Downloaded 2,959 times

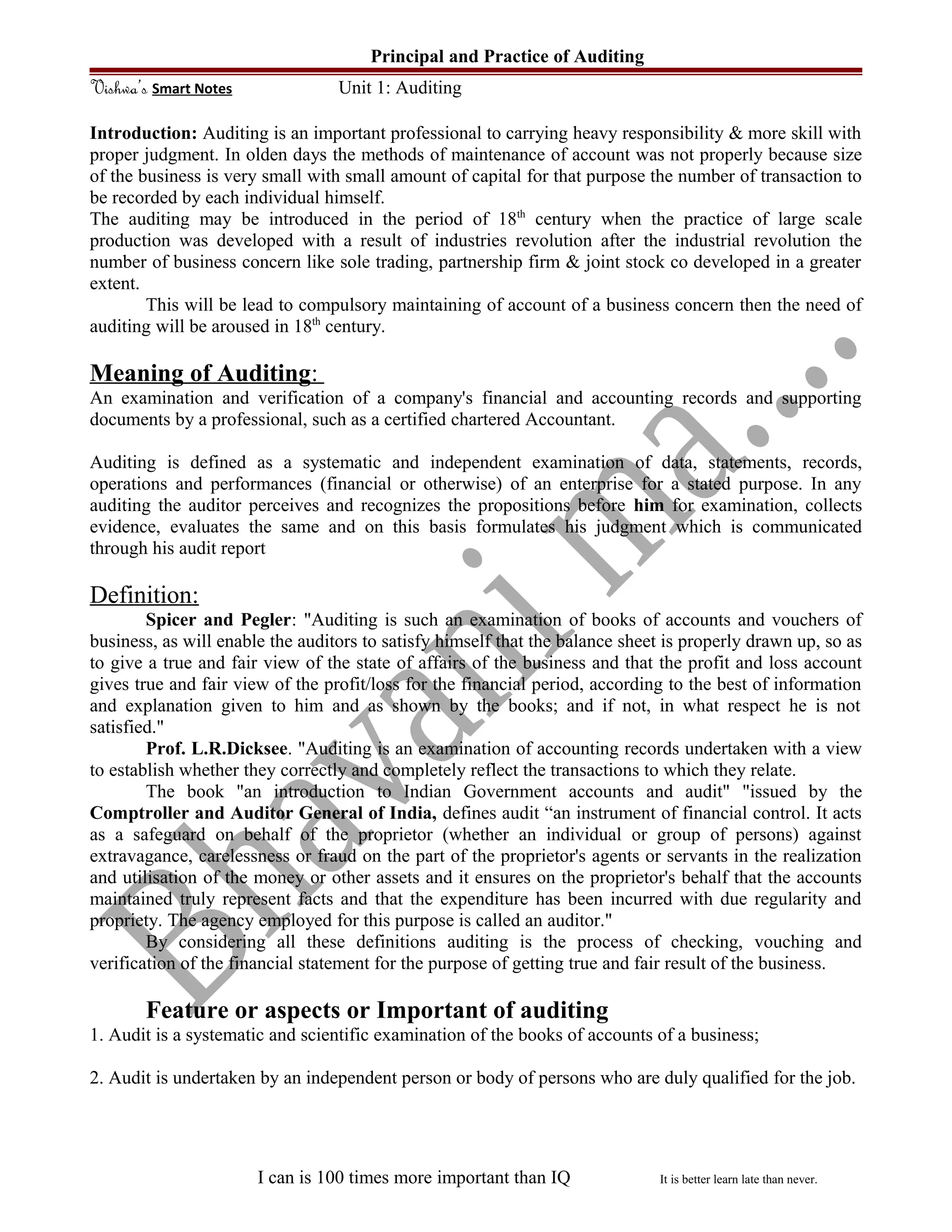

1. Auditing originated in the 18th century with the rise of large-scale industries and businesses, which led to more complex accounting practices. 2. Auditing involves the systematic and independent examination of a company's financial records and documents to verify that the financial statements accurately reflect the company's transactions and financial position. 3. Auditing provides benefits such as detecting errors and fraud, protecting shareholder interests, checking directors and management, and giving an independent opinion on the business's financial health. However, auditors also face limitations like not detecting every fraud and having to rely on information from company personnel.