Downloaded 19 times

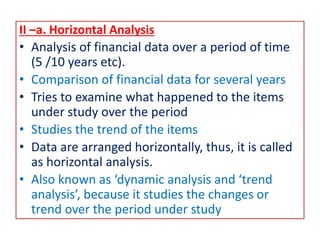

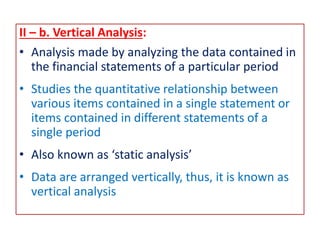

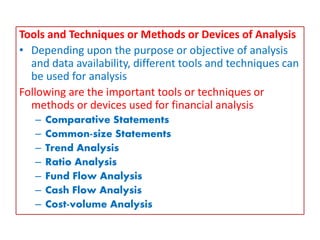

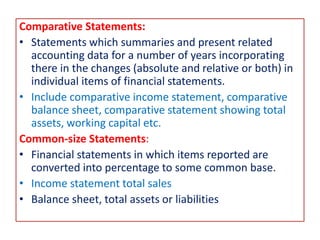

The document discusses the analysis and interpretation of financial statements, emphasizing their importance for various stakeholders and the methods used for evaluation. It differentiates between 'analysis' as a simplification of financial data and 'interpretation' as the explanation of its significance, while outlining objectives and steps for analysis. Additionally, it covers internal and external analysis, horizontal and vertical analysis, and various tools such as comparative statements, common-size statements, and ratio analysis.