Downloaded 149 times

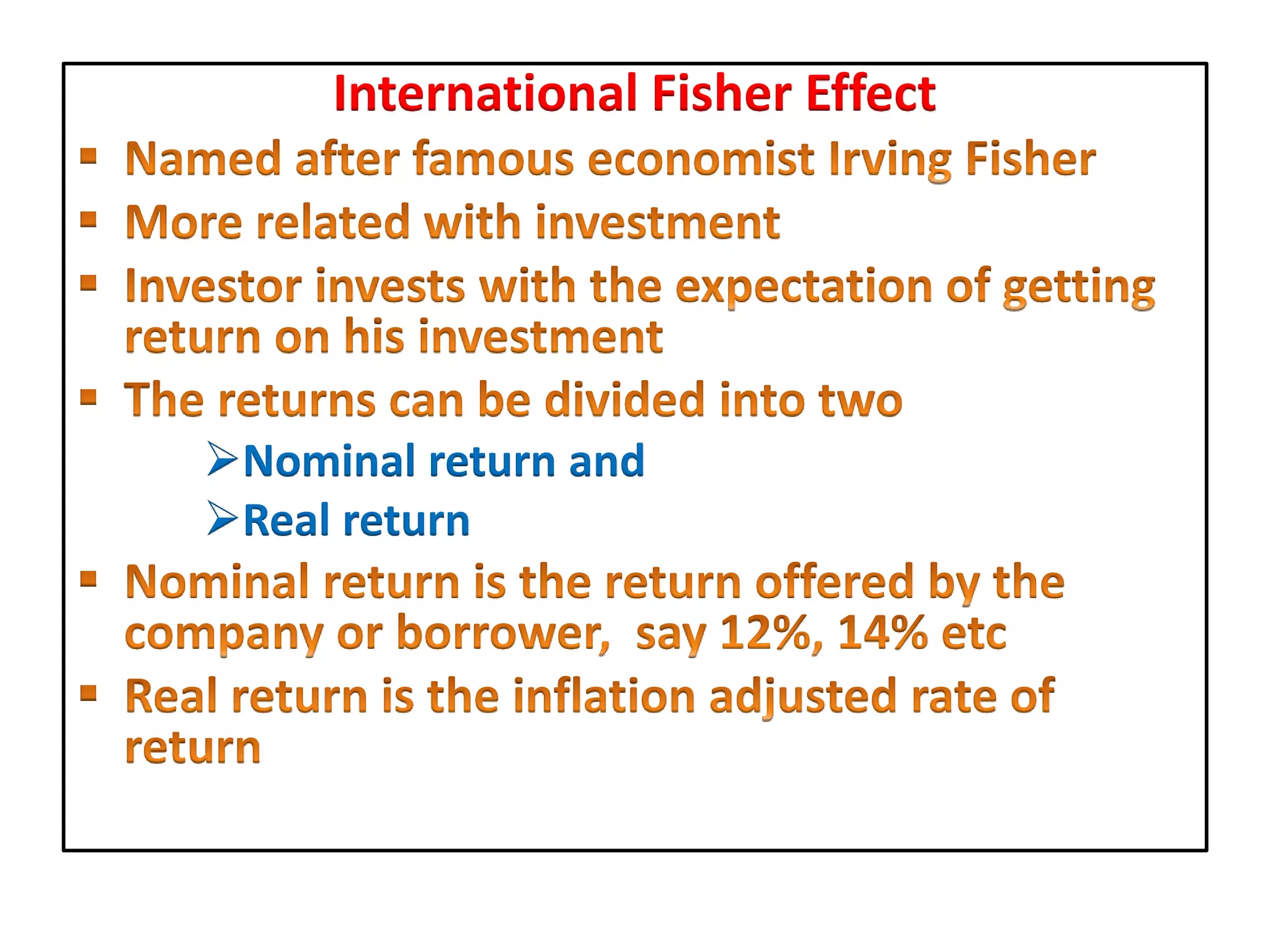

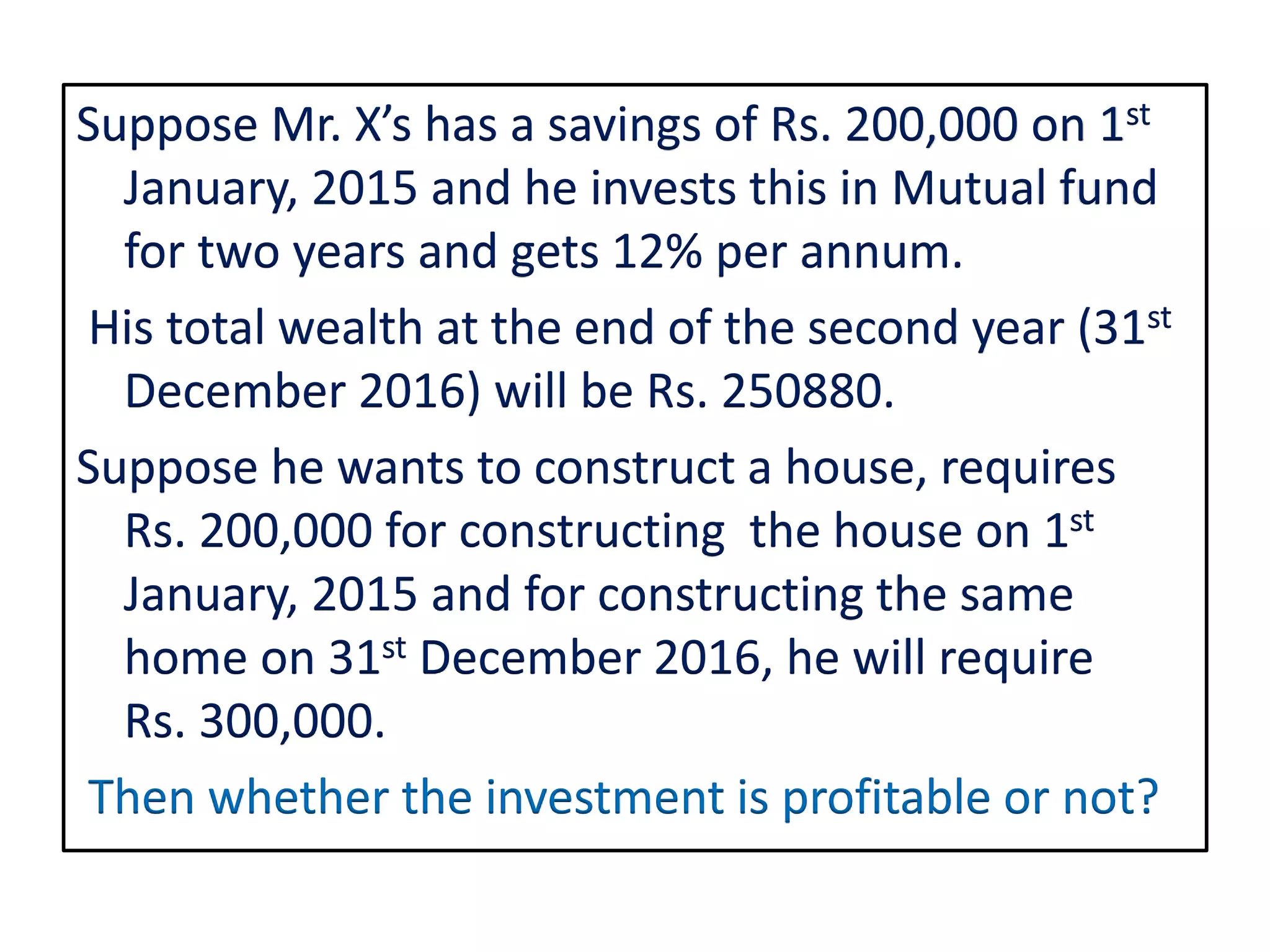

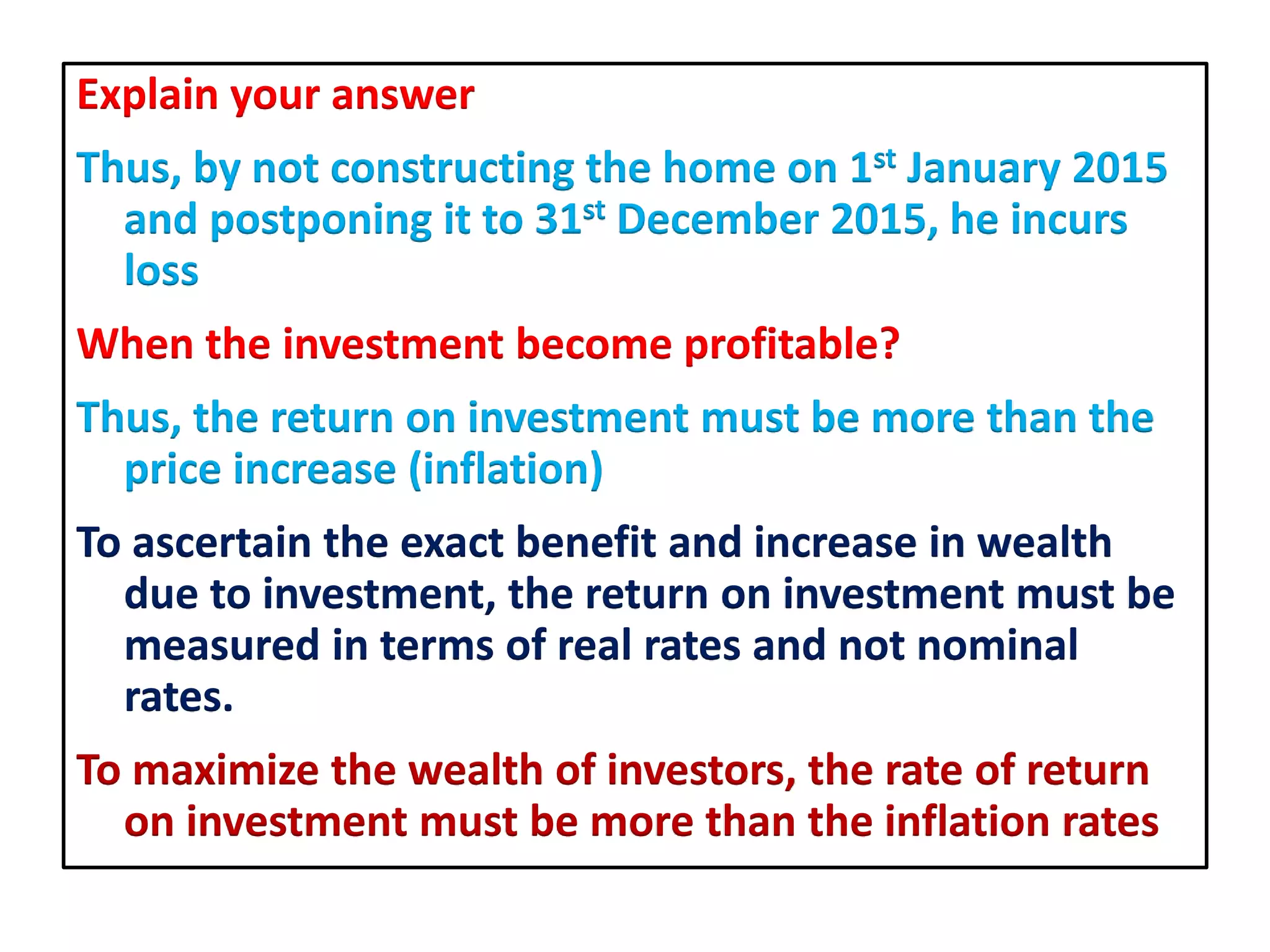

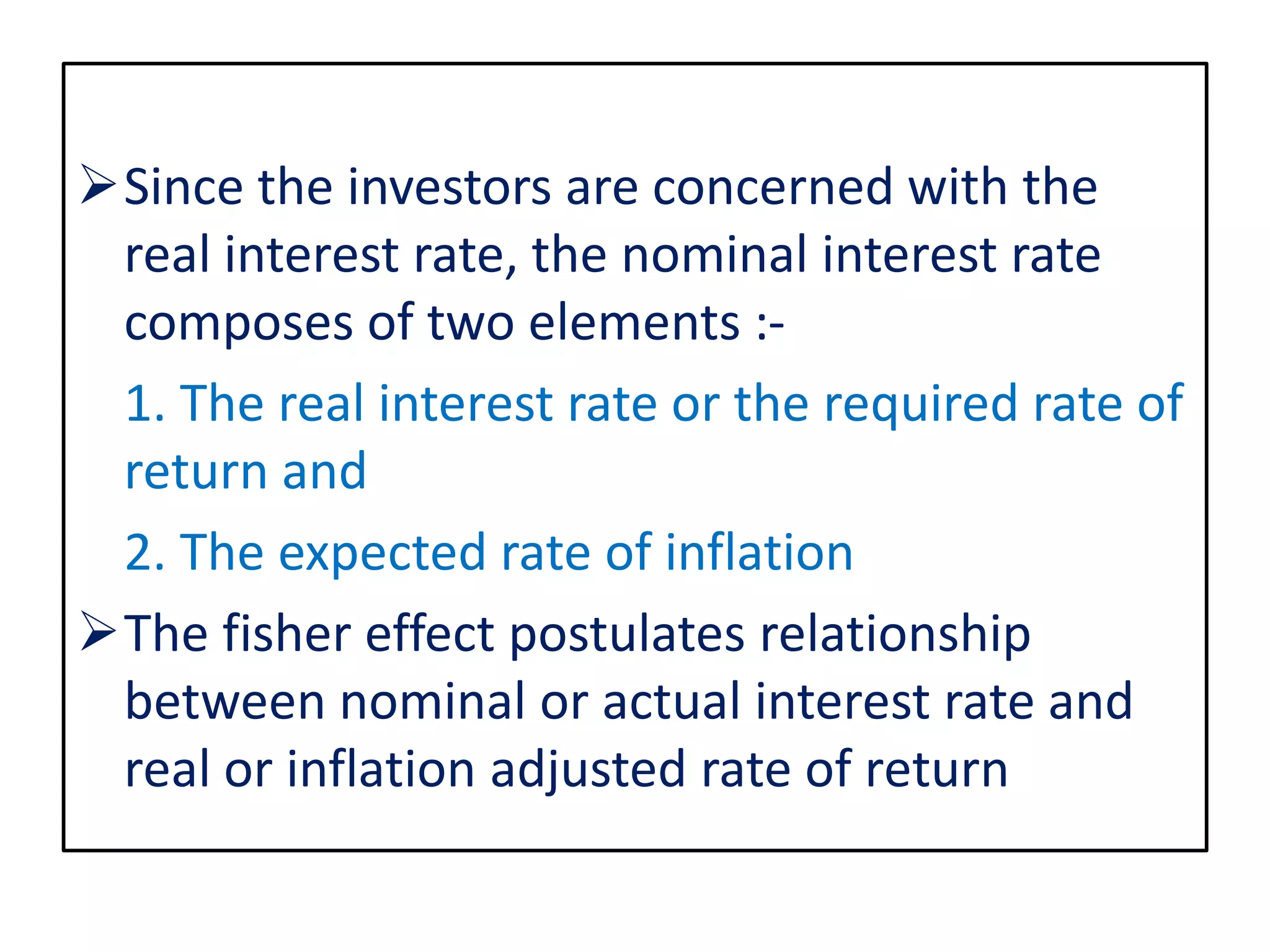

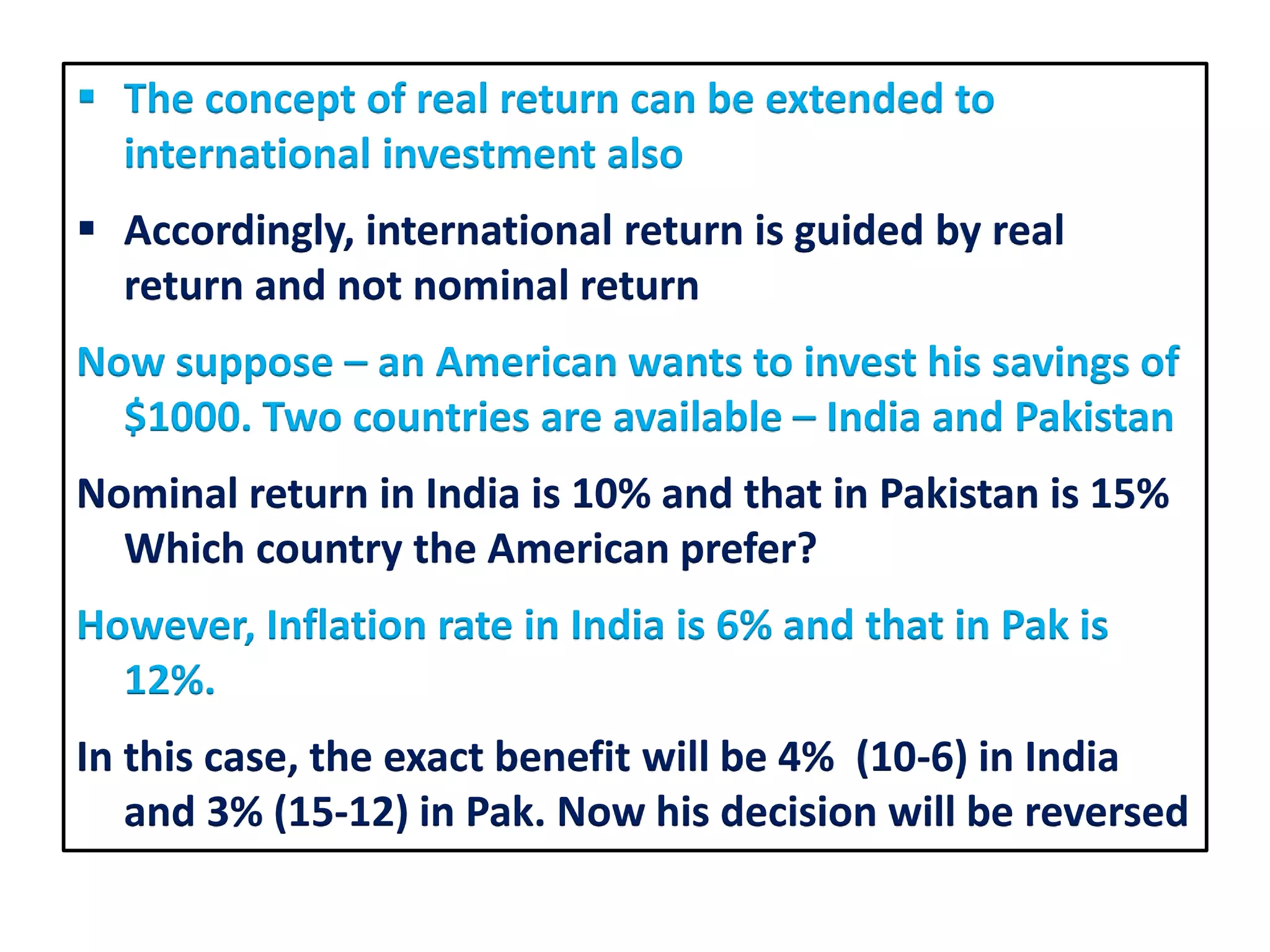

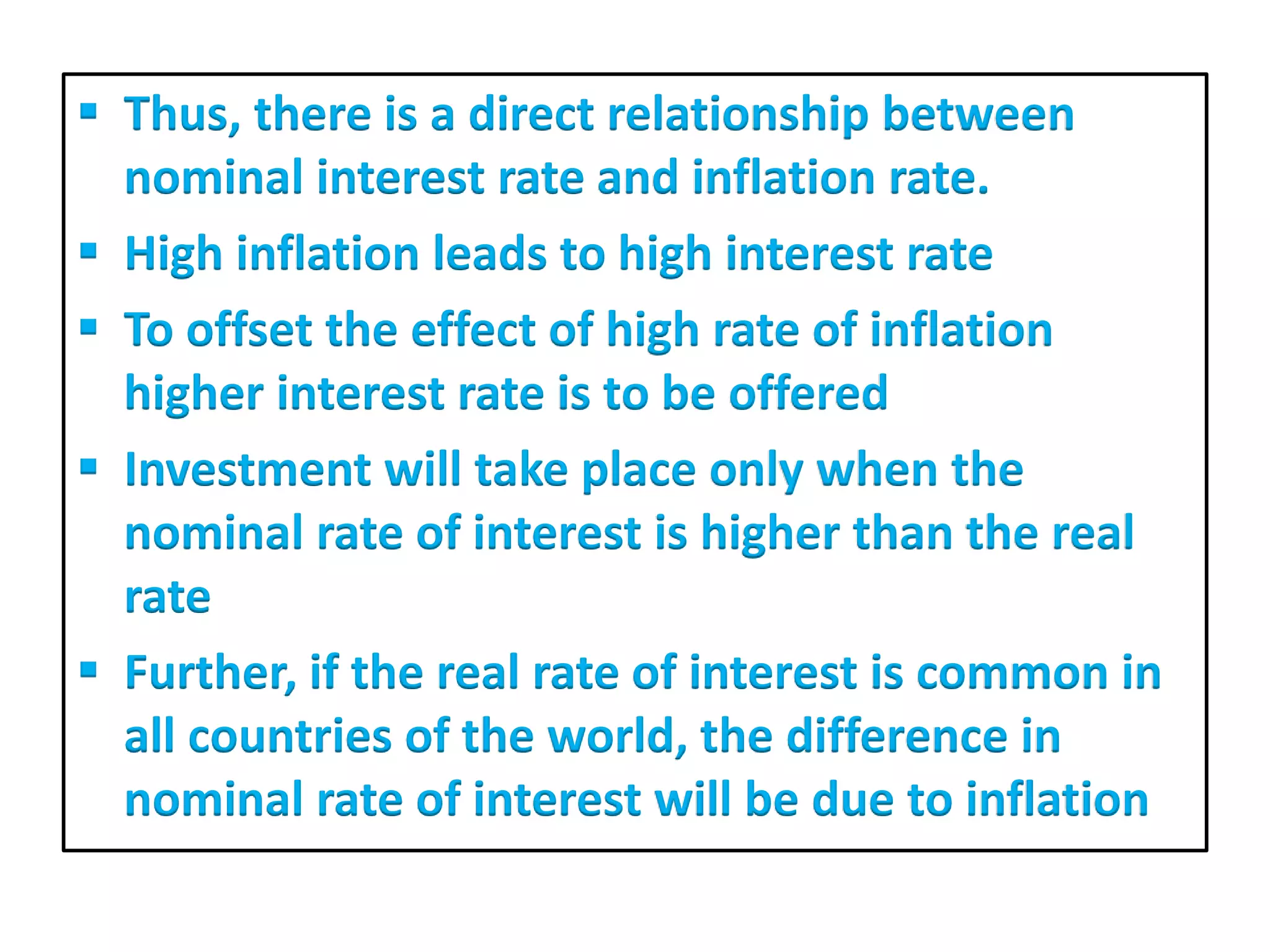

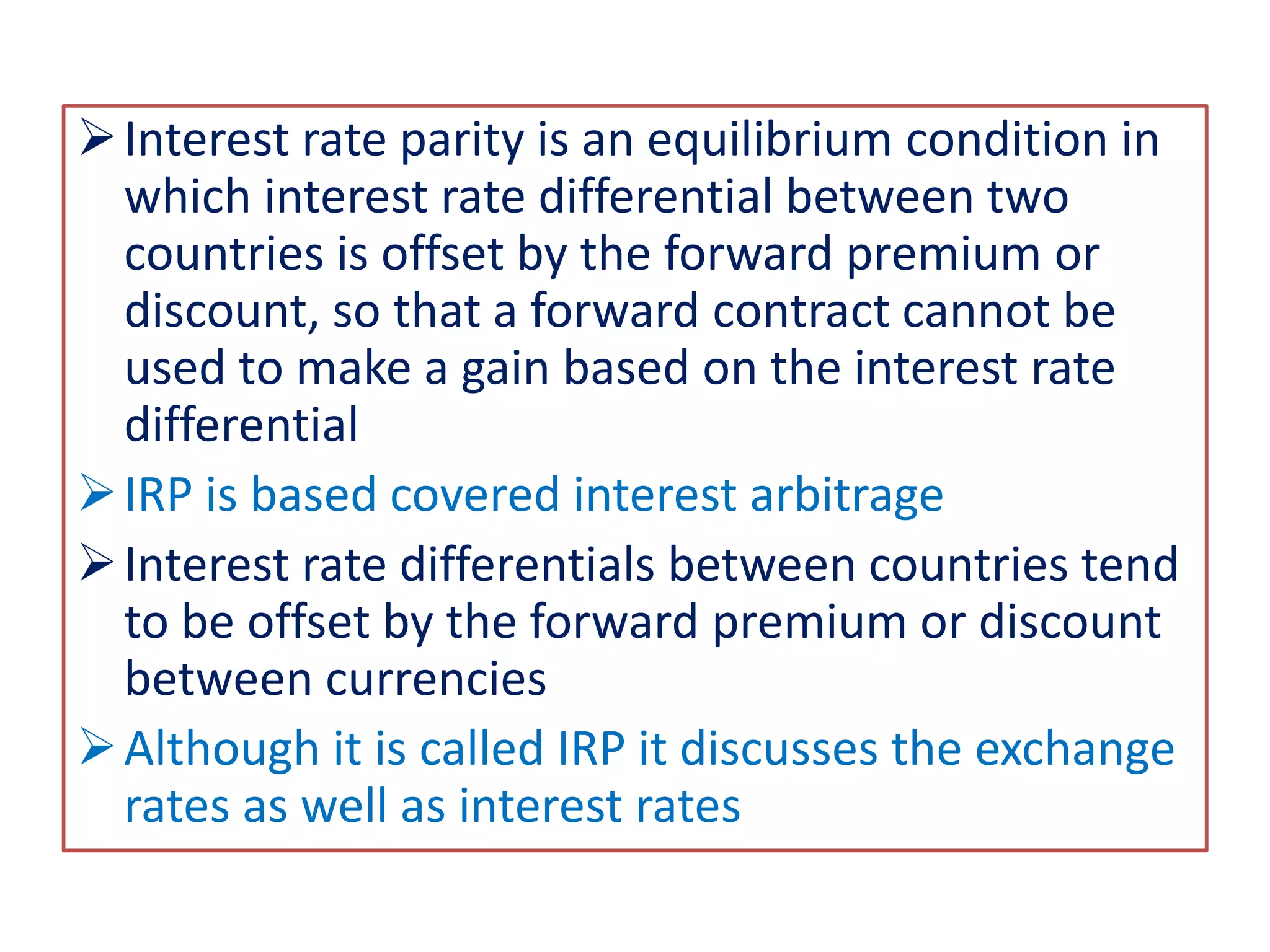

This document discusses the international Fisher effect and interest rate parity. It explains that the Fisher effect postulates a relationship between nominal interest rates and real interest rates adjusted for inflation. According to the Fisher effect, high inflation leads to high nominal interest rates. The document also discusses how interest rate parity argues that identical securities should have the same price when quoted in a common currency, so interest rate differentials between countries tend to be offset by forward exchange rate premiums or discounts.