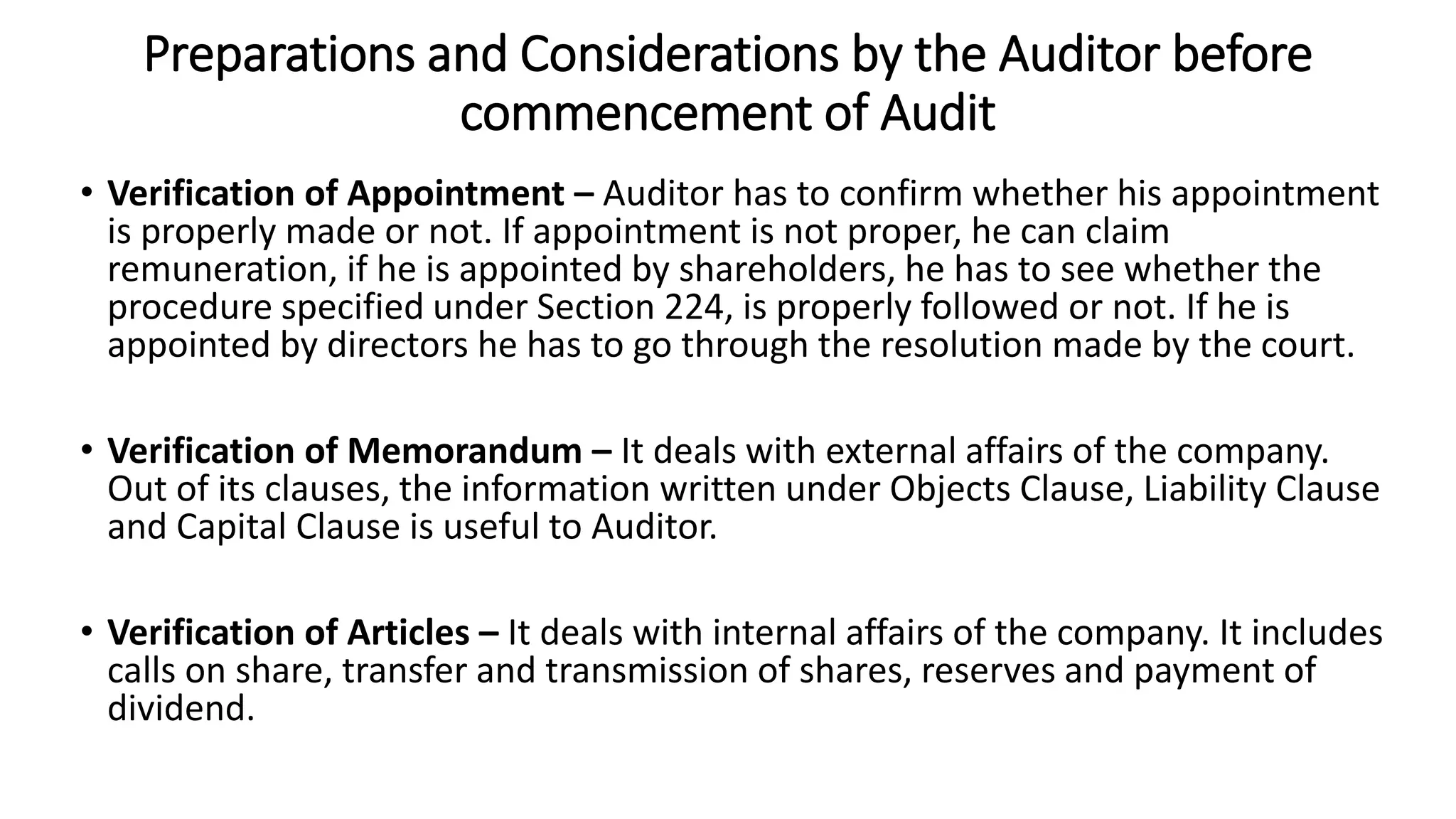

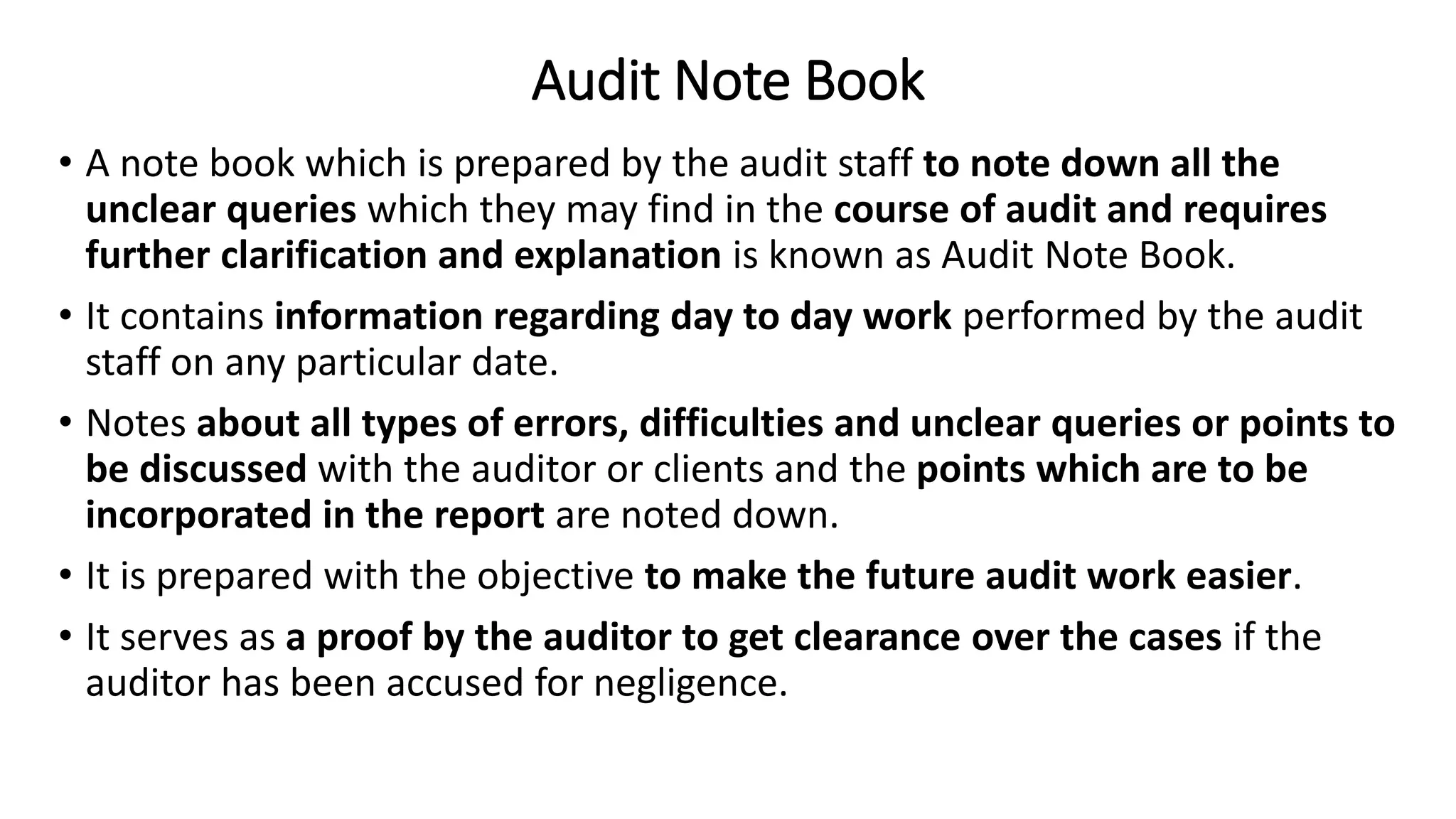

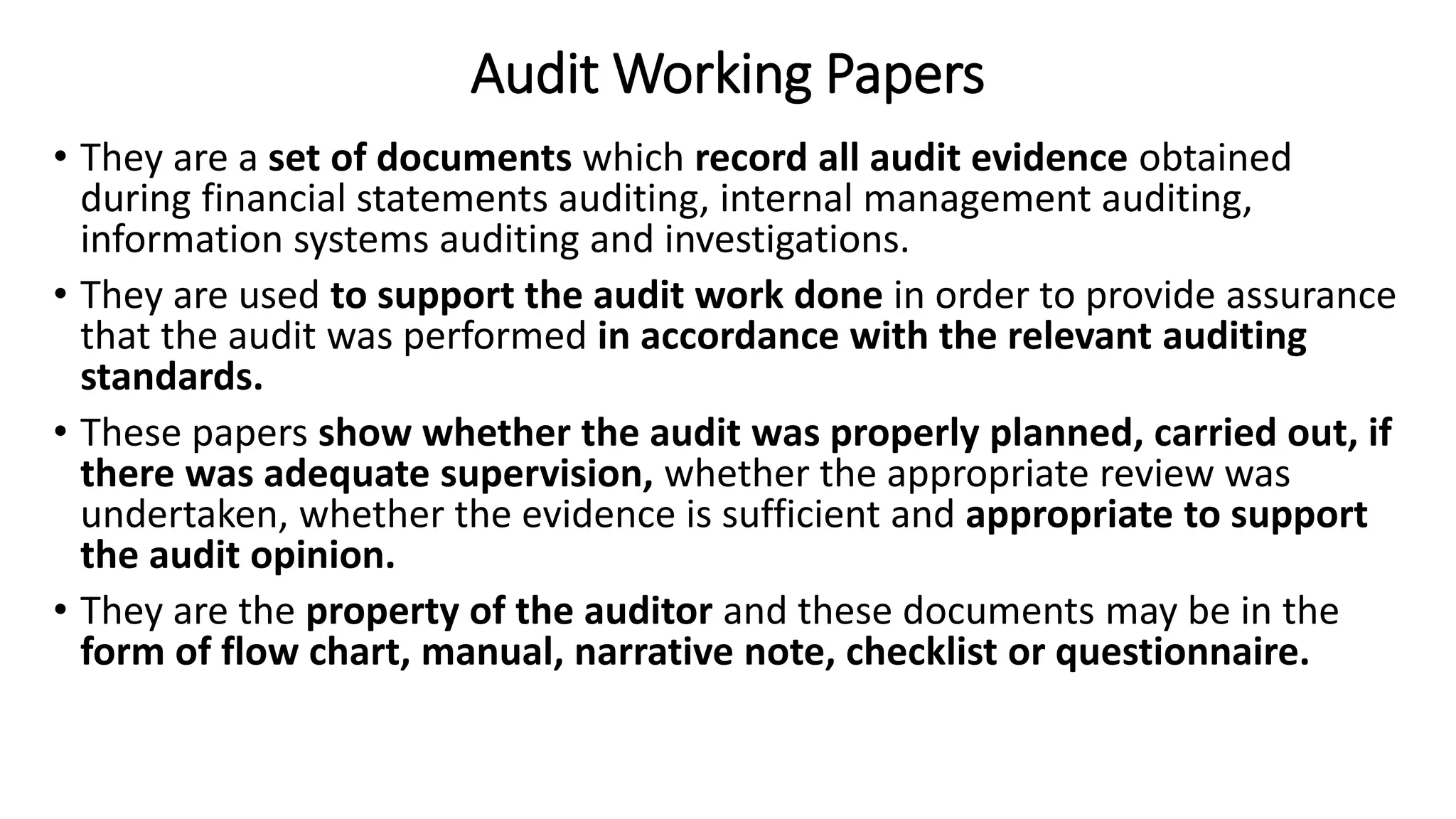

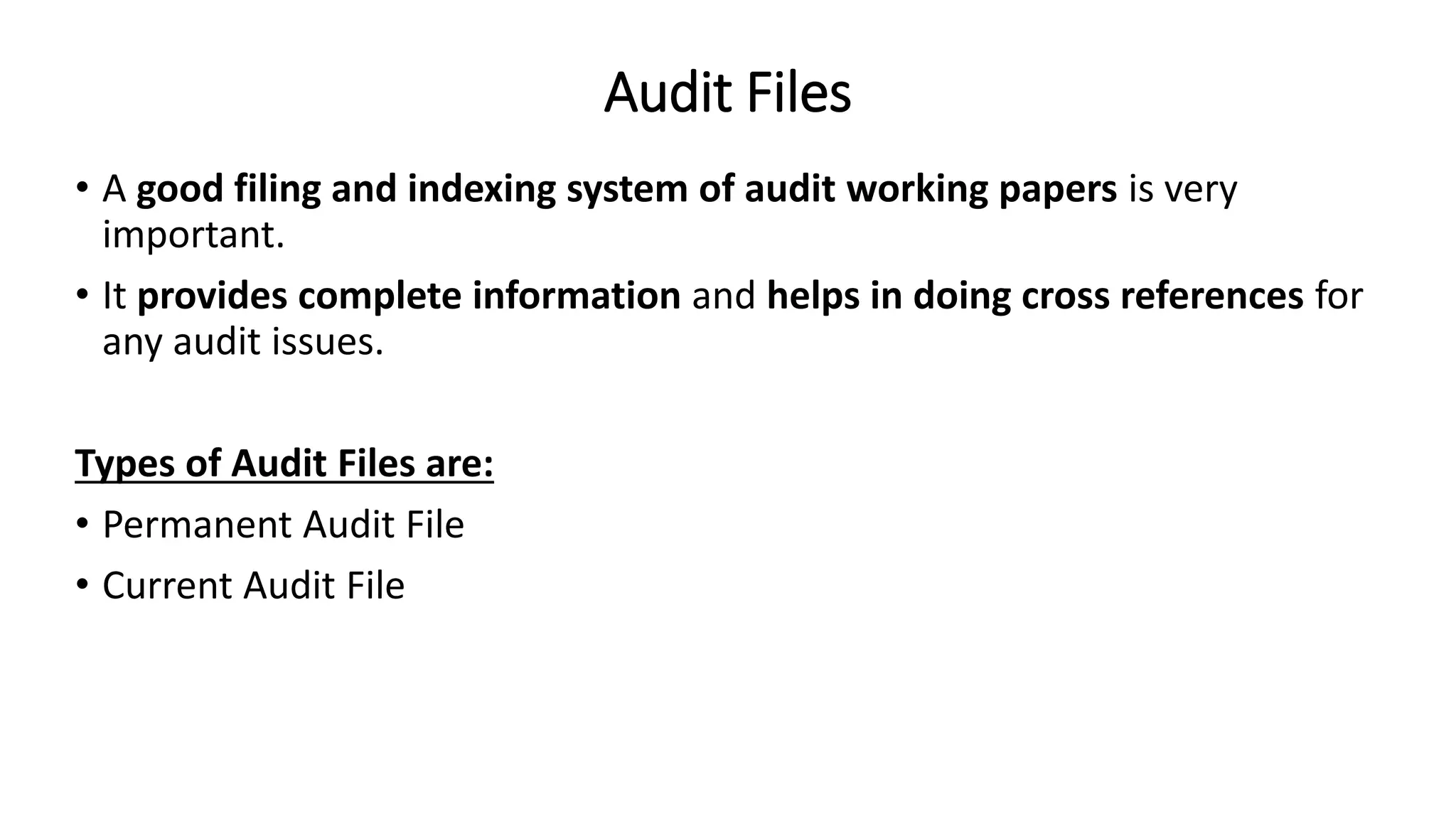

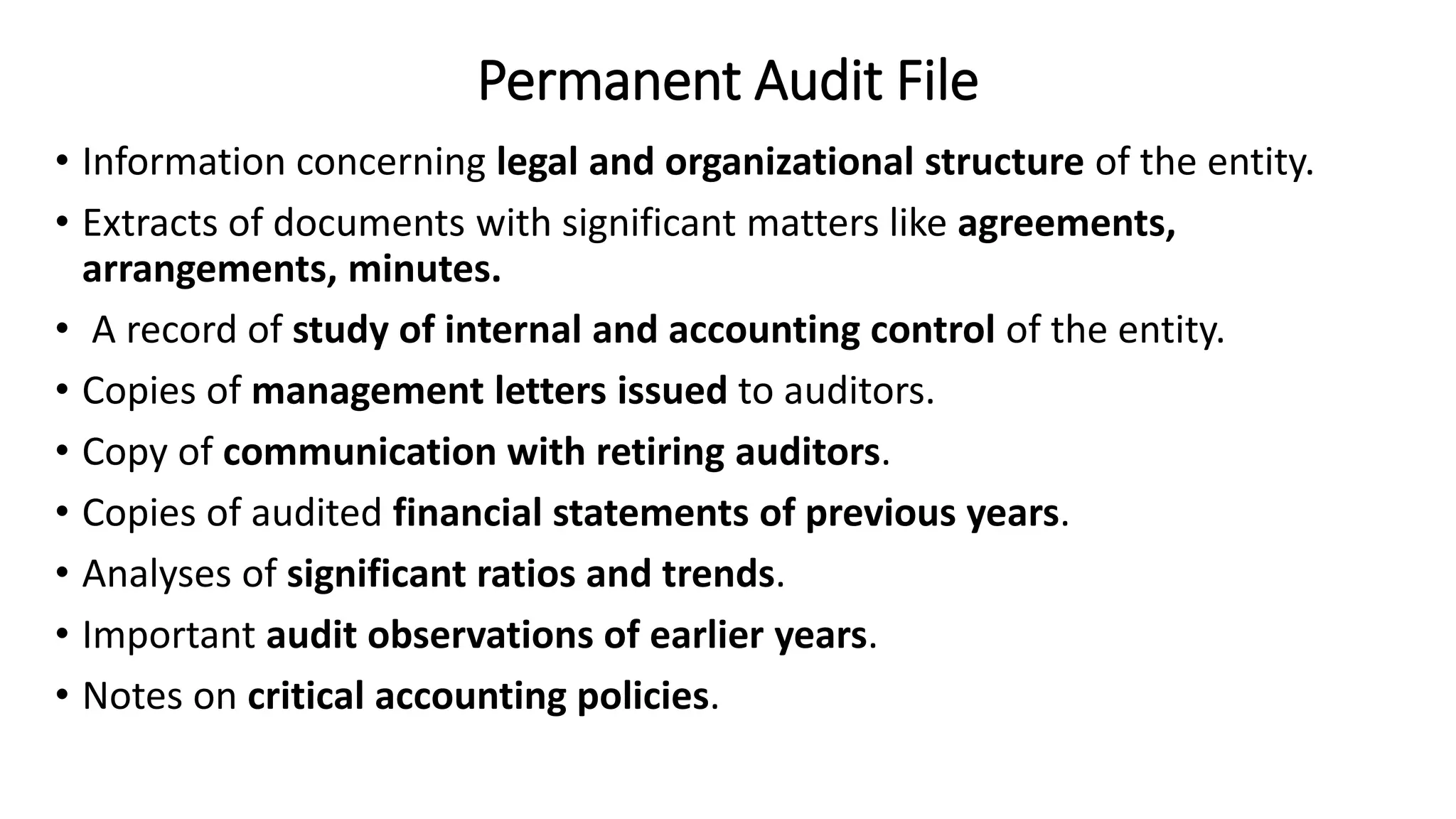

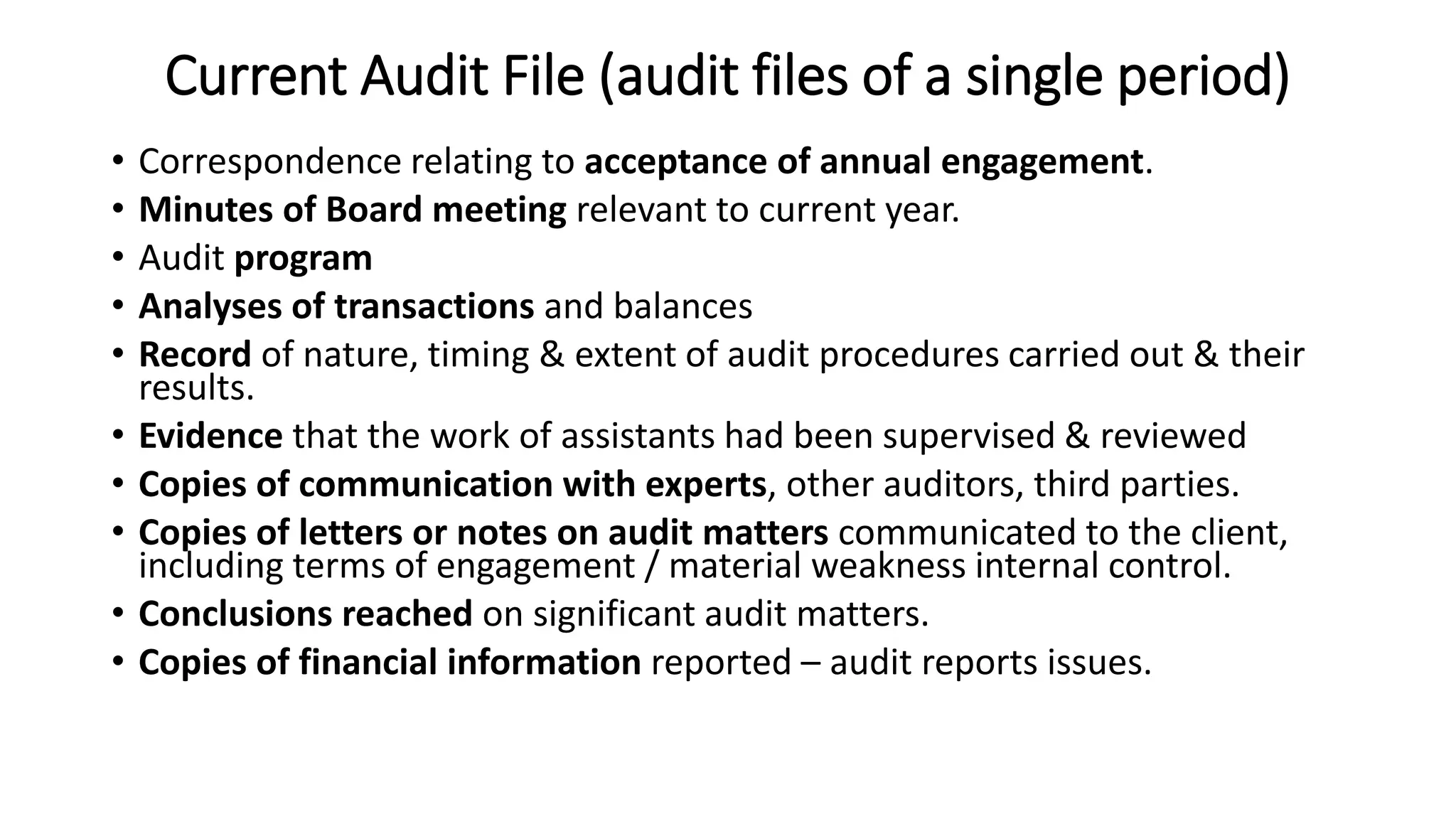

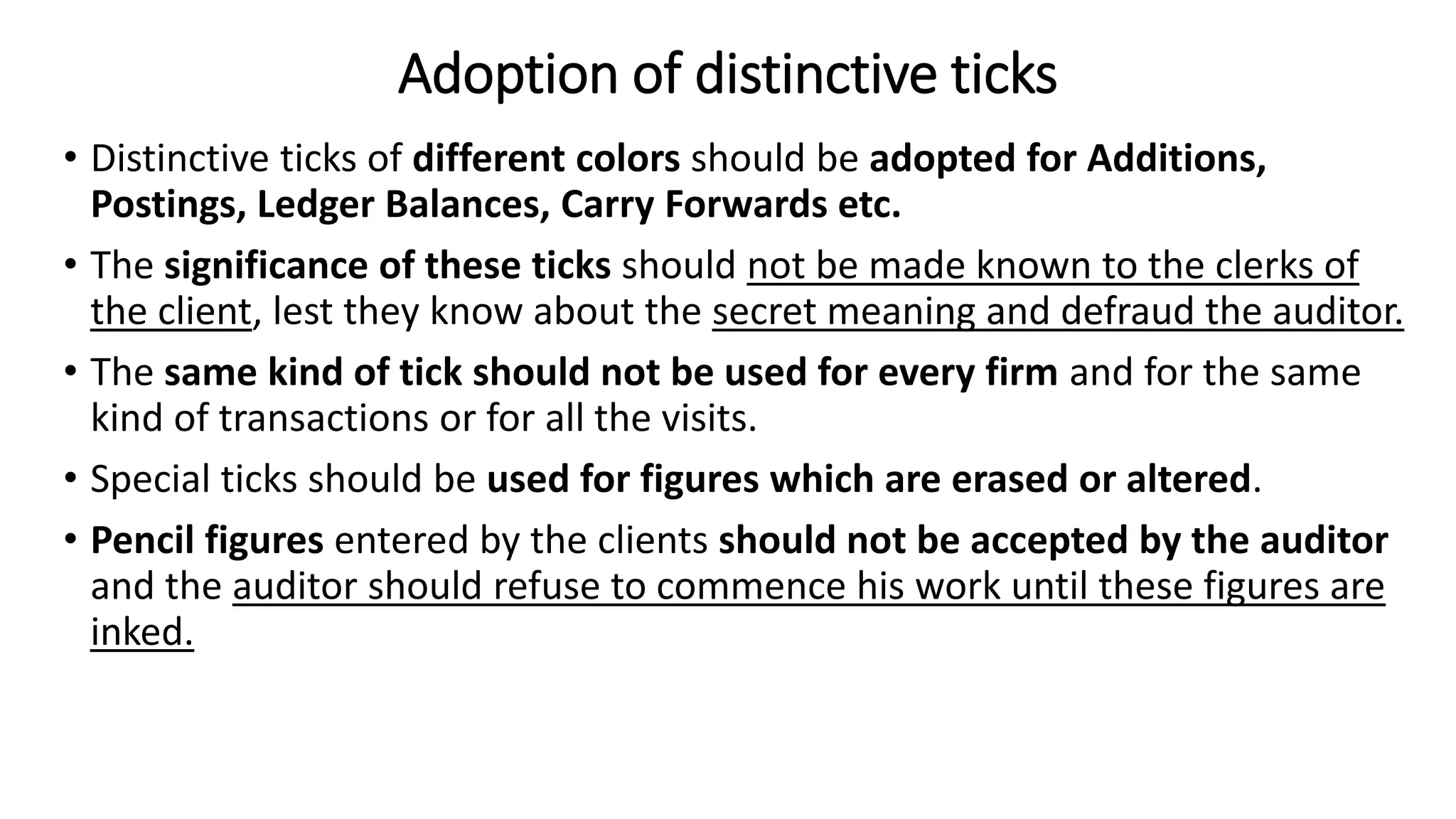

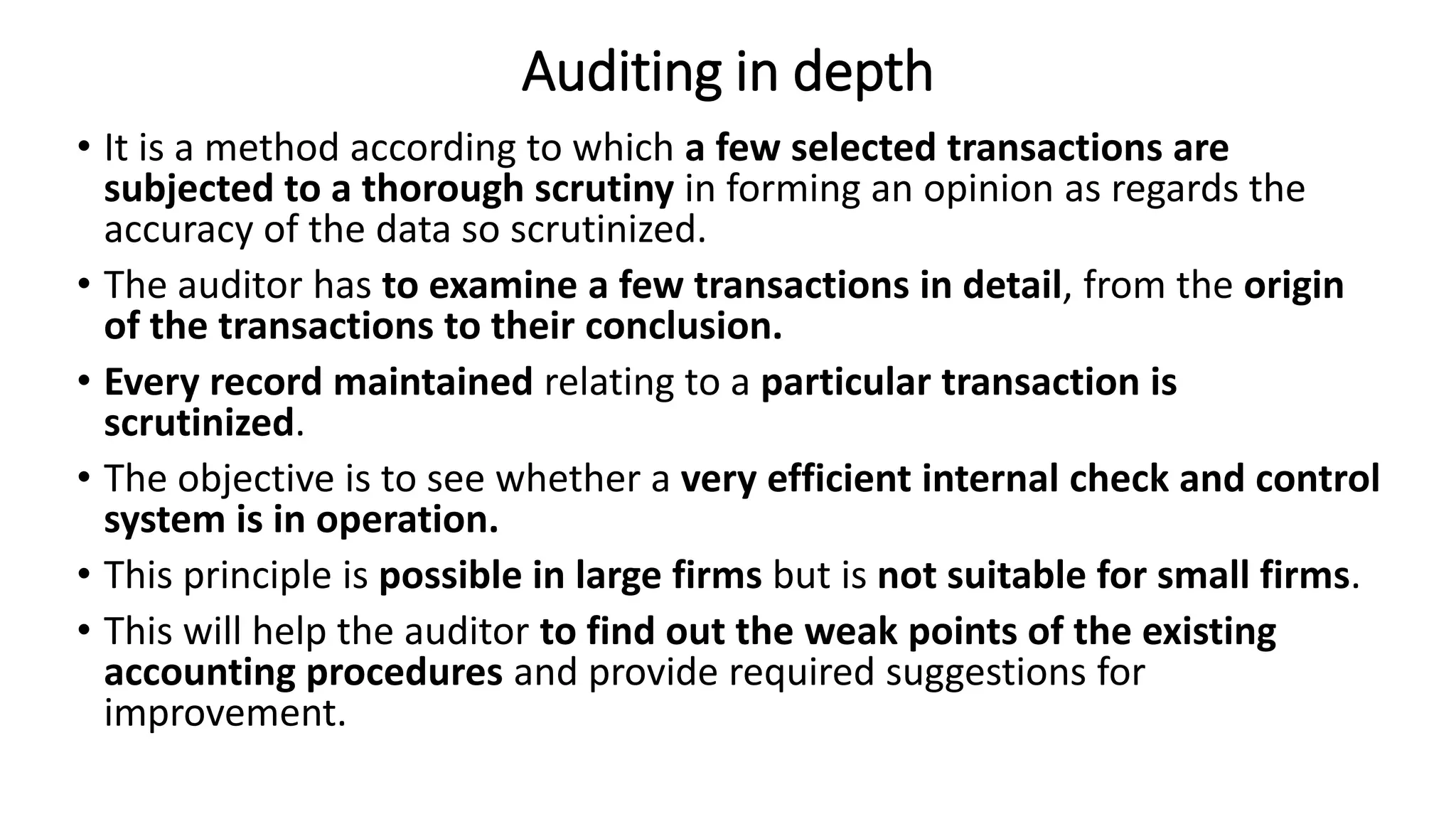

The document outlines the preparations and procedures involved in auditing, detailing essential steps such as verifying appointments, understanding company documents, and planning audit programs. It emphasizes the creation of audit working papers and files, and introduces methods like routine checking and test checking to identify errors and ensure proper audit practices. Key considerations for auditors include maintaining a robust internal check system, the use of distinctive ticks for documentation, and understanding the necessity of thorough examinations for accuracy.

![Audit evidence a framework (ppt ch7[1].pdf)](https://cdn.slidesharecdn.com/ss_thumbnails/auditevidence-aframeworkpptch71-pdf-121211154609-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)