Downloaded 25 times

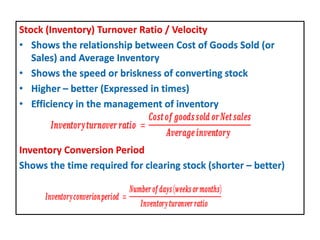

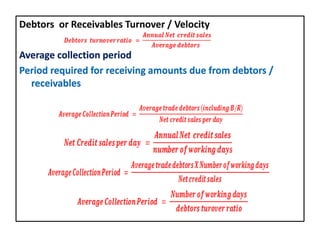

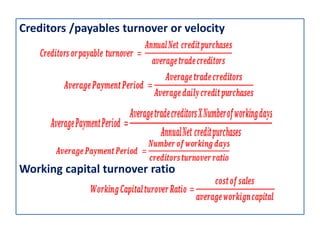

This document discusses various activity and efficiency ratios used to measure the operational performance of a business. It defines stock turnover ratio, debtors turnover ratio, creditors turnover ratio, and working capital turnover ratio. For stock turnover ratio, it provides the calculation and explains that a higher ratio indicates more efficient inventory management. It also defines inventory conversion period and average collection period as metrics related to stock and debtors turnover ratios.