Download as PDF, PPTX

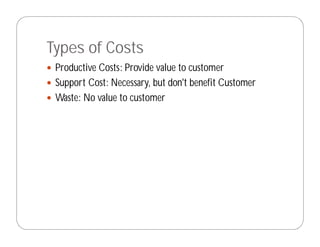

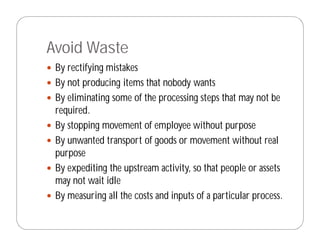

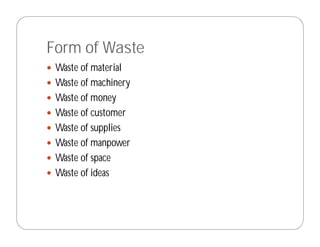

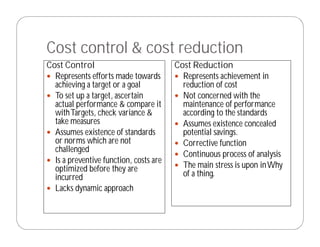

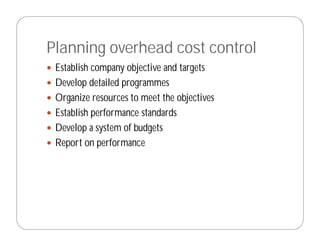

Strategic cost control involves identifying three types of costs: productive costs that provide value to customers, support costs that are necessary but don't directly benefit customers, and waste that provides no value. Organizations can control costs by avoiding waste through various means like eliminating unnecessary processing steps, stopping non-value adding movement of employees and goods, and measuring all costs and inputs. Effective cost control involves setting targets, measuring actual performance against targets, identifying variances, and taking corrective actions. It is a preventative function aimed at optimizing costs before they are incurred. Strategic thinking about cost control requires examining cost allocation mechanisms, manager awareness of cost implications, and distinguishing between restraint-based and freedom-based forms of control.