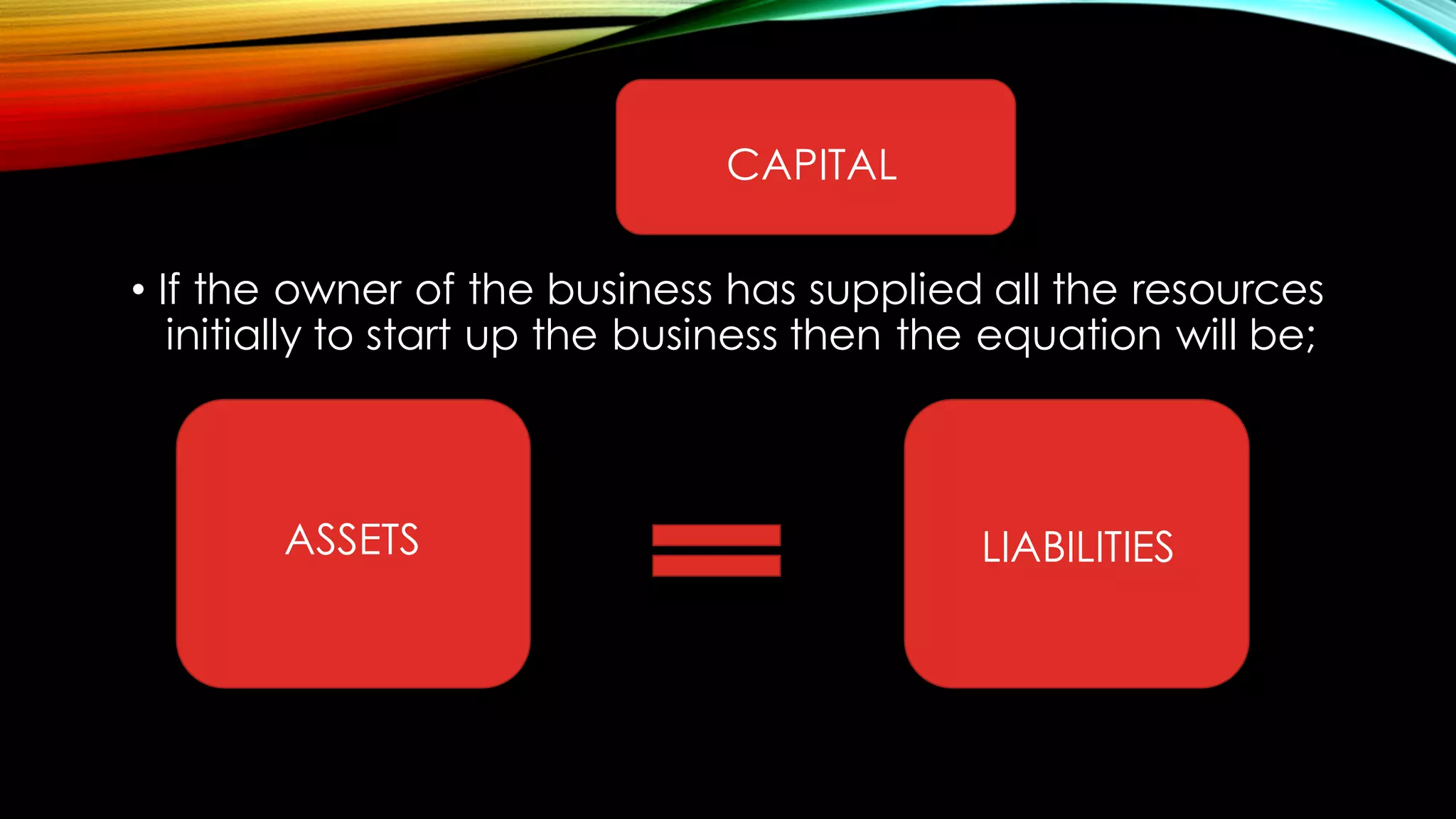

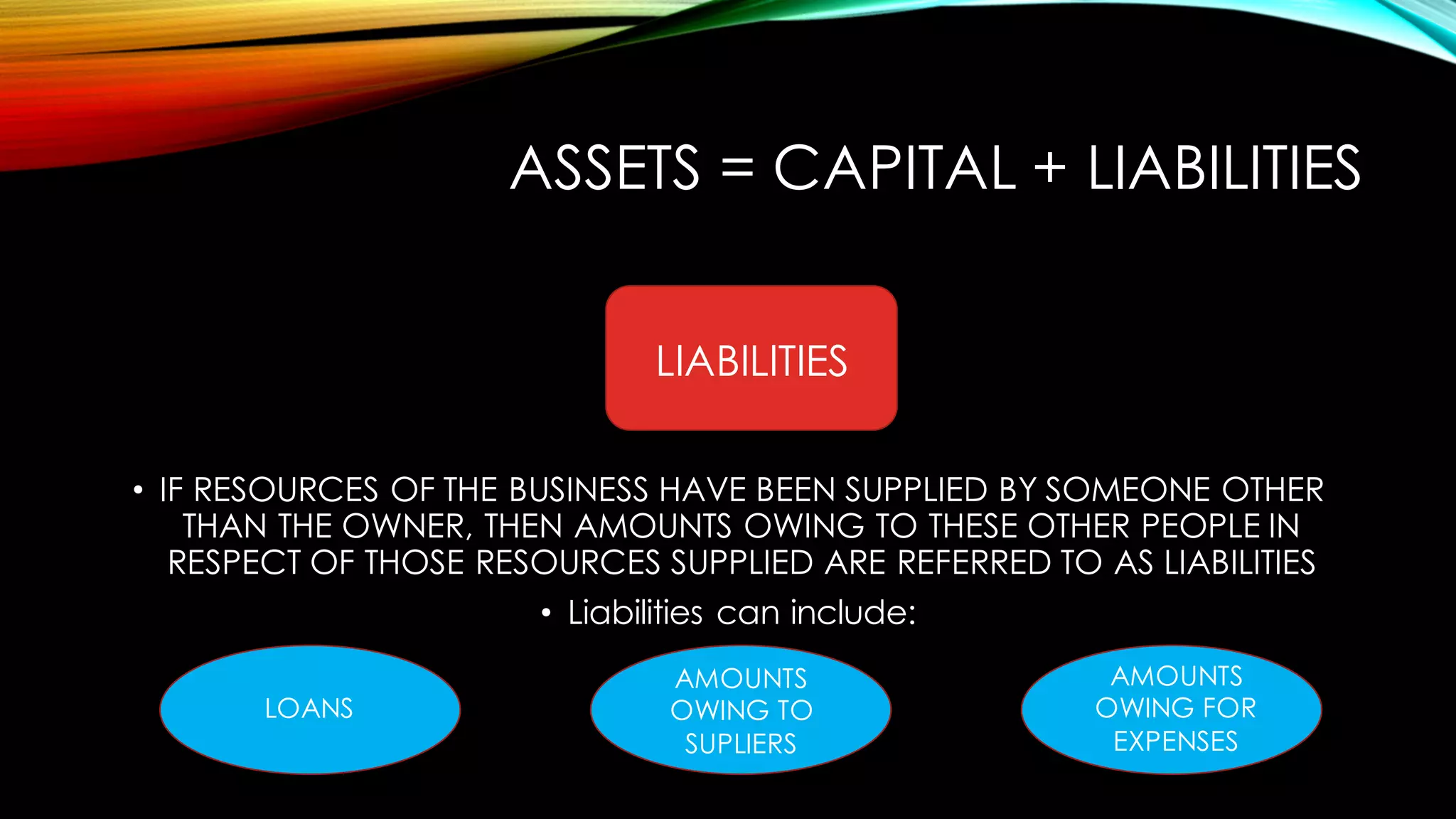

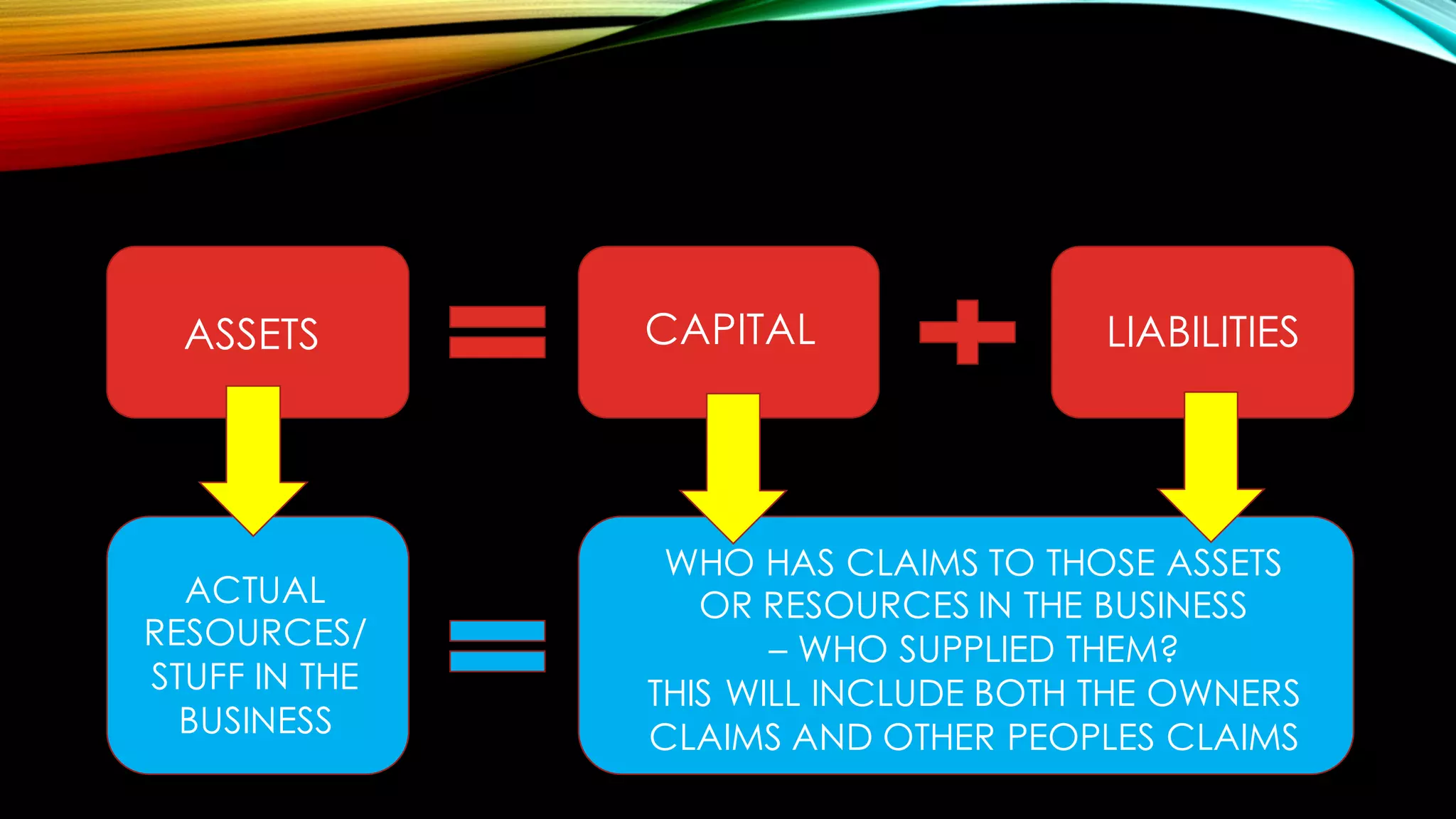

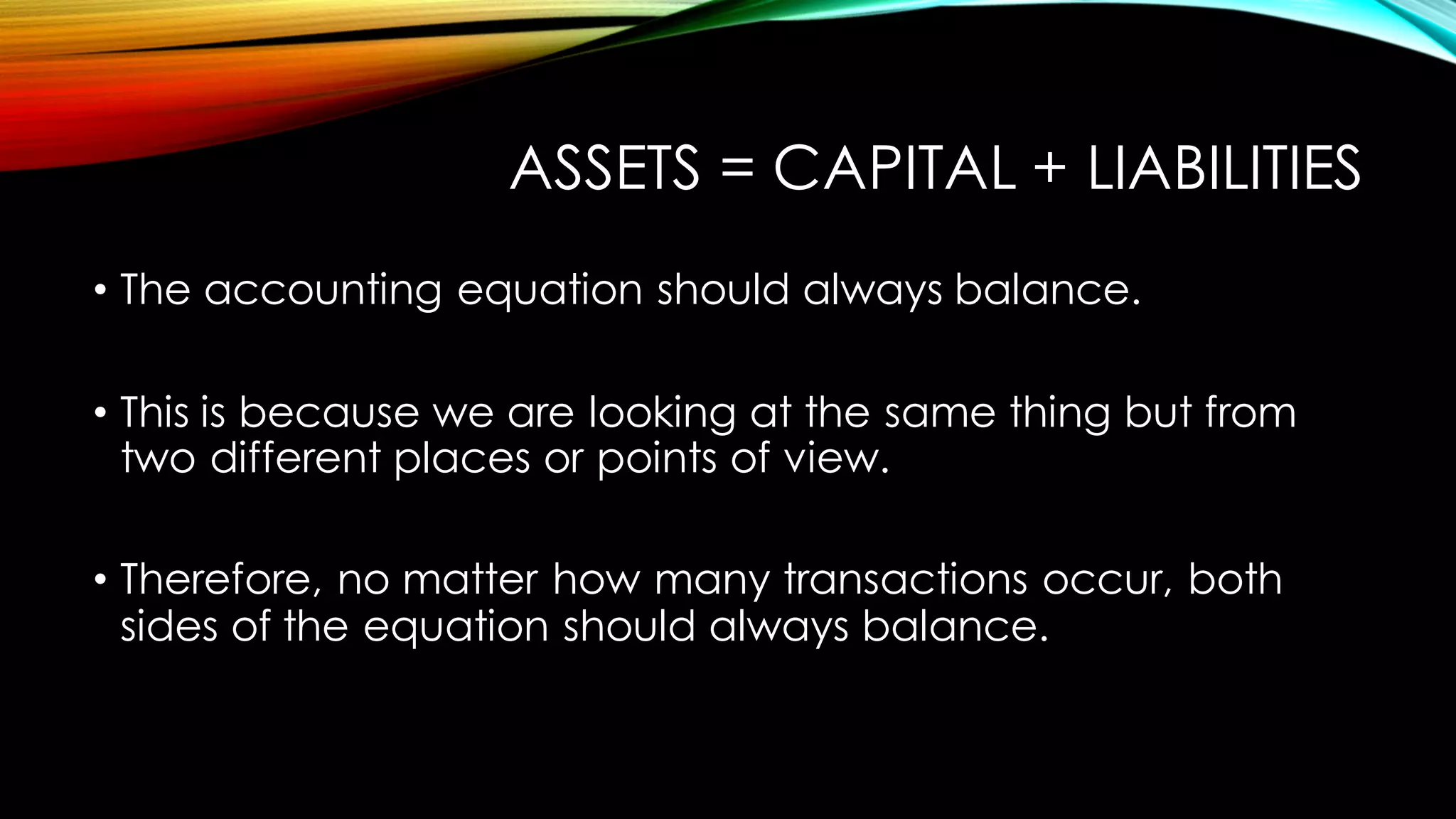

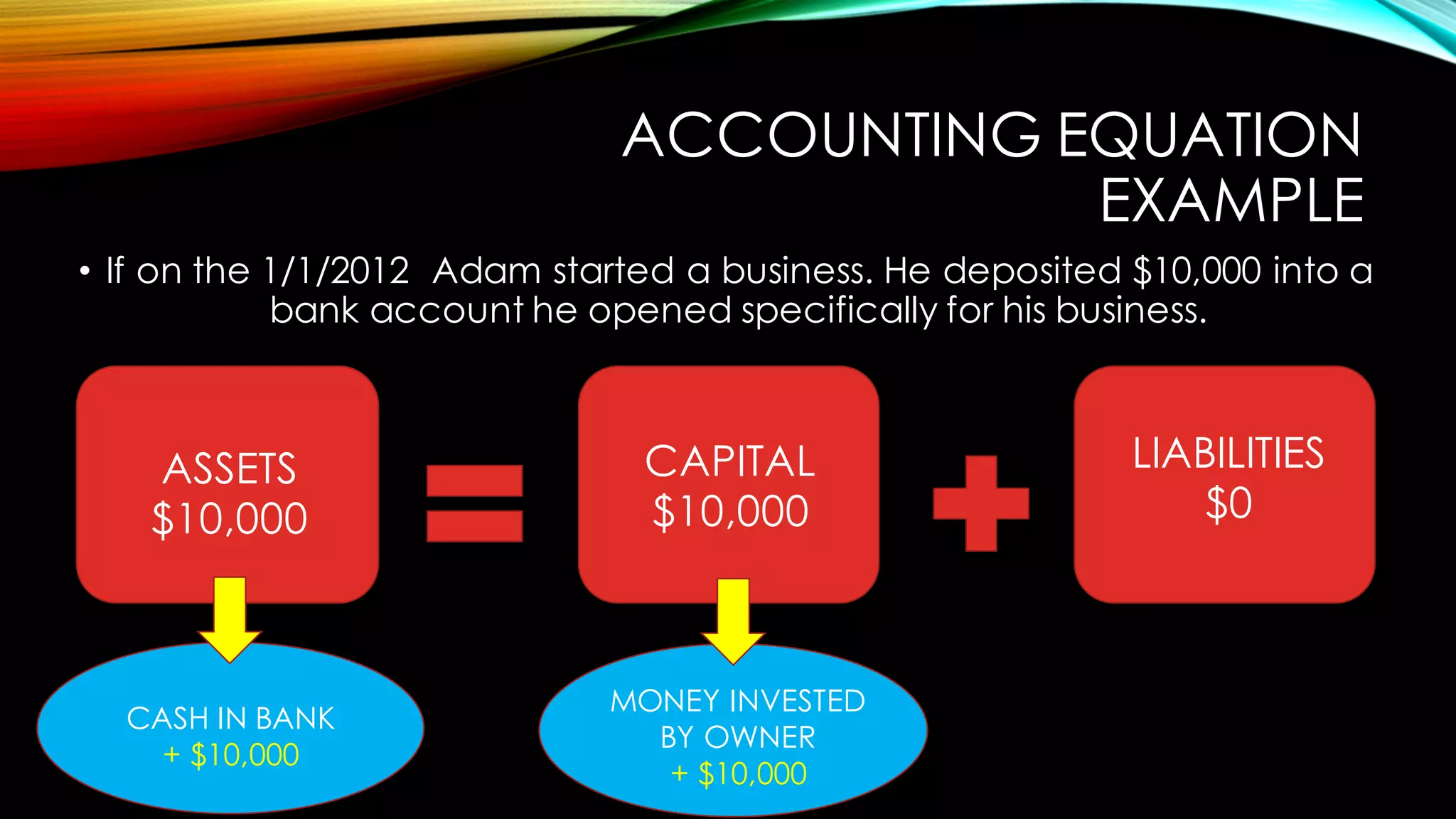

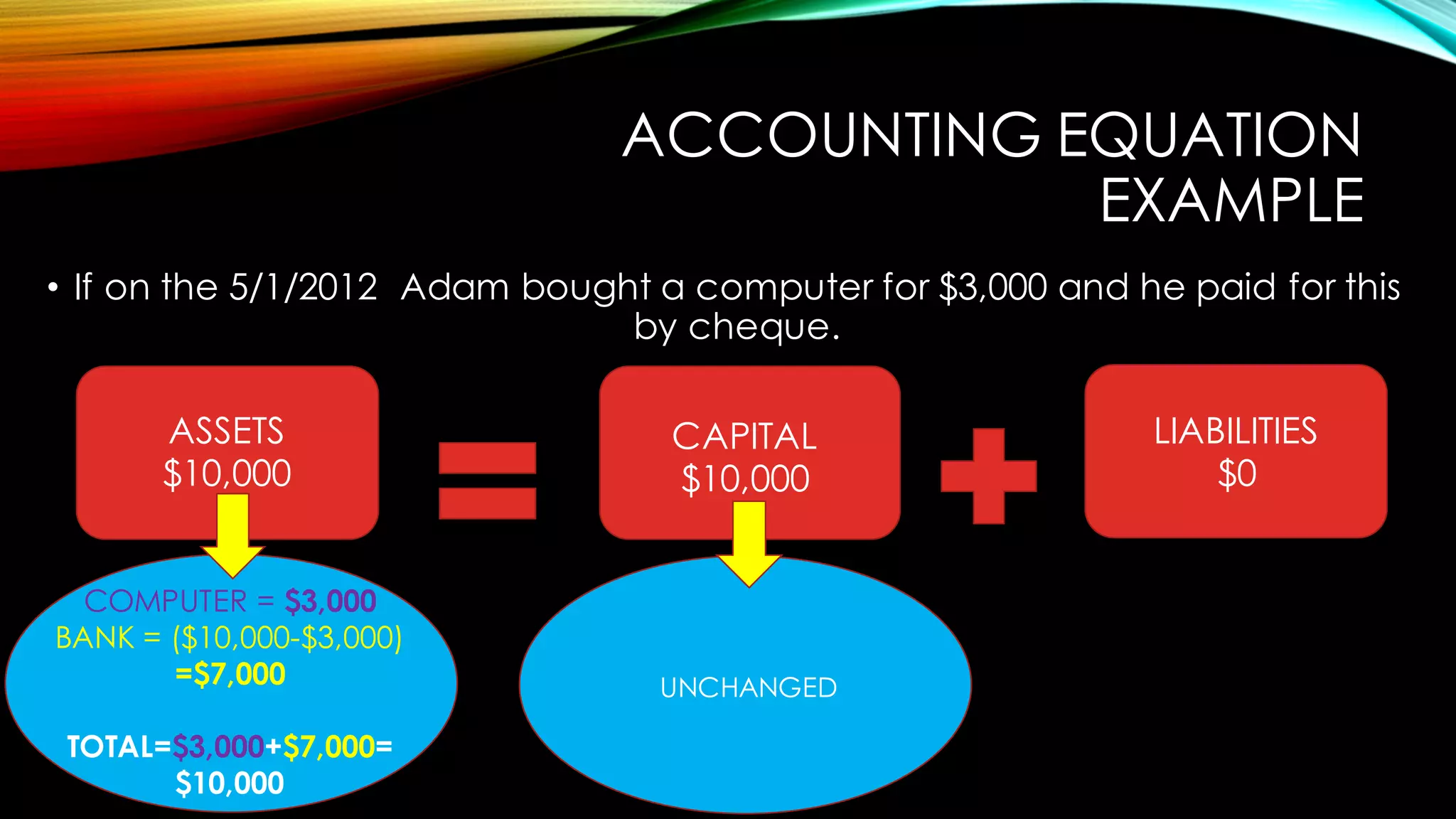

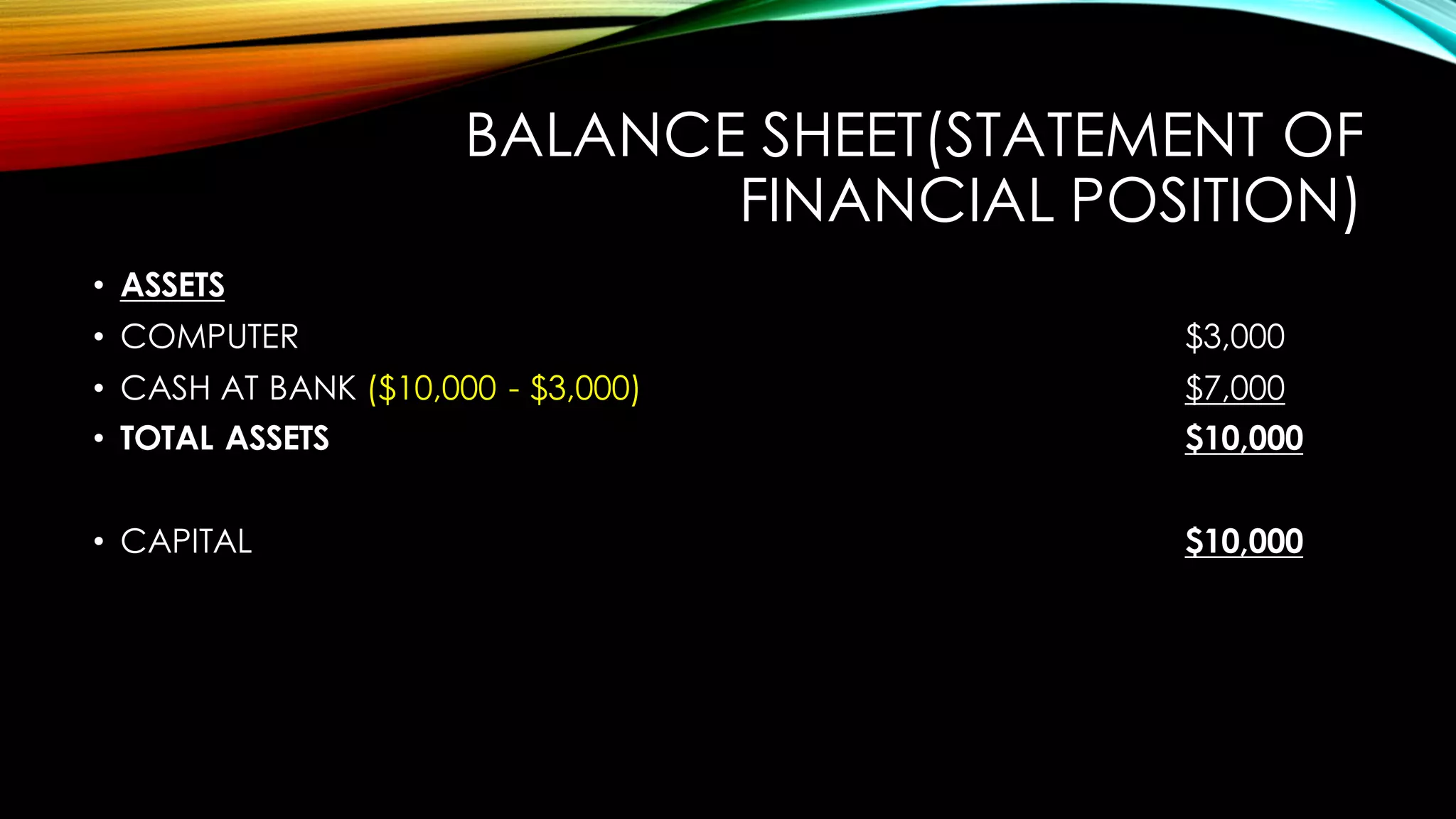

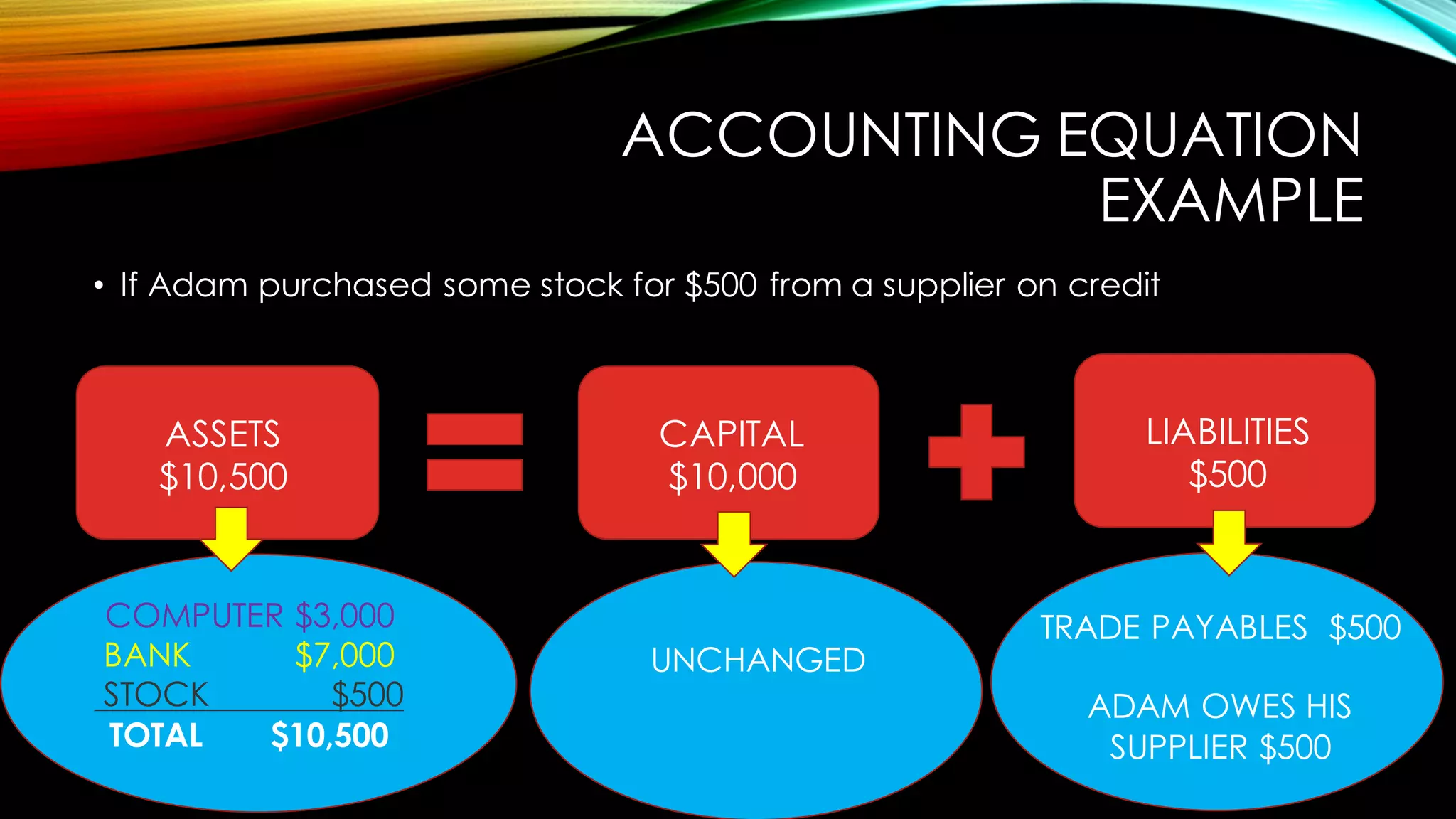

The accounting equation states that assets must always equal the sum of capital and liabilities. It is the fundamental concept in accounting that the resources (assets) of a business are supplied by either its owners (capital) or others it owes (liabilities). Assets represent the resources owned, capital represents the owners' claim to assets, and liabilities represent amounts owed to non-owners. The equation must always balance, as it reflects two ways of looking at the same financial position of a business. Examples are given to illustrate how transactions affect the components of the equation while maintaining the balance.