Downloaded 36 times

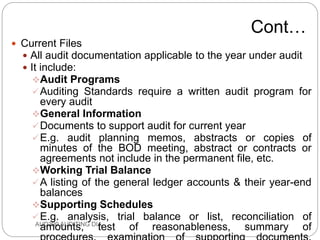

This document discusses audit documentation and working papers. It defines audit working papers as the principal record of auditing procedures applied, evidence obtained, and conclusions reached. It notes that working papers serve several purposes including planning and performing the audit, supervising and reviewing audit work, and gathering evidence to support the auditor's opinion. The document also describes the different types of working papers, including permanent files which contain historical data, and current files which contain all documentation for the current year audit. It addresses ownership, confidentiality, and exceptions for accessing working papers.

![AUDIT PLANNING AND PROCEDURES [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/4777auditplanningandproceduresautosaved-240818090542-6370a7b2-thumbnail.jpg?width=640&height=640&fit=bounds)